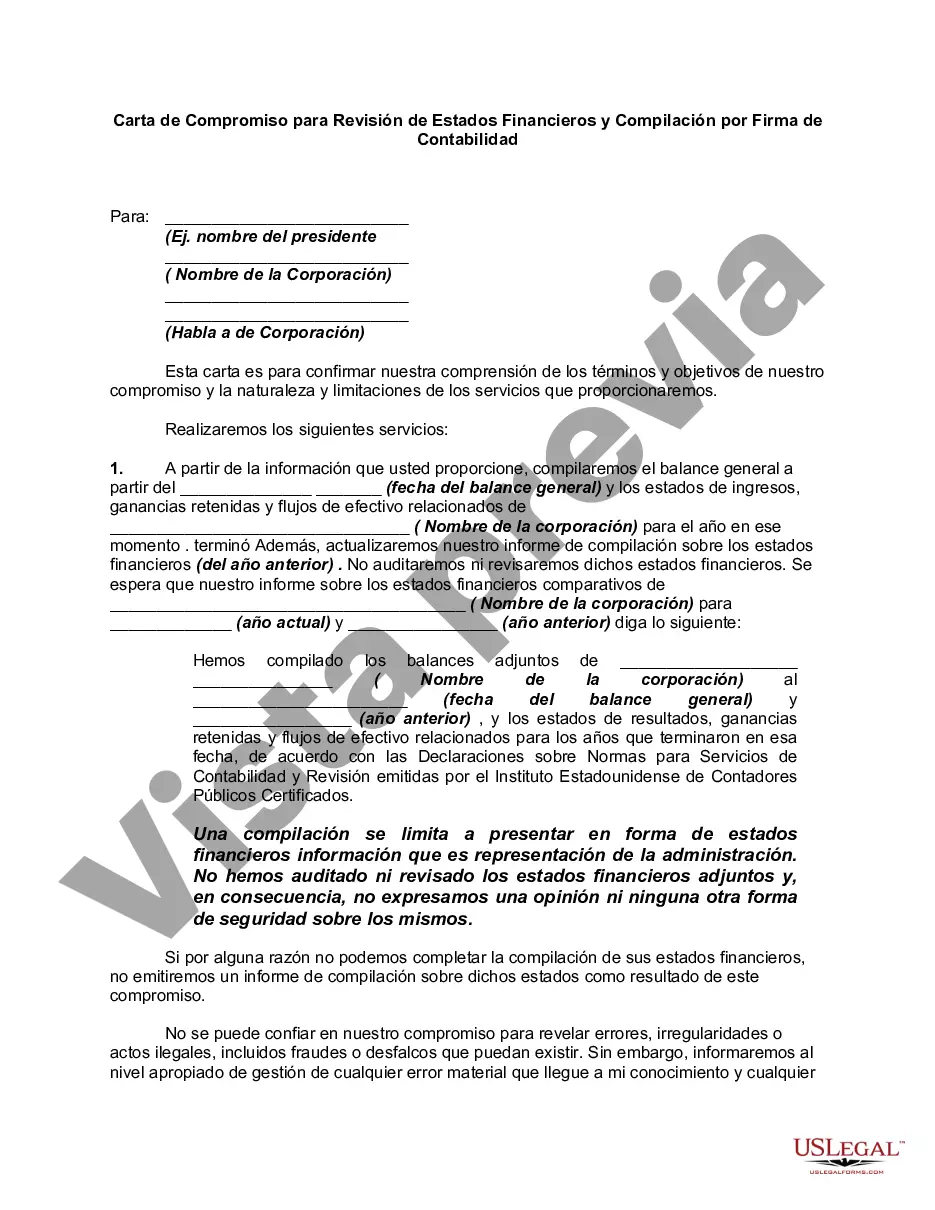

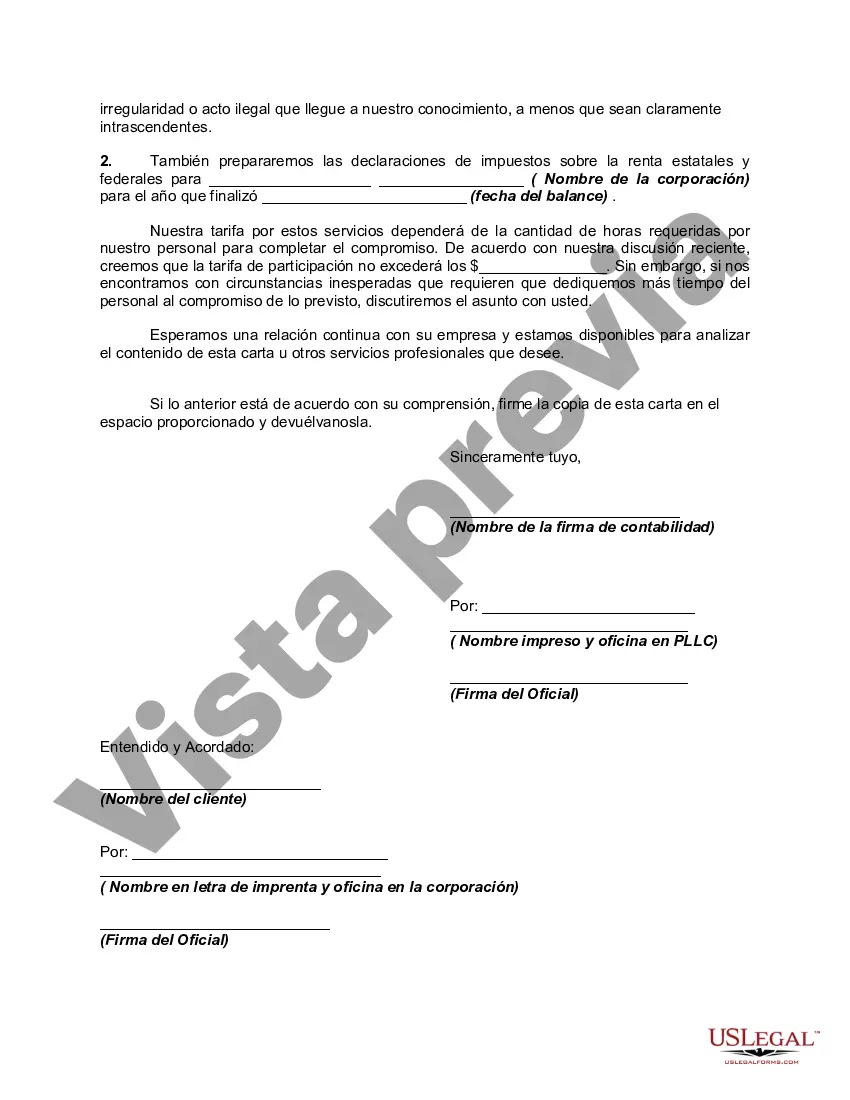

Compiled financial statements represent the most basic level of service that certified public accountants provide with respect to financial statements. In a compilation, the CPA must comply with certain basic requirements of professional standards, such as having a knowledge of the client's industry and applicable accounting principles, having a clear understanding with the client as to the services to be provided, and reading the financial statements to determine whether there are any obvious departures from generally accepted accounting principles (or, in some cases, another comprehensive basis of accounting used by the entity). It may be necessary for the CPA to perform "other accounting services" (such as creating a general ledger for the client, or assisting the client with adjusting entries for the books of the client (before the financial statements can be prepared). Upon completion, a report on the financial statements is issued that states a compilation was performed in accordance with AICPA professional standards, but no assurance is expressed that the statements are in conformity with generally accepted accounting principles. This is known as the expression of "no assurance." Compiled financial statements are often prepared for privately-held entities that do not need a higher level of assurance expressed by the CPA.

Rhode Island Engagement Letter for Review of Financial Statements and Compilation by Accounting Firm An engagement letter is a crucial document used between an accounting firm and a client to outline the scope, responsibilities, and fees involved in conducting a review of financial statements or providing compilation services. In the state of Rhode Island, engagement letters are essential for ensuring a clear understanding of the services being provided, establishing expectations, and mitigating any potential misunderstandings. The Rhode Island Engagement Letter for Review of Financial Statements typically includes the following components: 1. Introduction: The letter begins by formally addressing the client and the accounting firm, and it may also include a brief overview of the client's business or organization. 2. Objective and Scope of the Engagement: This section explicitly outlines the purpose of the engagement, which is the review of the client's financial statements. It would state whether the review is being conducted in accordance with Generally Accepted Accounting Principles (GAAP) or any other applicable standards. The scope of services is clarified, mentioning the specific procedures that will be performed during the review process. 3. Responsibilities of the Client: The engagement letter highlights the client's role in the engagement, such as providing access to relevant financial records, documents, and necessary information within a specified timeframe. It also emphasizes the importance of management's representations being complete and accurate. 4. Responsibilities of the Accounting Firm: This section outlines the responsibilities of the accounting firm, which include conducting the review in accordance with professional standards, consistently applying professional judgment, and expressing an opinion or providing an unbiased report on the financial statements. 5. Reporting: Here, the engagement letter discusses the expected form and content of the reporting. It specifies whether the accounting firm will issue a written report expressing limited assurance or an adverse opinion if material misstatements are identified. 6. Legal and Ethical Considerations: This part of the engagement letter highlights the accounting firm's commitment to comply with legal and ethical requirements, including maintaining confidentiality and independence. It may also touch upon any potential limitations or restrictions on liability. 7. Fees and Payment: This section outlines the basis and method of determining fees, payment terms, and any additional costs that may arise during the engagement, such as travel expenses or data retrieval. 8. Termination of Engagement: This clause specifies the circumstances under which either party can terminate the engagement, such as non-payment, breach of contract, or non-cooperation. It also discusses the consequences of termination for both parties. Rhode Island may have different types of engagement letters, tailored to specific services or industries. Some variations could include: 1. Rhode Island Engagement Letter for Review of Financial Statements — Not-for-Profit Organizations: This type of engagement letter caters specifically to not-for-profit organizations, taking into account the unique reporting requirements and regulations applicable to such entities. 2. Rhode Island Engagement Letter for Review of Financial Statements — Small Businesses: Designed for small businesses, this engagement letter focuses on the specific needs and considerations of small-scale enterprises, perhaps with simplified reporting standards. In conclusion, the Rhode Island Engagement Letter for Review of Financial Statements and Compilation by an Accounting Firm is a comprehensive document that outlines the scope, responsibilities, and expectations of both the accounting firm and the client. It ensures transparency, establishes a professional relationship, and sets the stage for a successful financial review or compilation engagement.Rhode Island Engagement Letter for Review of Financial Statements and Compilation by Accounting Firm An engagement letter is a crucial document used between an accounting firm and a client to outline the scope, responsibilities, and fees involved in conducting a review of financial statements or providing compilation services. In the state of Rhode Island, engagement letters are essential for ensuring a clear understanding of the services being provided, establishing expectations, and mitigating any potential misunderstandings. The Rhode Island Engagement Letter for Review of Financial Statements typically includes the following components: 1. Introduction: The letter begins by formally addressing the client and the accounting firm, and it may also include a brief overview of the client's business or organization. 2. Objective and Scope of the Engagement: This section explicitly outlines the purpose of the engagement, which is the review of the client's financial statements. It would state whether the review is being conducted in accordance with Generally Accepted Accounting Principles (GAAP) or any other applicable standards. The scope of services is clarified, mentioning the specific procedures that will be performed during the review process. 3. Responsibilities of the Client: The engagement letter highlights the client's role in the engagement, such as providing access to relevant financial records, documents, and necessary information within a specified timeframe. It also emphasizes the importance of management's representations being complete and accurate. 4. Responsibilities of the Accounting Firm: This section outlines the responsibilities of the accounting firm, which include conducting the review in accordance with professional standards, consistently applying professional judgment, and expressing an opinion or providing an unbiased report on the financial statements. 5. Reporting: Here, the engagement letter discusses the expected form and content of the reporting. It specifies whether the accounting firm will issue a written report expressing limited assurance or an adverse opinion if material misstatements are identified. 6. Legal and Ethical Considerations: This part of the engagement letter highlights the accounting firm's commitment to comply with legal and ethical requirements, including maintaining confidentiality and independence. It may also touch upon any potential limitations or restrictions on liability. 7. Fees and Payment: This section outlines the basis and method of determining fees, payment terms, and any additional costs that may arise during the engagement, such as travel expenses or data retrieval. 8. Termination of Engagement: This clause specifies the circumstances under which either party can terminate the engagement, such as non-payment, breach of contract, or non-cooperation. It also discusses the consequences of termination for both parties. Rhode Island may have different types of engagement letters, tailored to specific services or industries. Some variations could include: 1. Rhode Island Engagement Letter for Review of Financial Statements — Not-for-Profit Organizations: This type of engagement letter caters specifically to not-for-profit organizations, taking into account the unique reporting requirements and regulations applicable to such entities. 2. Rhode Island Engagement Letter for Review of Financial Statements — Small Businesses: Designed for small businesses, this engagement letter focuses on the specific needs and considerations of small-scale enterprises, perhaps with simplified reporting standards. In conclusion, the Rhode Island Engagement Letter for Review of Financial Statements and Compilation by an Accounting Firm is a comprehensive document that outlines the scope, responsibilities, and expectations of both the accounting firm and the client. It ensures transparency, establishes a professional relationship, and sets the stage for a successful financial review or compilation engagement.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.