The "look through" trust can affords long term IRA deferrals and special protection or tax benefits for the family. But, as with all specialized tools, you must use it only in the right situation. If the IRA participant names a trust as beneficiary, and the trust meets certain requirements, for purposes of calculating minimum distributions after death, one can "look through" the trust and treat the trust beneficiary as the designated beneficiary of the IRA. You can then use the beneficiary's life expectancy to calculate minimum distributions. Were it not for this "look through" rule, the IRA or plan assets would have to be paid out over a much shorter period after the owner's death, thereby losing long term deferral.

Rhode Island Irrevocable Trust as Designated Beneficiary of an Individual Retirement Account (IRA) An Irrevocable Trust is a legal entity established by an individual, known as the Granter, for the purpose of managing and distributing assets. When an Irrevocable Trust is named as the designated beneficiary of an Individual Retirement Account (IRA) in Rhode Island, it can provide numerous benefits and opportunities for both the Granter and the beneficiaries. One of the primary advantages of utilizing a Rhode Island Irrevocable Trust as the designated beneficiary of an IRA is the potential for tax savings. By designating a trust as the beneficiary, the Granter can control the distribution of assets, ensuring that they are distributed in a tax-efficient manner and in line with their intended wishes. This strategy can help minimize the tax burden on the beneficiaries, as well as potentially reduce the overall estate taxes. There are several types of Rhode Island Irrevocable Trusts that can be designated as beneficiaries of an IRA, each serving a unique purpose: 1. Conduit Trust: This type of trust requires that all distributions received from the IRA must be immediately distributed to the beneficiaries. The conduit trust acts as a pass-through entity, ensuring that the required minimum distributions (Rods) are distributed accordingly. The beneficiaries are then responsible for paying taxes on the distributed funds based on their individual tax rates. 2. Accumulation Trust: Unlike a conduit trust, an accumulation trust allows for the accumulation of funds within the trust. This can be advantageous in situations where the beneficiaries may not be ready to receive a large sum of money all at once, or if the Granter wants to provide for the long-term financial well-being of the beneficiaries. 3. Discretionary Trust: A discretionary trust offers the trustee more flexibility in determining the timing and amount of distributions from the IRA to the beneficiaries. The trustee can consider factors such as the beneficiaries' needs, financial management capabilities, and any potential creditors. This type of trust provides greater asset protection and control over the inherited funds. 4. Standalone Retirement Trust: This trust is designed specifically to be the beneficiary of retirement accounts, including IRAs. It includes specific provisions to meet the requirements set by the Internal Revenue Service (IRS) to ensure tax-efficient distributions. It provides protection from creditors, potential divorces, bankruptcy, and other risks that may jeopardize the inherited funds. Choosing the right type of Rhode Island Irrevocable Trust as the designated beneficiary of an Individual Retirement Account requires careful consideration of the Granter's goals, financial situation, and the needs of the beneficiaries. Consulting with an experienced estate planning attorney who specializes in IRA trusts can help ensure that the trust structure aligns with the Granter's objectives and maximizes the benefits for all parties involved.

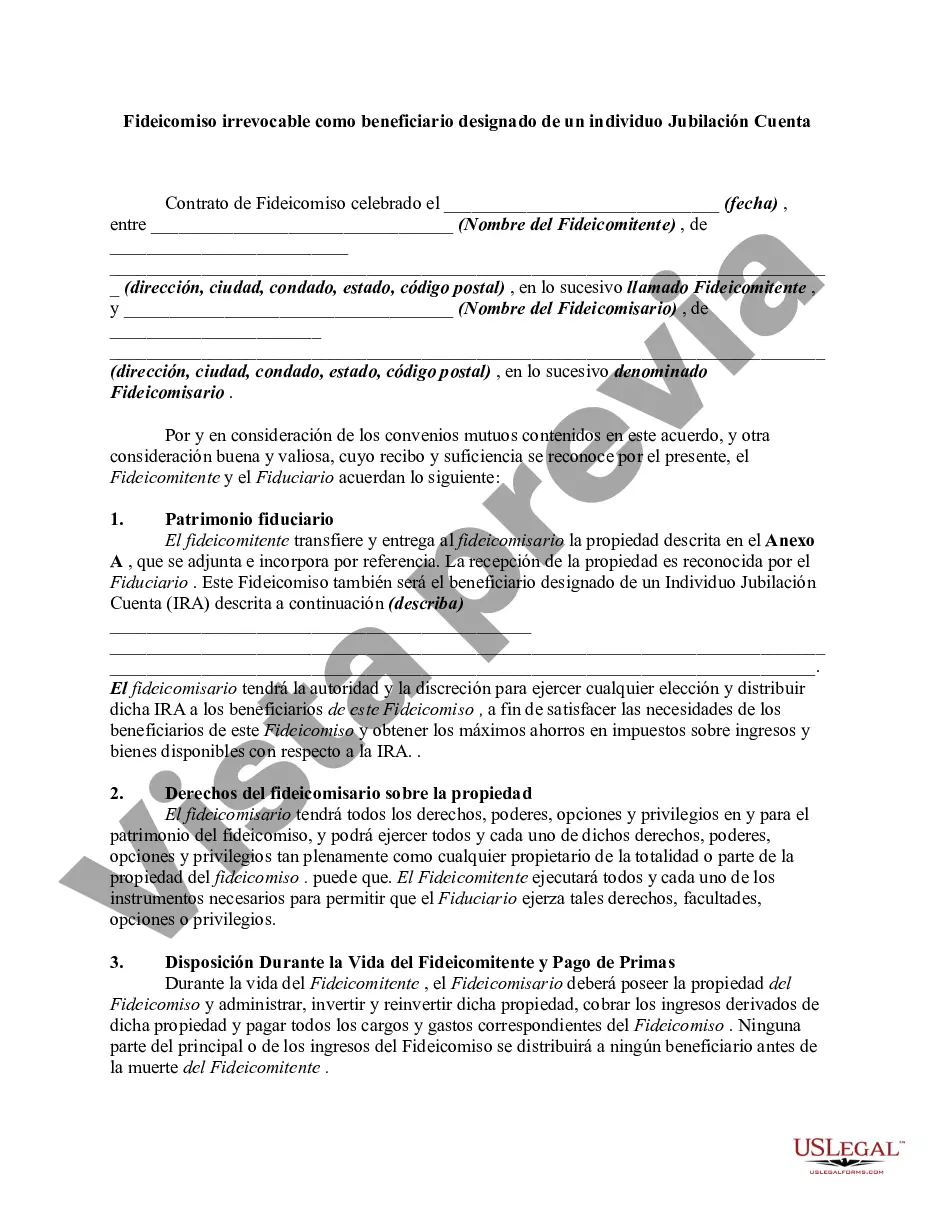

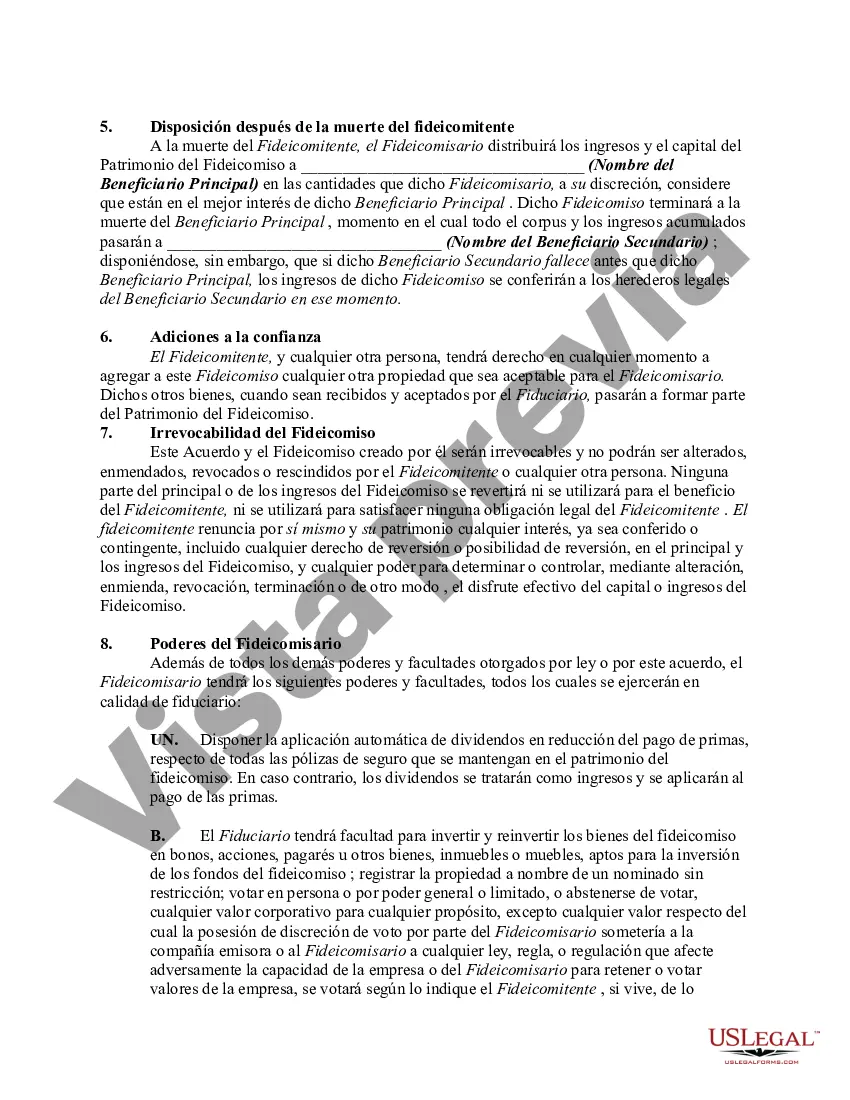

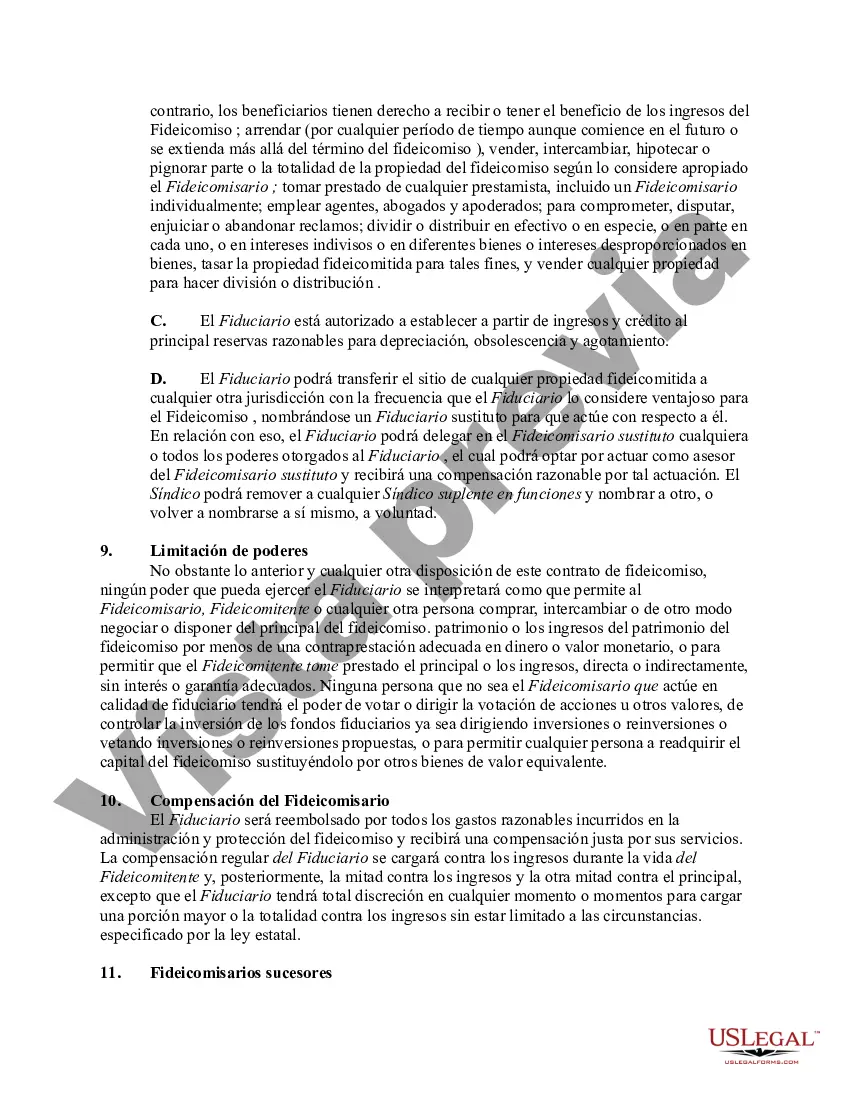

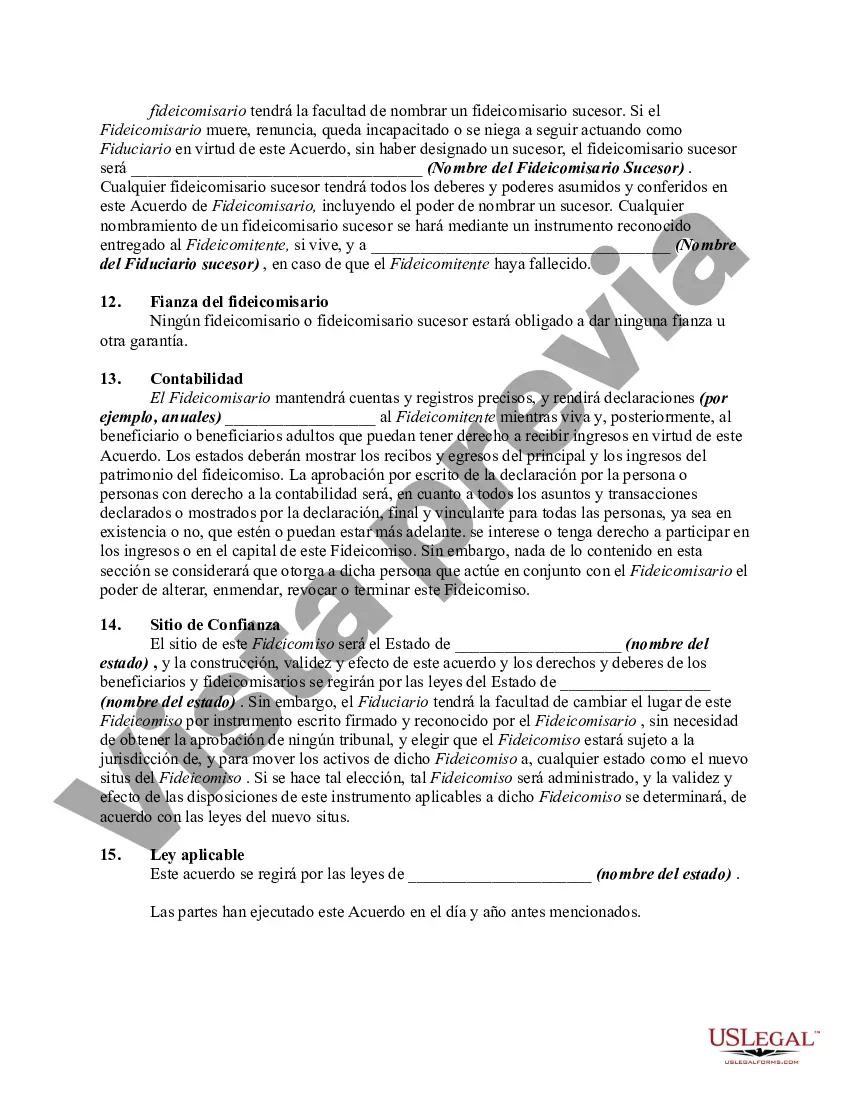

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.