The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. TILA applies only to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use. This form was designed to cover an situation where the Seller is not a creditor as defined by the TILA.

Title: Exploring Different Types of Oklahoma Installment Sales Not Covered by the Federal Consumer Credit Protection Act with Security Agreements Introduction: In Oklahoma, there are various types of installment sales that are not covered by the Federal Consumer Credit Protection Act (FC CPA) when combined with a security agreement. This article aims to provide a comprehensive understanding of what constitutes an Oklahoma Installment Sale, the importance of the Federal Consumer Credit Protection Act, and the different categories of installment sales exempted under the Act. Keywords: Oklahoma Installment Sale, Federal Consumer Credit Protection Act, FC CPA, Security Agreement 1. Understanding Oklahoma Installment Sales: — Oklahoma Installment Sale refers to a transaction in which a buyer acquires goods or services from a seller and agrees to make payments over a period of time, typically in installments. — The buyer receives immediate possession or use of the goods or services, but ownership is often retained by the seller until the full payment is made. 2. Federal Consumer Credit Protection Act (FC CPA): THCFC CPAPA is a federal law that protects consumers by regulating the consumer credit industry. — It primarily addresses issues such as interest rates, unfair or deceptive practices, credit reporting, debt collection, and disclosure requirements. — However, certain types of installment sales in Oklahoma are not subject to the provisions of the FC CPA due to specific exemptions. 3. Installment Sales Exempted from FC CPA in Oklahoma: a) Agricultural Credit Transactions: — Agriculture-based installment sales involving the financing of agricultural production inputs or equipment used in agricultural operations are among the exemptions. — These sales are designed to facilitate credit for farmers, ranchers, and other professionals engaged in agricultural activities. b) Business-purpose Transactions: — Installment sales made for business purposes, such as the acquisition of assets or services for commercial or industrial use, are exempt from FC CPA coverage. — This exemption aims to ensure that commercial activities are not unduly burdened by consumer credit regulations. c) Real Property Transactions: — Sales or financing arrangements related to real property (land and structures) fall outside the scope of FC CPA coverage. — This exemption applies to both residential and commercial real estate transactions, recognizing the distinct nature of these transactions compared to sales involving movable goods. d) Sales under $25,000: — Installment sales with a credit limit of less than $25,000 are also exempt from FC CPA provisions. — This exemption takes into account smaller transactions where the potential consumer protection issues may be less significant. Conclusion: Understanding the different types of Oklahoma Installment Sales exempted from the Federal Consumer Credit Protection Act is essential for both consumers and businesses. By recognizing these exemptions, consumers can evaluate their rights and protections within various transaction contexts, while businesses can engage in the selling of goods and services for specific purposes without being bound by certain FC CPA requirements. Keywords: Oklahoma Installment Sale, Federal Consumer Credit Protection Act, FC CPA, Security Agreement, exemptions, agricultural credit transactions, business-purpose transactions, real property transactions, sales under $25,000.Title: Exploring Different Types of Oklahoma Installment Sales Not Covered by the Federal Consumer Credit Protection Act with Security Agreements Introduction: In Oklahoma, there are various types of installment sales that are not covered by the Federal Consumer Credit Protection Act (FC CPA) when combined with a security agreement. This article aims to provide a comprehensive understanding of what constitutes an Oklahoma Installment Sale, the importance of the Federal Consumer Credit Protection Act, and the different categories of installment sales exempted under the Act. Keywords: Oklahoma Installment Sale, Federal Consumer Credit Protection Act, FC CPA, Security Agreement 1. Understanding Oklahoma Installment Sales: — Oklahoma Installment Sale refers to a transaction in which a buyer acquires goods or services from a seller and agrees to make payments over a period of time, typically in installments. — The buyer receives immediate possession or use of the goods or services, but ownership is often retained by the seller until the full payment is made. 2. Federal Consumer Credit Protection Act (FC CPA): THCFC CPAPA is a federal law that protects consumers by regulating the consumer credit industry. — It primarily addresses issues such as interest rates, unfair or deceptive practices, credit reporting, debt collection, and disclosure requirements. — However, certain types of installment sales in Oklahoma are not subject to the provisions of the FC CPA due to specific exemptions. 3. Installment Sales Exempted from FC CPA in Oklahoma: a) Agricultural Credit Transactions: — Agriculture-based installment sales involving the financing of agricultural production inputs or equipment used in agricultural operations are among the exemptions. — These sales are designed to facilitate credit for farmers, ranchers, and other professionals engaged in agricultural activities. b) Business-purpose Transactions: — Installment sales made for business purposes, such as the acquisition of assets or services for commercial or industrial use, are exempt from FC CPA coverage. — This exemption aims to ensure that commercial activities are not unduly burdened by consumer credit regulations. c) Real Property Transactions: — Sales or financing arrangements related to real property (land and structures) fall outside the scope of FC CPA coverage. — This exemption applies to both residential and commercial real estate transactions, recognizing the distinct nature of these transactions compared to sales involving movable goods. d) Sales under $25,000: — Installment sales with a credit limit of less than $25,000 are also exempt from FC CPA provisions. — This exemption takes into account smaller transactions where the potential consumer protection issues may be less significant. Conclusion: Understanding the different types of Oklahoma Installment Sales exempted from the Federal Consumer Credit Protection Act is essential for both consumers and businesses. By recognizing these exemptions, consumers can evaluate their rights and protections within various transaction contexts, while businesses can engage in the selling of goods and services for specific purposes without being bound by certain FC CPA requirements. Keywords: Oklahoma Installment Sale, Federal Consumer Credit Protection Act, FC CPA, Security Agreement, exemptions, agricultural credit transactions, business-purpose transactions, real property transactions, sales under $25,000.

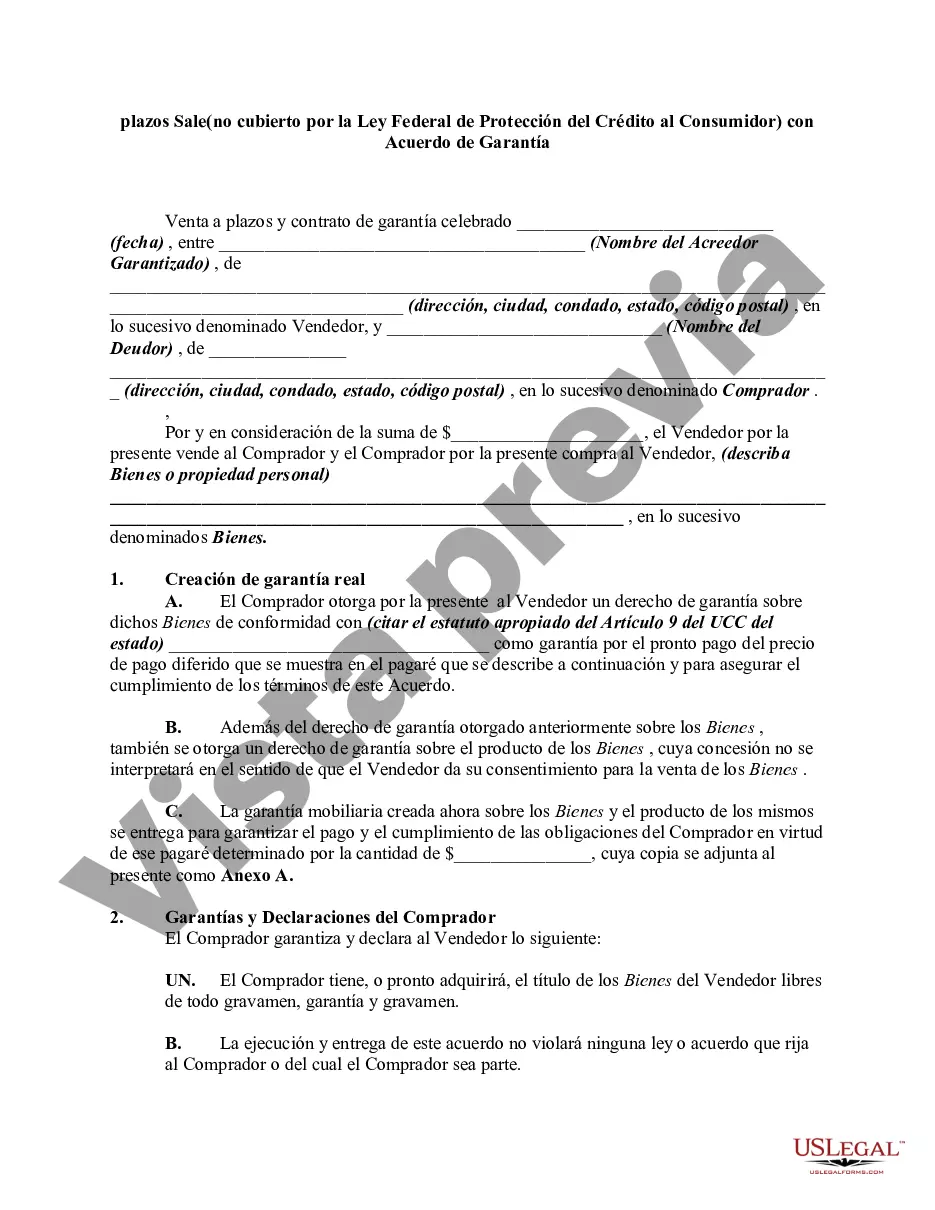

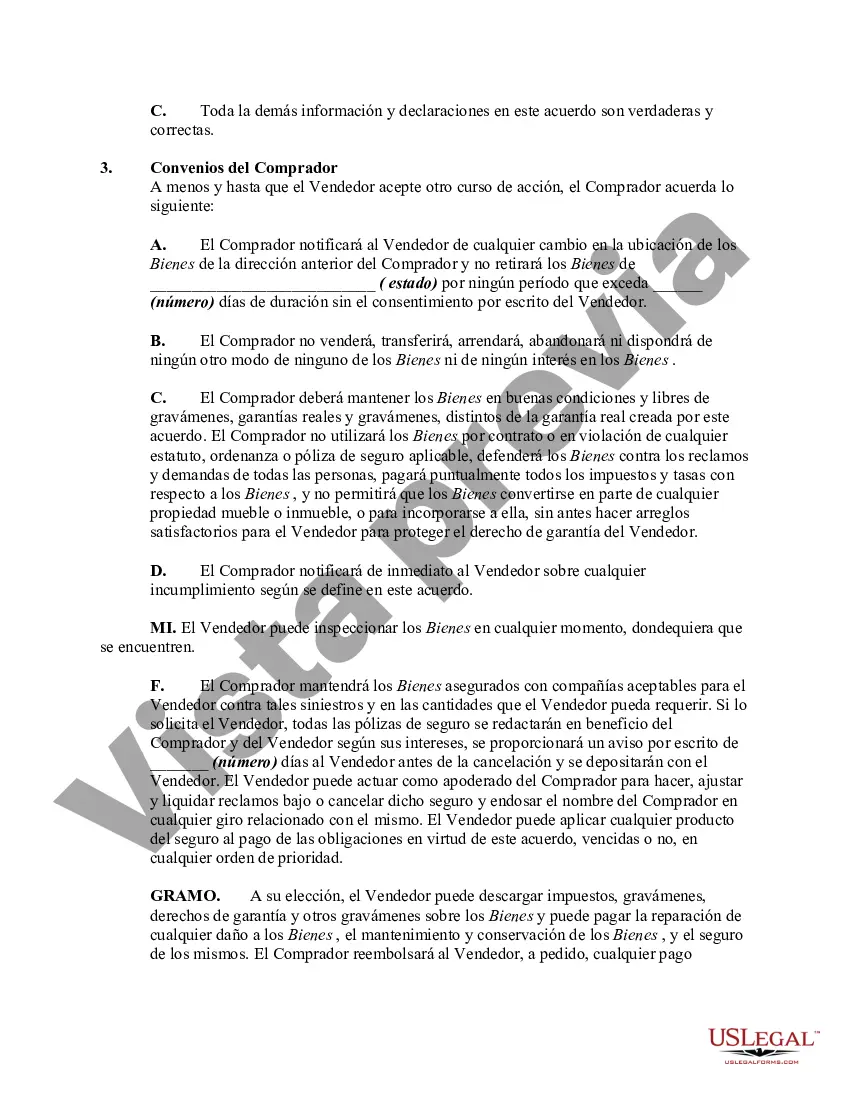

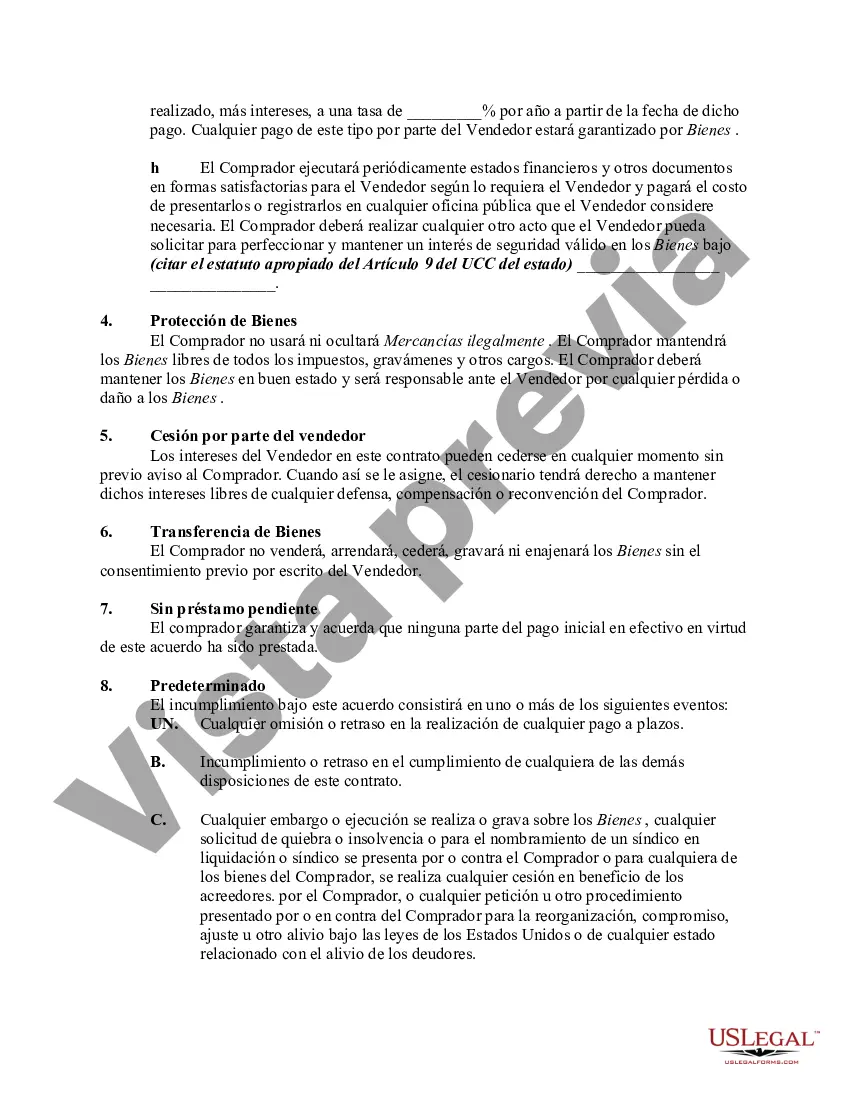

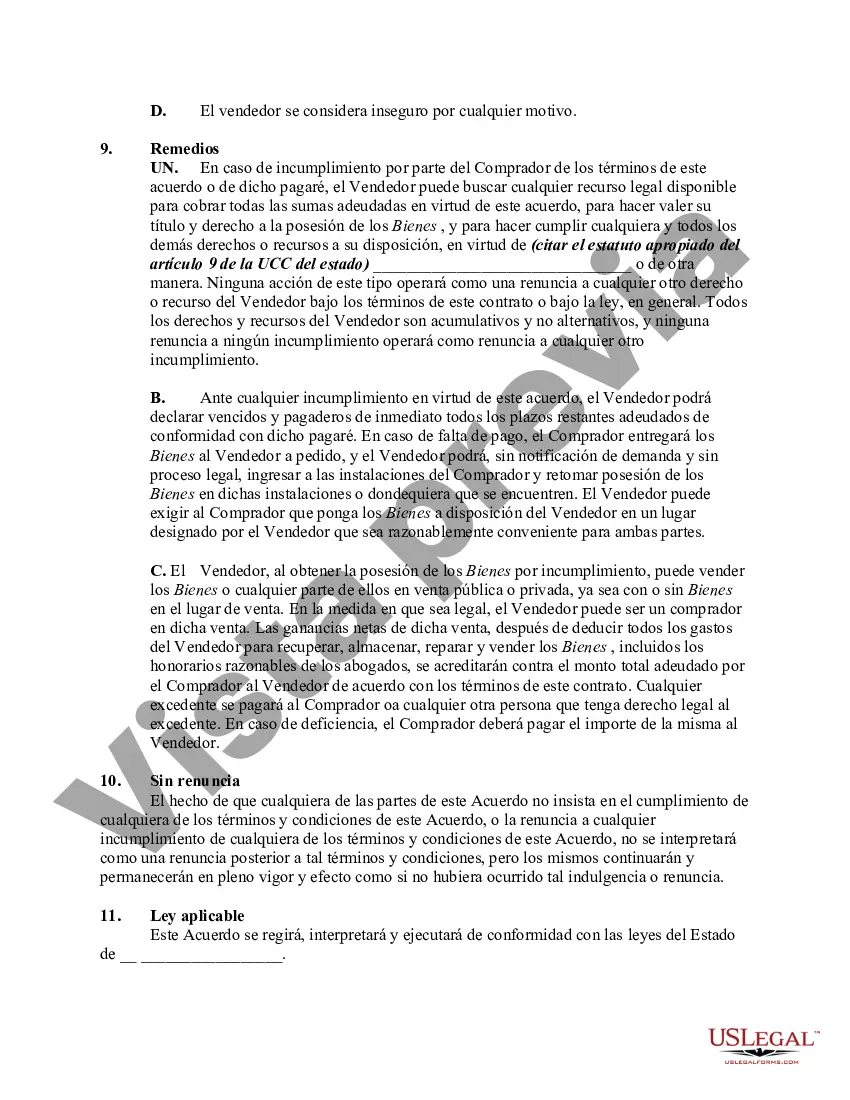

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.