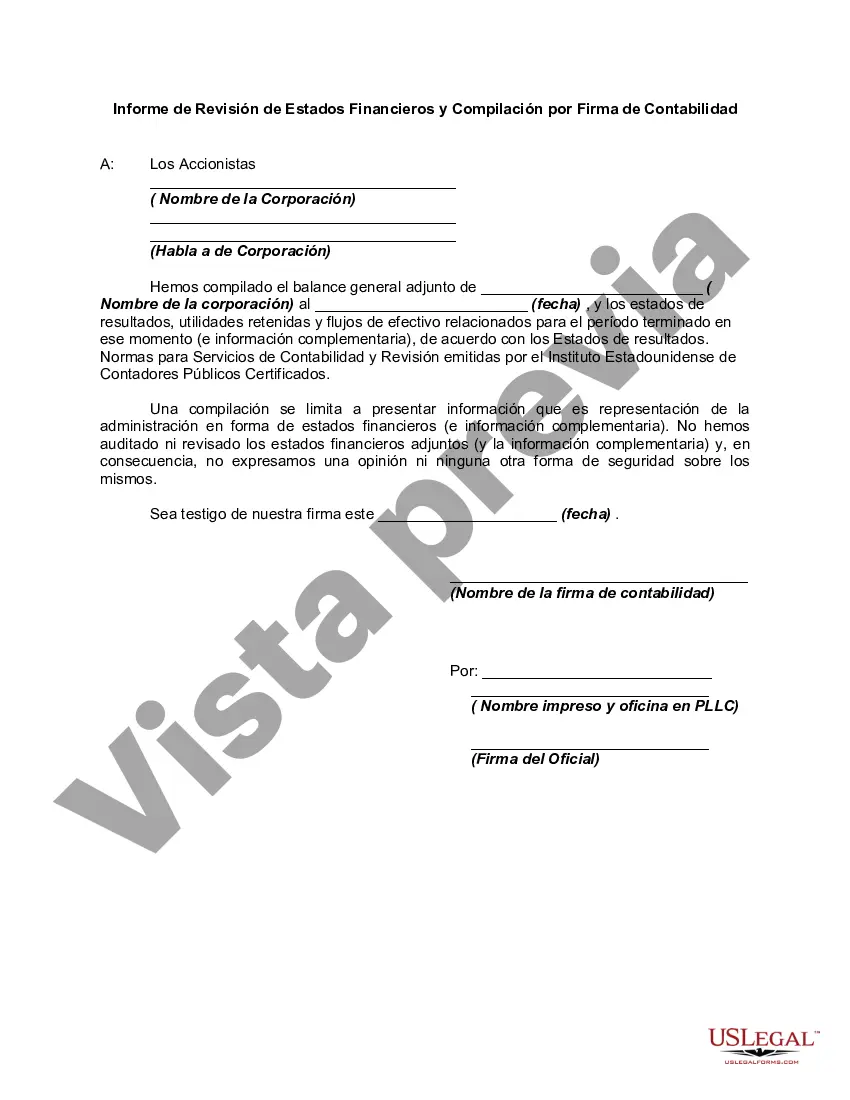

In a compilation engagement, the accountant presents in the form of financial statements information that is the representation of management (owners) without undertaking to express any assurance on the statements. In other words, using management's records, the accountant creates financial statements without gathering evidence or opining about the validity of those underlying records. Because compiled financial statements provide the reader no assurance regarding the statements, they represent the lowest level of financial statement service accountants can provide to their clients. Accordingly, standards governing compilation engagements require that financial statements presented by the accountant to the client or third parties must at least be compiled.

Ohio Report from Review of Financial Statements and Compilation by Accounting Firm An Ohio Report from Review of Financial Statements and Compilation by Accounting Firm is a comprehensive evaluation of a company's financial records conducted by an independent accounting firm based in Ohio. This type of report is crucial for businesses as it provides an objective assessment of their financial health, assisting stakeholders, such as investors, creditors, and management, in making informed decisions. The Ohio Report from Review of Financial Statements may come in different forms that cater to specific requirements. These types include: 1. Ohio Report from Review of Financial Statements: This report offers a limited level of assurance for financial statements. The accounting firm conducts analytical procedures, inquiries, and other review procedures to provide reasonable assurance that the financial statements conform to Generally Accepted Accounting Principles (GAAP). However, a review does not provide absolute assurance of the accuracy of the financial statements. 2. Ohio Report from Compilation: Unlike a review, a compilation report does not provide any level of assurance. Instead, the accounting firm compiles the financial statements from management's data without performing substantive auditing procedures. This report is suitable for companies that do not require a high level of assurance or when financial statements are used internally. Regardless of the type, an Ohio Report from Review of Financial Statements and Compilation by an Accounting Firm typically includes the following key components: 1. Independent Accountant's Report: This section contains the accounting firm's opinion on the financial statements or compilation. It outlines the scope of the engagement, procedures performed, and whether the financial statements comply with GAAP. 2. Management's Responsibility: This section describes management's responsibility for preparing and presenting the financial statements. It emphasizes the integrity of financial data, the selection of accounting policies, and the evaluation of the company's ability to continue as a going concern. 3. Financial Statements: This section includes the company's balance sheet, income statement, statement of cash flows, and notes to the financial statements. The financial statements present an overview of the company's financial position, performance, and cash flows for a specific period. 4. Accountant's Findings: In a review report, this section highlights any significant findings or potential issues identified during the review process. It may include recommended adjustments or suggestions for improving financial reporting practices. 5. Limitations: Acknowledging the inherent limitations of a review or compilation engagement, this section outlines the inherent risks and restrictions associated with such reports. The Ohio Report from Review of Financial Statements and Compilation by Accounting Firm is an essential tool for evaluating a company's financial performance and ensuring transparency. By providing stakeholders with reliable financial information, businesses can instill confidence and promote informed decision-making.Ohio Report from Review of Financial Statements and Compilation by Accounting Firm An Ohio Report from Review of Financial Statements and Compilation by Accounting Firm is a comprehensive evaluation of a company's financial records conducted by an independent accounting firm based in Ohio. This type of report is crucial for businesses as it provides an objective assessment of their financial health, assisting stakeholders, such as investors, creditors, and management, in making informed decisions. The Ohio Report from Review of Financial Statements may come in different forms that cater to specific requirements. These types include: 1. Ohio Report from Review of Financial Statements: This report offers a limited level of assurance for financial statements. The accounting firm conducts analytical procedures, inquiries, and other review procedures to provide reasonable assurance that the financial statements conform to Generally Accepted Accounting Principles (GAAP). However, a review does not provide absolute assurance of the accuracy of the financial statements. 2. Ohio Report from Compilation: Unlike a review, a compilation report does not provide any level of assurance. Instead, the accounting firm compiles the financial statements from management's data without performing substantive auditing procedures. This report is suitable for companies that do not require a high level of assurance or when financial statements are used internally. Regardless of the type, an Ohio Report from Review of Financial Statements and Compilation by an Accounting Firm typically includes the following key components: 1. Independent Accountant's Report: This section contains the accounting firm's opinion on the financial statements or compilation. It outlines the scope of the engagement, procedures performed, and whether the financial statements comply with GAAP. 2. Management's Responsibility: This section describes management's responsibility for preparing and presenting the financial statements. It emphasizes the integrity of financial data, the selection of accounting policies, and the evaluation of the company's ability to continue as a going concern. 3. Financial Statements: This section includes the company's balance sheet, income statement, statement of cash flows, and notes to the financial statements. The financial statements present an overview of the company's financial position, performance, and cash flows for a specific period. 4. Accountant's Findings: In a review report, this section highlights any significant findings or potential issues identified during the review process. It may include recommended adjustments or suggestions for improving financial reporting practices. 5. Limitations: Acknowledging the inherent limitations of a review or compilation engagement, this section outlines the inherent risks and restrictions associated with such reports. The Ohio Report from Review of Financial Statements and Compilation by Accounting Firm is an essential tool for evaluating a company's financial performance and ensuring transparency. By providing stakeholders with reliable financial information, businesses can instill confidence and promote informed decision-making.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.