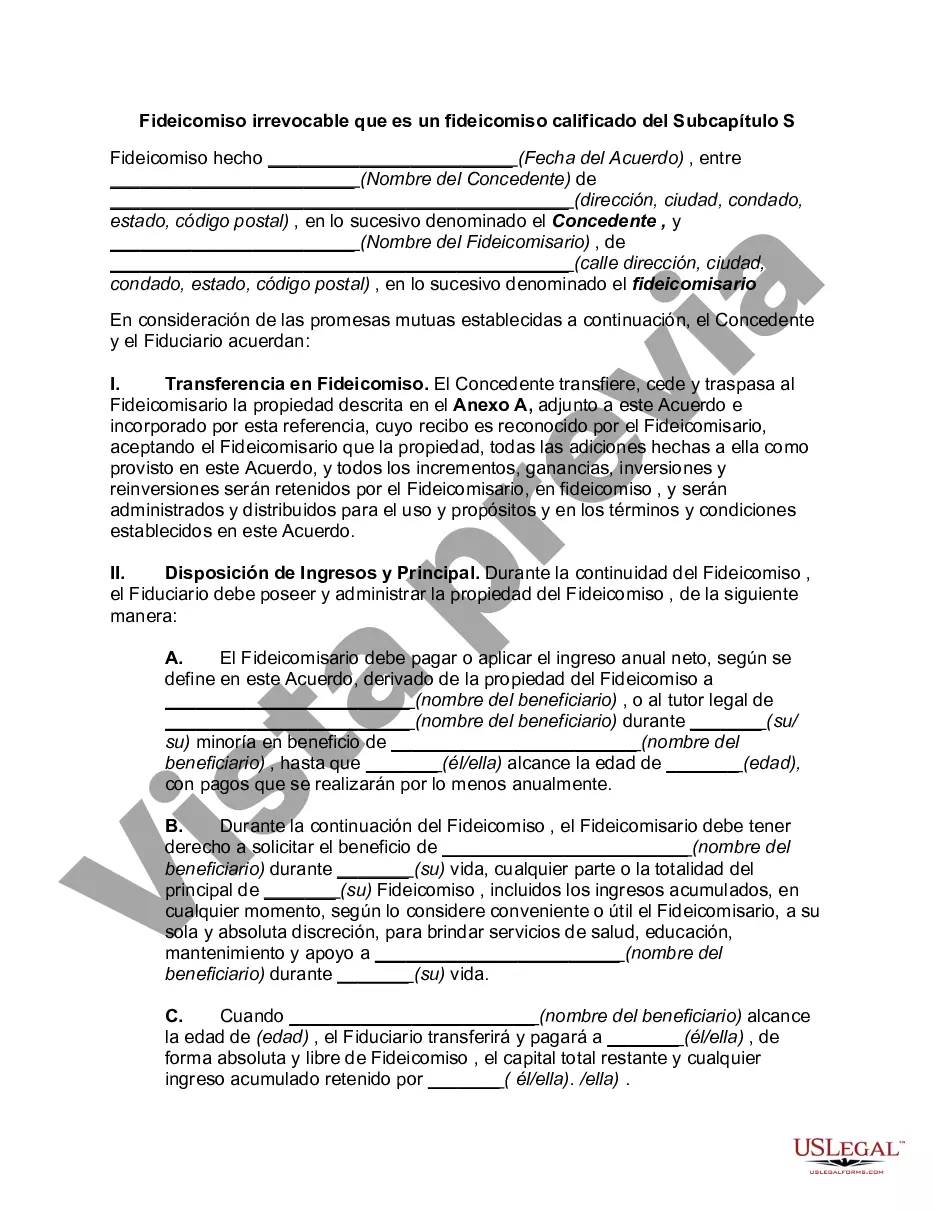

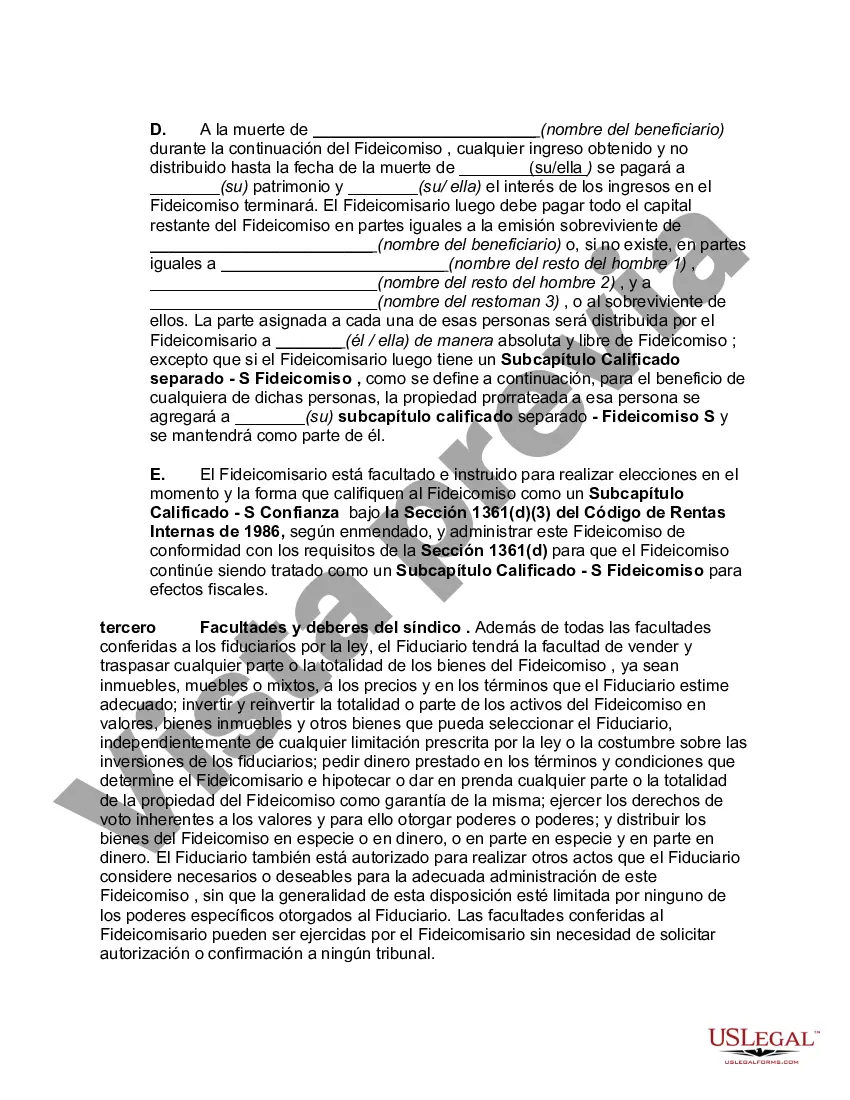

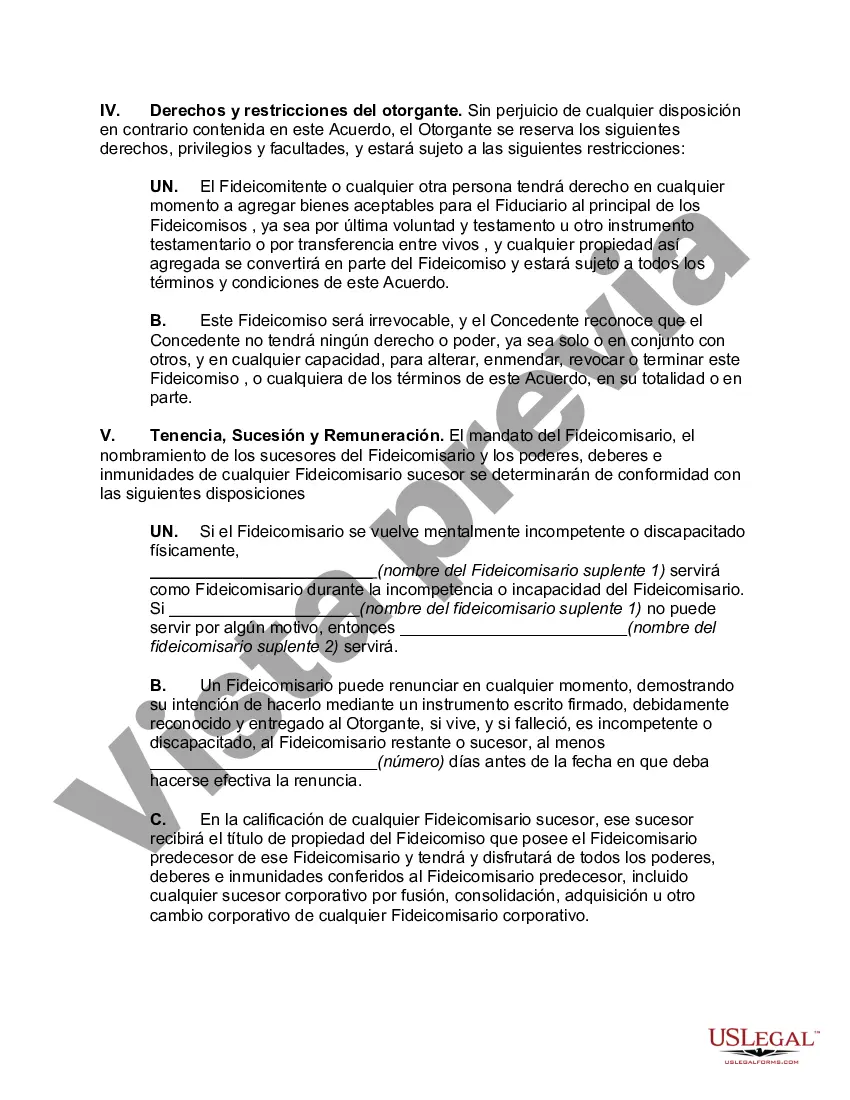

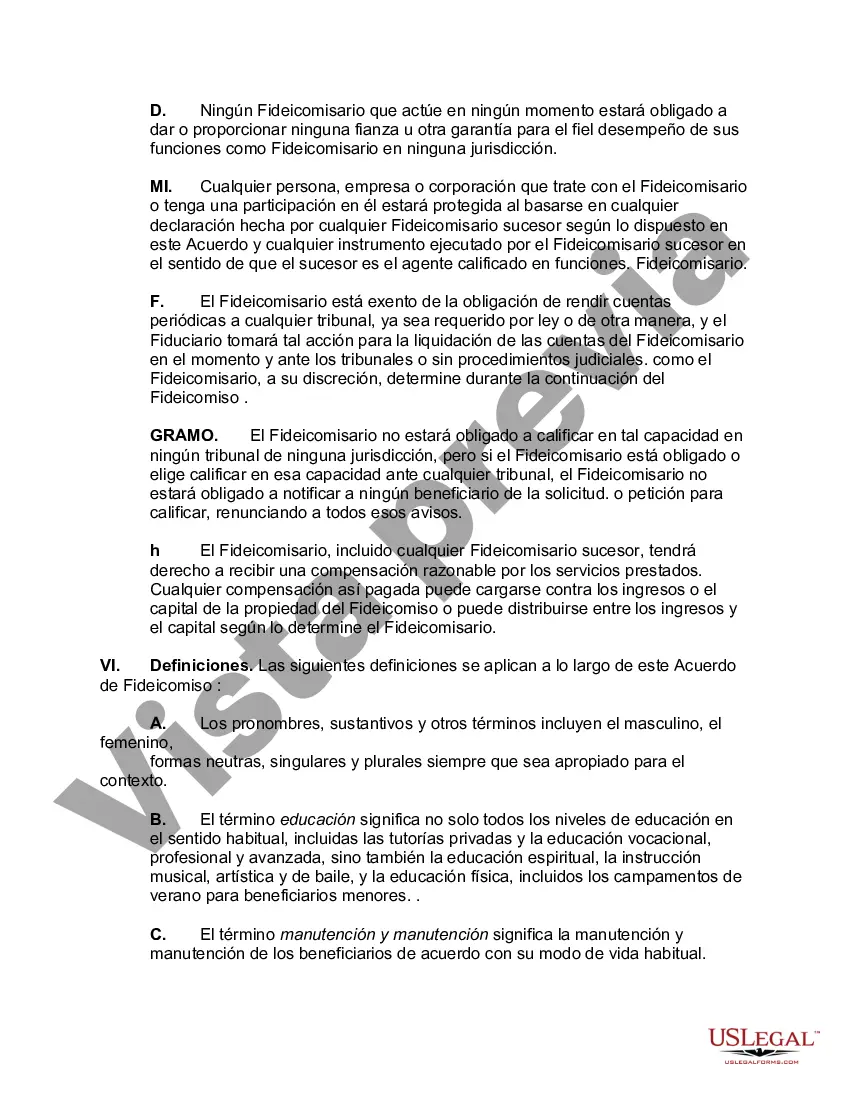

An Oregon Irrevocable Trust, classified as a Qualifying Subchapter-S Trust, is a legal arrangement that provides individuals with various estate planning benefits and tax advantages. It is important to note that while Oregon recognizes Irrevocable Trusts, it does not specifically have a subtype known as a Qualifying Subchapter-S Trust. However, understanding the features and benefits of a Qualifying Subchapter-S Trust in general can still be relevant for estate planning in Oregon. A Qualifying Subchapter-S Trust, often abbreviated as SST, is a type of trust that meets specific criteria set forth by the Internal Revenue Service (IRS) to qualify as an eligible shareholder of an S-corporation. By designating a trust as an SST, the trust can own shares of an S-corporation without jeopardizing the S-corporation's tax status. This trust structure allows for effective estate planning while ensuring the continuance of favorable tax treatment. Keywords: Oregon Irrevocable Trust, Qualifying Subchapter-S Trust, estate planning, tax advantages, legal arrangement, Oregon, Irrevocable Trusts, Qualifying Subchapter-S Trust, SST, Internal Revenue Service, IRS, eligible shareholder, S-corporation, tax status, estate planning.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Oregon Fideicomiso irrevocable que es un fideicomiso calificado del Subcapítulo S - Irrevocable Trust which is a Qualifying Subchapter-S Trust

Description

How to fill out Oregon Fideicomiso Irrevocable Que Es Un Fideicomiso Calificado Del Subcapítulo S?

Discovering the right legitimate papers design can be a have difficulties. Naturally, there are a variety of layouts available online, but how will you discover the legitimate form you require? Use the US Legal Forms internet site. The assistance offers a large number of layouts, including the Oregon Irrevocable Trust which is a Qualifying Subchapter-S Trust, that you can use for company and personal requires. Each of the forms are checked by professionals and meet up with state and federal demands.

In case you are presently listed, log in for your account and then click the Obtain key to have the Oregon Irrevocable Trust which is a Qualifying Subchapter-S Trust. Make use of your account to appear throughout the legitimate forms you have acquired previously. Visit the My Forms tab of your own account and have another copy in the papers you require.

In case you are a brand new customer of US Legal Forms, allow me to share simple guidelines that you should follow:

- Initially, make certain you have selected the right form to your metropolis/region. You can examine the form while using Review key and read the form description to make certain it will be the best for you.

- When the form is not going to meet up with your expectations, make use of the Seach discipline to find the right form.

- When you are positive that the form is acceptable, click the Get now key to have the form.

- Choose the rates plan you need and type in the required information and facts. Create your account and pay for an order with your PayPal account or Visa or Mastercard.

- Opt for the submit structure and acquire the legitimate papers design for your system.

- Total, edit and print out and signal the acquired Oregon Irrevocable Trust which is a Qualifying Subchapter-S Trust.

US Legal Forms is the most significant library of legitimate forms where you will find a variety of papers layouts. Use the company to acquire professionally-created files that follow state demands.