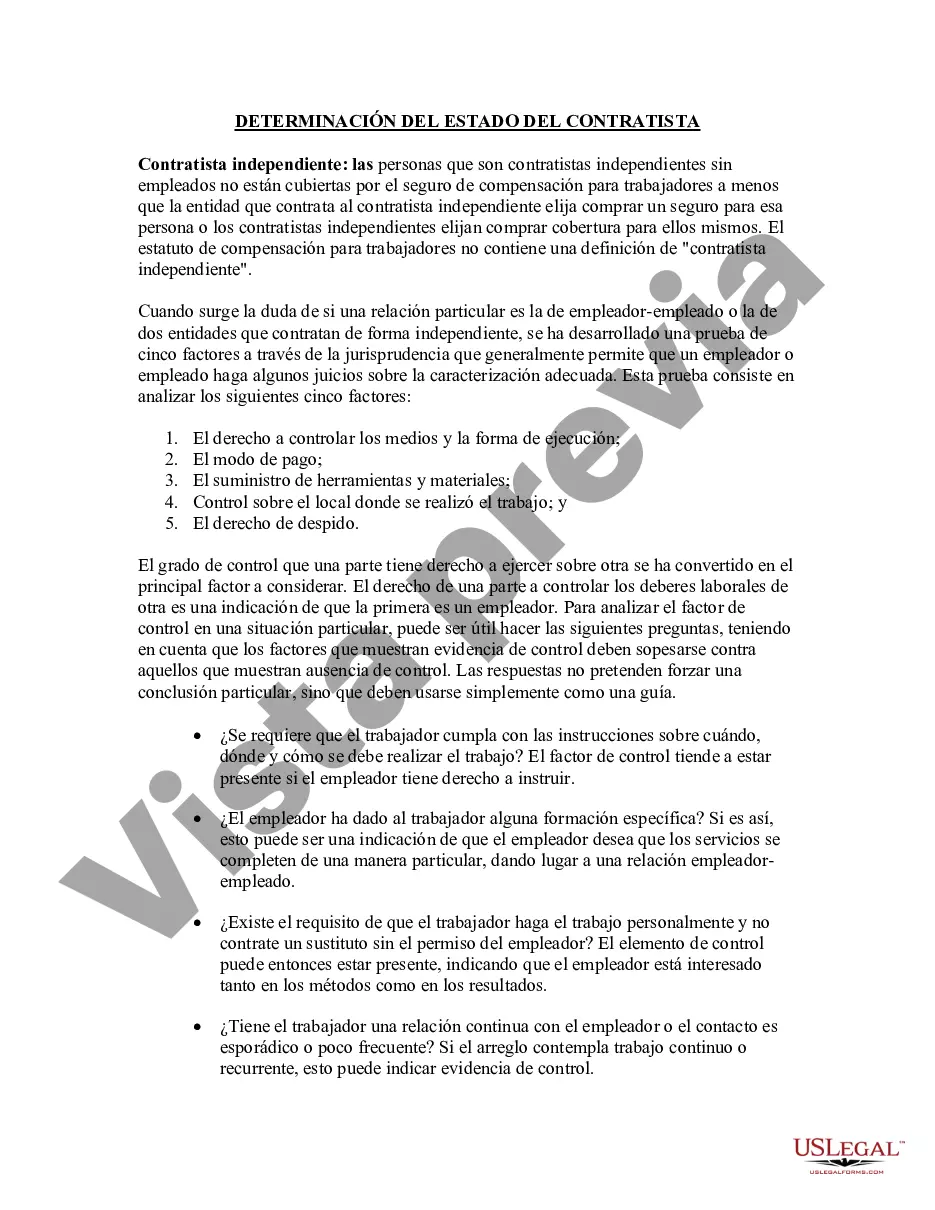

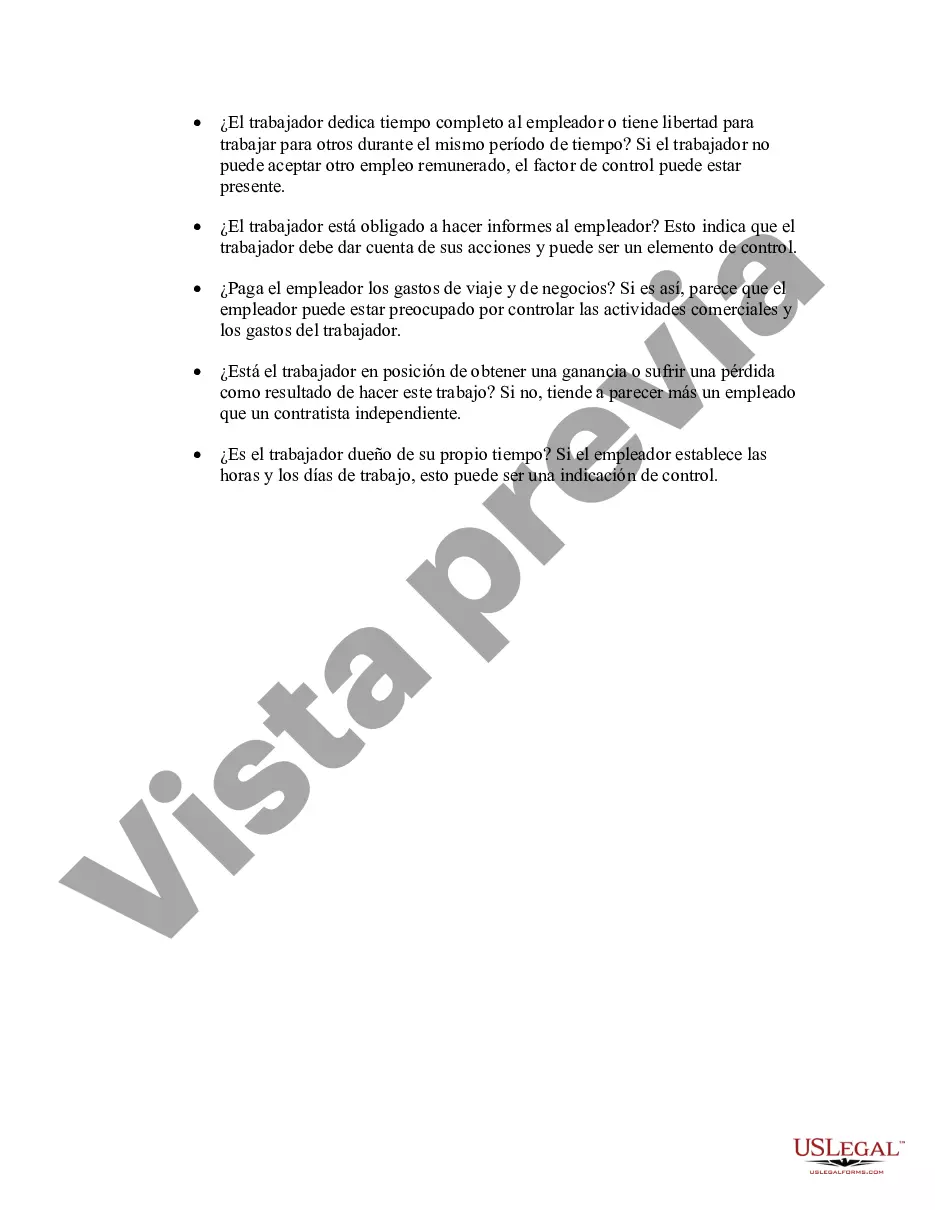

Ohio Determining Self-Employed Contractor Status: A Comprehensive Guide In Ohio, determining the self-employed contractor status plays a crucial role in various industries and businesses. This classification determines the legal and tax obligations of individuals or companies engaging in contractor relationships. Whether you are an employer or a worker, understanding these determinations is essential to ensure compliance with Ohio laws. 1. Criteria Used to Determine Self-Employed Contractor Status: To establish the self-employment contractor status in Ohio, several key factors are considered. These criteria aim to assess the degree of control exercised by the employer over the worker. The determination primarily revolves around the following elements: a) Behavioral Control: This involves evaluating the extent to which an employer controls how a worker performs their duties, including instructions given, training provided, and methods of work evaluation. b) Financial Control: This focuses on examining whether the employer controls the financial aspects of the work, such as reimbursement methods, provision of tools/equipment, and the extent of investment made by the worker. c) Relationship Type: The nature of the relationship between the worker and the employer are also an essential factor in classification. Factors like the presence of a written contract, the permanency of the relationship, and benefits provided may be considered. 2. Types of Self-Employed Contractor Status in Ohio: a) Independent Contractors: Independent contractors are workers who are in business for themselves and maintain control over the services they provide. They operate independently and are usually engaged for a particular project or task. Independent contractors are responsible for their tax payments and reporting. b) Statutory Employees: Statutory employees, despite being labeled as employees for certain employment tax purposes, are still treated as self-employed individuals under Ohio law. They typically include workers engaged in specific professions like traveling salespeople, full-time drivers, and certain home-based workers. c) Common-Law Employees: Common-law employees are individuals whose working conditions and relationship with the employer indicate an employer-employee relationship. They generally work under direct supervision and control of the employer. Consequently, they are not considered self-employed contractors. 3. Importance of Accurate Classification: Properly classifying workers is crucial for both employers and employees in Ohio. Employers that misclassify workers may face legal consequences, penalties, and unpaid taxes. Workers, on the other hand, may miss out on important employee benefits, such as minimum wage requirements, overtime pay, workers' compensation, and unemployment benefits. By correctly determining self-employed contractor status, employers can ensure compliance with Ohio's laws and avoid potential liabilities. Workers can also understand their status and associated rights, fostering a more transparent working relationship. In summary, understanding Ohio's determinations for self-employed contractor status can greatly benefit both employers and workers alike. By evaluating behavioral and financial control factors, as well as considering the type of relationship established, employers can classify workers accurately. This ensures compliance with legal and tax obligations and provides workers with a clear understanding of their rights and entitlements.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Ohio Determinación del estado de contratista que trabaja por cuenta propia - Determining Self-Employed Contractor Status

Description

How to fill out Ohio Determinación Del Estado De Contratista Que Trabaja Por Cuenta Propia?

US Legal Forms - one of the greatest libraries of legitimate types in the States - delivers an array of legitimate record layouts you are able to acquire or printing. Using the website, you may get thousands of types for enterprise and personal purposes, sorted by types, claims, or search phrases.You can get the latest types of types like the Ohio Determining Self-Employed Contractor Status within minutes.

If you already possess a monthly subscription, log in and acquire Ohio Determining Self-Employed Contractor Status in the US Legal Forms collection. The Download key will show up on each type you perspective. You have access to all formerly delivered electronically types in the My Forms tab of your own profile.

If you would like use US Legal Forms for the first time, here are basic guidelines to help you started off:

- Make sure you have picked out the best type for your personal city/county. Click the Preview key to analyze the form`s information. See the type information to ensure that you have selected the appropriate type.

- If the type does not match your needs, use the Search field at the top of the screen to discover the one that does.

- Should you be satisfied with the shape, validate your decision by clicking on the Acquire now key. Then, pick the pricing program you want and provide your credentials to register for an profile.

- Process the transaction. Make use of charge card or PayPal profile to complete the transaction.

- Find the file format and acquire the shape on your own gadget.

- Make alterations. Fill out, edit and printing and indication the delivered electronically Ohio Determining Self-Employed Contractor Status.

Every template you put into your bank account does not have an expiry particular date and is also your own property for a long time. So, in order to acquire or printing an additional backup, just proceed to the My Forms segment and then click on the type you will need.

Gain access to the Ohio Determining Self-Employed Contractor Status with US Legal Forms, probably the most substantial collection of legitimate record layouts. Use thousands of professional and state-certain layouts that meet up with your small business or personal requires and needs.