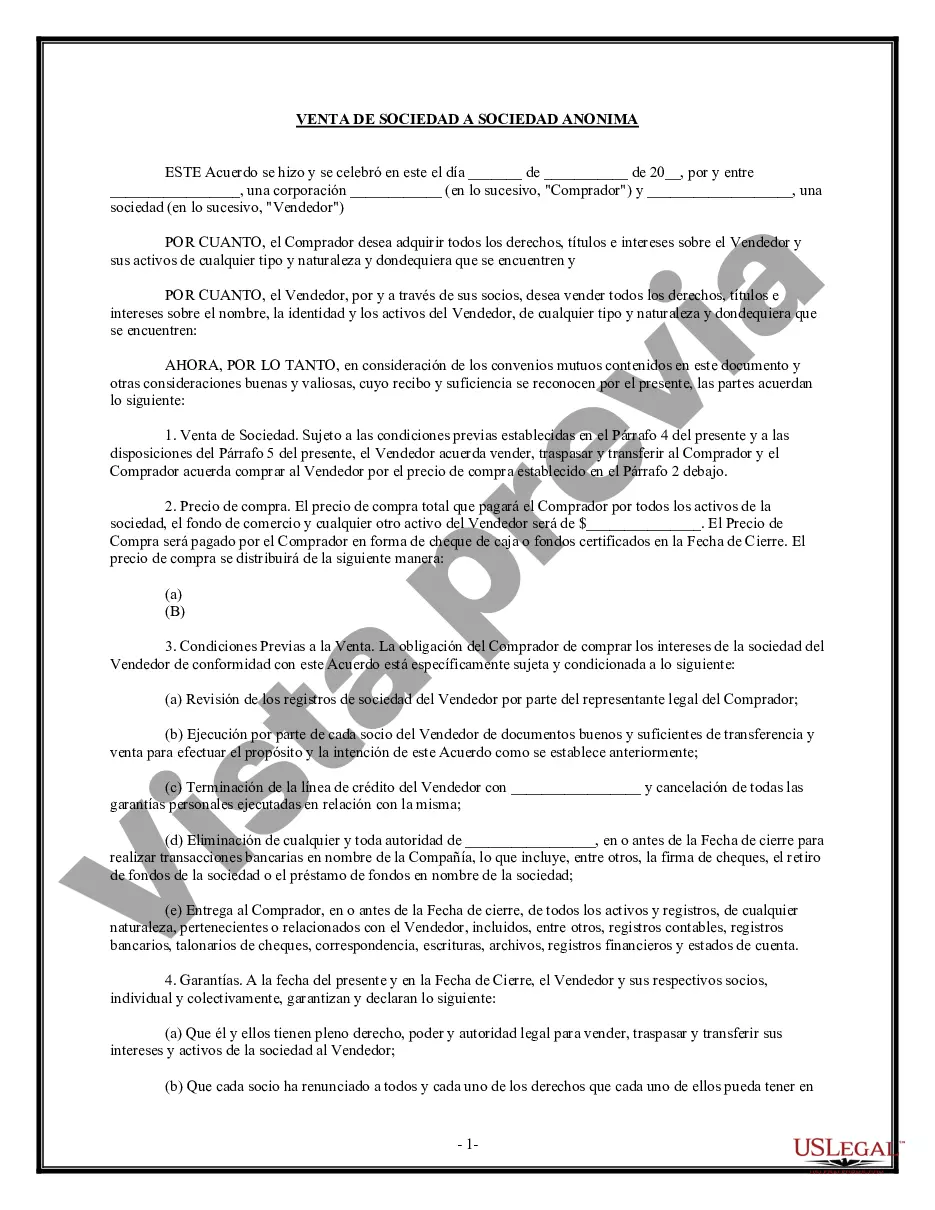

New York Sale of Partnership to Corporation refers to the legal process of transferring ownership of a partnership to a corporation in the state of New York. This transaction typically involves one or more partners selling their partnership interest to a corporation, allowing the corporation to become a partner or owner of the partnership entity. The sale of partnership interest to a corporation can occur for various reasons, such as strategic restructuring, tax considerations, or to facilitate the growth and expansion of the partnership. This transaction requires careful planning and adherence to the legal requirements set forth by the state of New York. There are different types of sales of partnership to corporation transactions that can take place in New York: 1. Outright Sale: In this type of transaction, the partner(s) sell their entire ownership interest in the partnership to the corporation. The corporation then assumes the rights and responsibilities associated with the partnership interest. 2. Partial Sale: In this scenario, a partner sells only a portion of their ownership interest in the partnership to the corporation. This allows the partner to retain some ownership while giving the corporation a stake in the partnership. 3. Merger: Instead of a direct sale, a merger can occur where the partnership and corporation combine their assets, liabilities, and operations into a new corporate entity. This results in the dissolution of the partnership and the creation of a new corporation. 4. Conversion: Conversion involves changing the legal structure of the partnership into a corporation. The partnership assets and liabilities are transferred to the newly formed corporation, and the partners become shareholders. Regardless of the type of New York Sale of Partnership to Corporation, certain steps need to be followed. This includes drafting and executing legal documents such as a purchase and sale agreement, a partnership dissolution agreement, and various forms required by the New York Department of State. Important considerations in this process include valuation of the partnership interest, negotiation of terms and conditions, compliance with tax laws, and the allocation of profits and losses among the partners and the corporation. Consulting with experienced corporate attorneys and tax professionals in New York is crucial to ensure compliance with applicable laws and to navigate the complexities associated with the Sale of Partnership to Corporation.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.New York Venta de Sociedad a Corporación - Sale of Partnership to Corporation

Description

How to fill out New York Venta De Sociedad A Corporación?

Choosing the best lawful file format can be quite a have a problem. Of course, there are tons of themes available online, but how can you get the lawful form you need? Make use of the US Legal Forms internet site. The support delivers a huge number of themes, such as the New York Sale of Partnership to Corporation, which you can use for enterprise and private requirements. Each of the forms are checked out by experts and meet federal and state needs.

In case you are presently listed, log in to your bank account and then click the Obtain option to find the New York Sale of Partnership to Corporation. Utilize your bank account to appear with the lawful forms you have bought earlier. Check out the My Forms tab of your respective bank account and have an additional version from the file you need.

In case you are a new customer of US Legal Forms, listed here are simple directions that you can stick to:

- Initially, make sure you have selected the correct form for the town/region. You are able to look through the form making use of the Preview option and read the form information to ensure this is the best for you.

- If the form will not meet your preferences, use the Seach industry to discover the correct form.

- When you are positive that the form is suitable, go through the Purchase now option to find the form.

- Opt for the pricing program you want and enter in the needed details. Design your bank account and pay money for the transaction with your PayPal bank account or charge card.

- Pick the document format and obtain the lawful file format to your device.

- Total, revise and print out and signal the acquired New York Sale of Partnership to Corporation.

US Legal Forms is definitely the biggest library of lawful forms where you will find different file themes. Make use of the company to obtain expertly-created documents that stick to status needs.