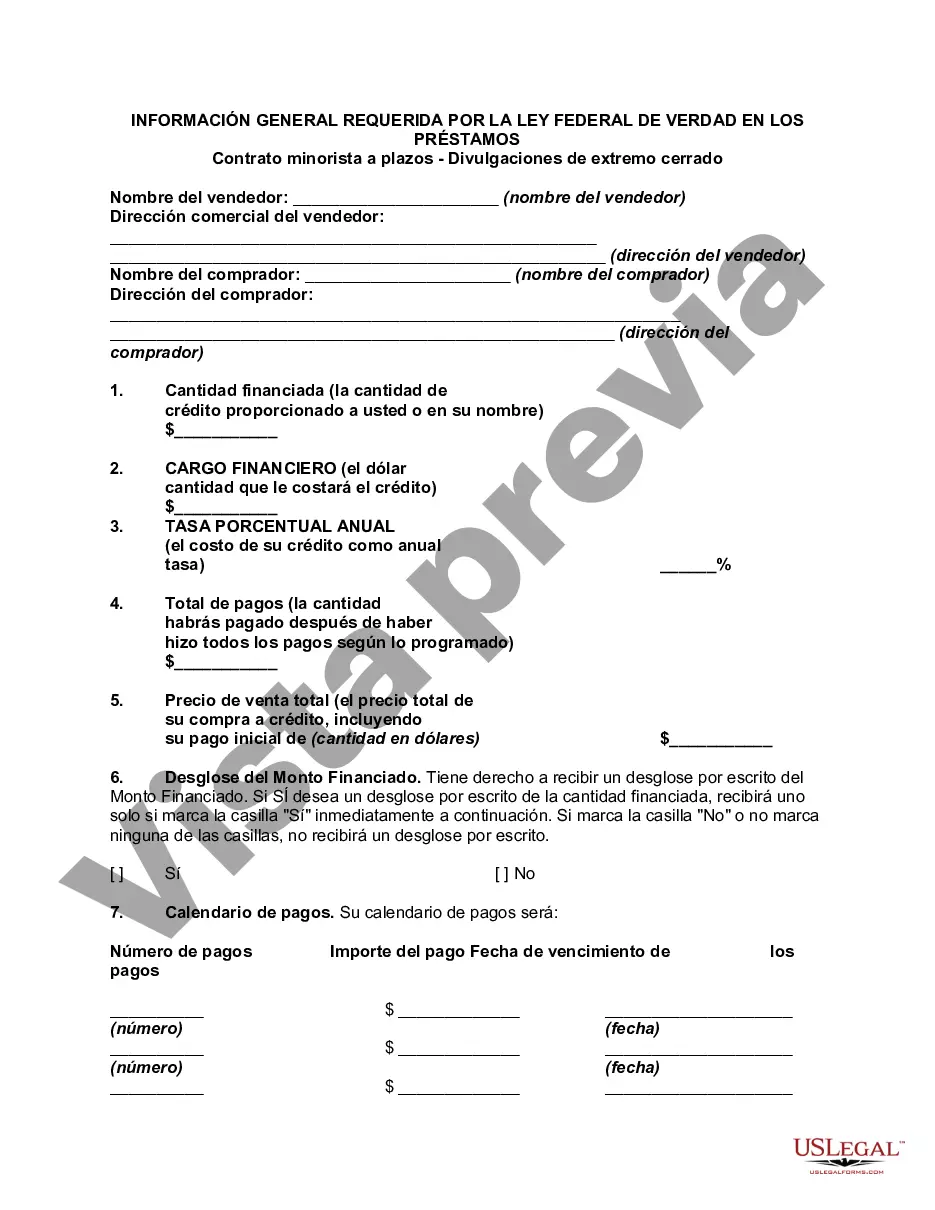

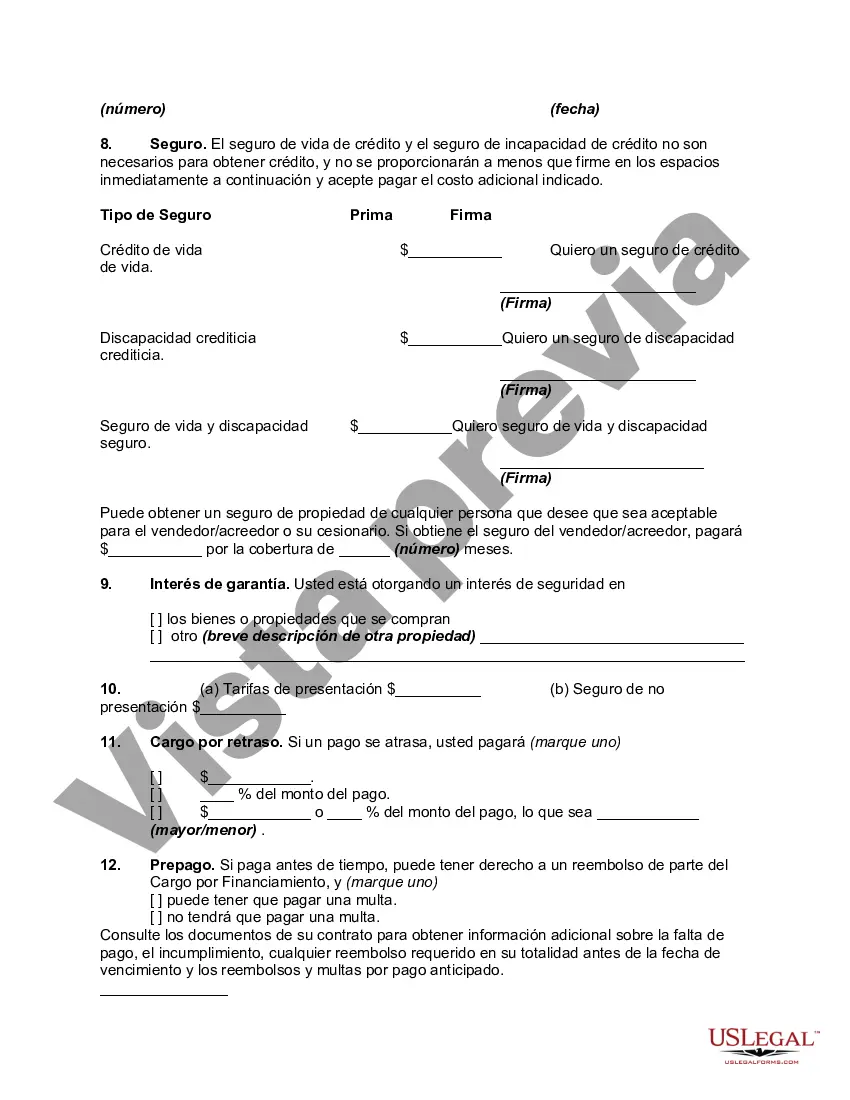

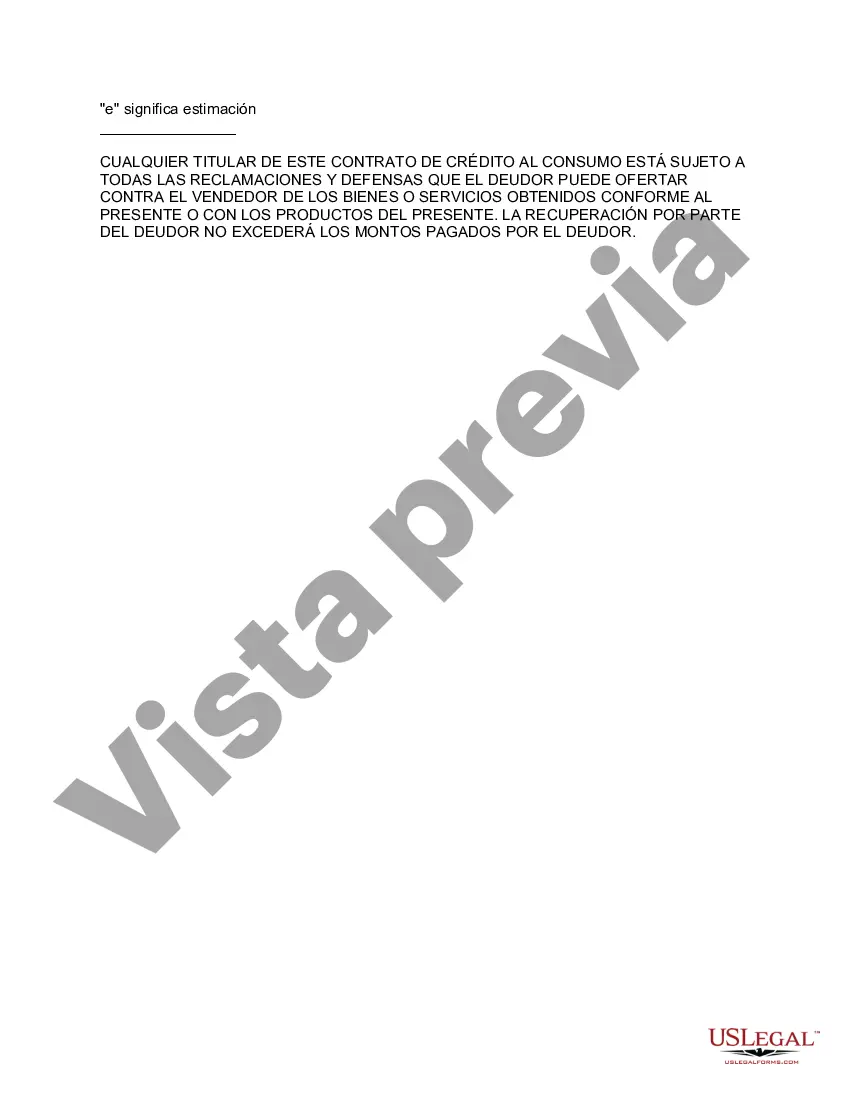

New Mexico General Disclosures Required By The Federal Truth In Lending Act — Retail InstallmenContractac— - Closed End Disclosures The Federal Truth in Lending Act (TILL) is a federal law in the United States that aims to protect consumers and ensure transparency in lending practices. In New Mexico, the TILL applies to retail installment contracts that fall under closed-end credit arrangements. As part of the TILL requirements, certain general disclosures must be provided to borrowers in New Mexico. Here are the key details and relevant keywords related to New Mexico general disclosures required by TILL for retail installment contracts: Annual Percentage Rate (APR): The APR is one of the most important disclosures mandated by TILL. It represents the cost of credit, including both the interest rate charged and certain finance charges expressed as a yearly rate. Finance Charge: The finance charge includes any charges, fees, or interest borrowers must pay for the credit being extended. It is an essential disclosure that indicates the total amount the borrower will pay over the life of the loan. Amount Financed: This disclosure refers to the actual amount of credit that the borrower will receive once any applicable charges or fees are deducted. It provides borrowers with a clear understanding of the net amount they will have available for use. Total Sales Price: The total sales price is the sum of the amount financed and the finance charge. It highlights the overall amount the borrower will repay during the loan term. Payment Schedule: The payment schedule outlines the number, frequency, and amount of payments the borrower is required to make. This disclosure helps borrowers anticipate and plan their repayment obligations. Prepayment Penalty: If the loan includes any penalties for prepaying the outstanding balance, it must be explicitly disclosed. Borrowers need to be aware of any financial repercussions they may face by repaying the loan early. Late Payment Fees: When applicable, lenders must disclose any penalties or fees imposed for late payments. This helps borrowers understand the consequences of missed or delayed payments. Security Interest: If the loan is secured by collateral, such as a vehicle or property, details about the security interest must be disclosed. This includes a description of the collateral and any potential risks associated with a default on the loan. In addition to the above general disclosures, it is important to note that TILL includes specific requirements for other disclosures, such as the right to rescind, advertising terms, and mortgage-related transactions. However, these pertain to different types of credit arrangements and may not directly apply to retail installment contracts. Compliance with the New Mexico General Disclosures Required By The Federal Truth In Lending Act is vital for lenders and financial institutions to ensure transparency and protect the rights of consumers. By providing borrowers with accurate and comprehensive information about loan terms and costs, lenders can foster a fair and informed borrowing process.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.New Mexico Divulgaciones generales requeridas por la Ley Federal de Veracidad en los Préstamos - Contrato minorista a plazos - Divulgaciones cerradas - General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures

Description

How to fill out New Mexico Divulgaciones Generales Requeridas Por La Ley Federal De Veracidad En Los Préstamos - Contrato Minorista A Plazos - Divulgaciones Cerradas?

US Legal Forms - one of many biggest libraries of lawful varieties in the USA - delivers an array of lawful papers themes you may down load or print out. Making use of the website, you can find a huge number of varieties for enterprise and person functions, categorized by categories, suggests, or keywords and phrases.You can get the most up-to-date variations of varieties such as the New Mexico General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures in seconds.

If you already have a membership, log in and down load New Mexico General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures from your US Legal Forms local library. The Down load button can look on each develop you look at. You get access to all in the past downloaded varieties inside the My Forms tab of the bank account.

In order to use US Legal Forms the very first time, listed below are easy guidelines to get you started out:

- Make sure you have selected the right develop for your metropolis/county. Click on the Review button to examine the form`s information. Read the develop information to actually have chosen the correct develop.

- If the develop does not satisfy your specifications, use the Look for industry on top of the display screen to discover the one who does.

- Should you be happy with the form, confirm your choice by clicking the Buy now button. Then, choose the costs prepare you prefer and offer your accreditations to sign up for an bank account.

- Approach the deal. Make use of Visa or Mastercard or PayPal bank account to finish the deal.

- Choose the file format and down load the form in your device.

- Make modifications. Fill up, revise and print out and indicator the downloaded New Mexico General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures.

Every template you included in your account lacks an expiration particular date and is your own property eternally. So, in order to down load or print out one more version, just go to the My Forms section and then click on the develop you want.

Get access to the New Mexico General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures with US Legal Forms, one of the most extensive local library of lawful papers themes. Use a huge number of expert and condition-particular themes that meet your business or person requires and specifications.