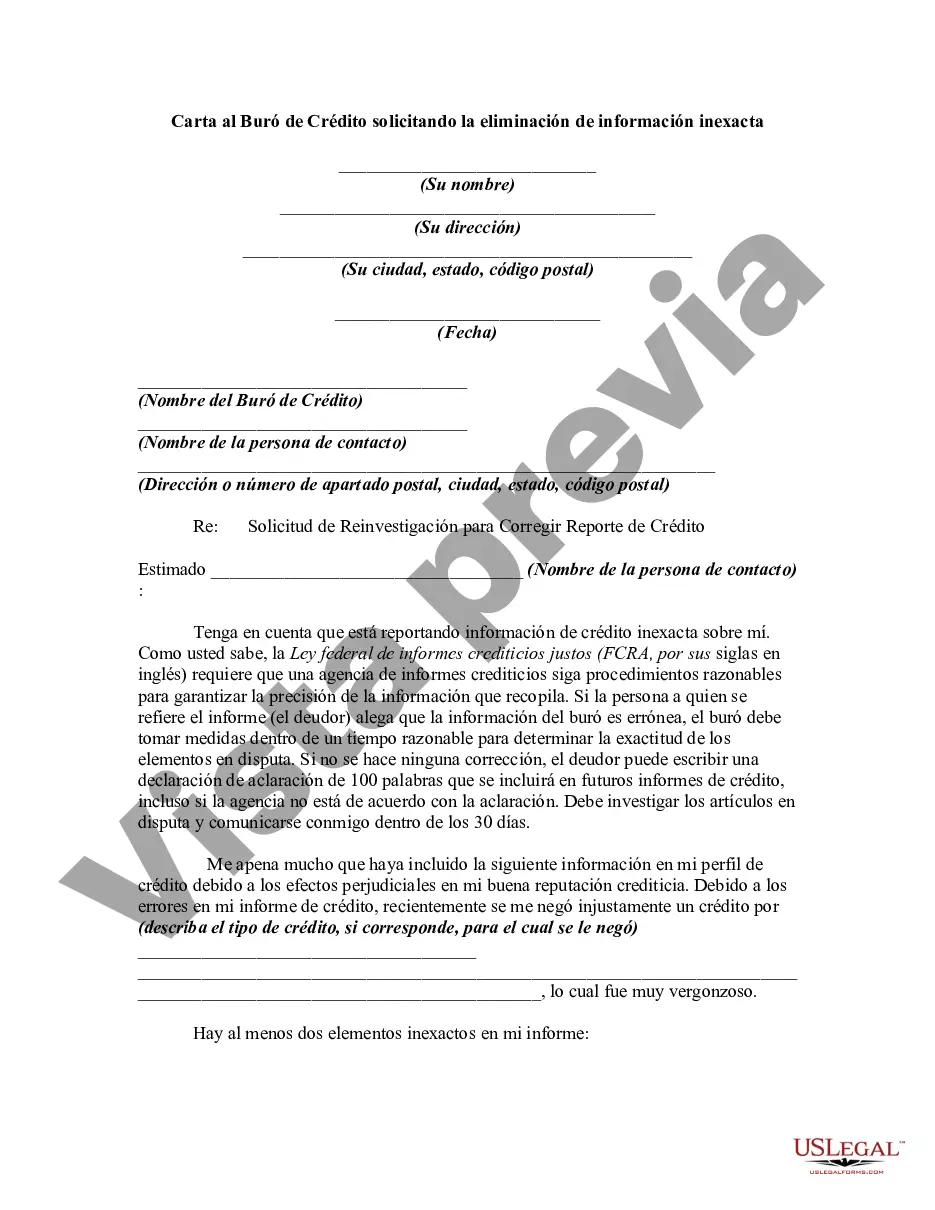

This form is a sample letter requesting the removal of inaccurate information. Always include any copies of proof you may have (e.g., copies of cancelled checks showing timely payments). If the person claims that the information of the bureau is erroneous, the bureau must take steps within a reasonable time to determine the accuracy of the disputed items. If no correction is made, the debtor can write a 100 word statement of clarification which will be included in future credit reports, even it the agency disagrees with clarification.

Title: South Carolina Letter to Credit Bureau Requesting the Removal of Inaccurate Information Introduction: In South Carolina, consumers have the right to dispute inaccurate information on their credit reports. A letter to a credit bureau in South Carolina is an effective method for individuals to request the removal of any erroneous or outdated data from their credit profiles. This comprehensive guide will outline the necessary steps and provide a template to help you craft a well-structured South Carolina letter to credit bureaus to dispute inaccuracies. Key Keywords: South Carolina, letter, credit bureau, requesting removal, inaccurate information I. Understanding the Importance of Accuracy in Credit Reports — South Carolina consumers need accurate credit reports for financial stability and opportunities. — Inaccurate information can negatively impact credit scores, loan approvals, and interest rates. — The Fair Credit Reporting Act (FCRA) empowers consumers to dispute errors to credit bureaus. II. Types of South Carolina Letters to Credit Bureaus 1. Dispute Letter: This type of letter is used to challenge the accuracy of specific information on a credit report, such as incorrect personal details, account discrepancies, or unauthorized activities. 2. Debt Validation Letter: If South Carolina consumers believe they hold no responsibility for a particular debt, they can request validation from the credit bureau. This letter ensures the debt is justified before further collection actions are pursued. III. Crafting an Effective South Carolina Letter to Credit Bureaus 1. Personal Information: Include your full name, address, contact details, and social security number to ensure proper identification. 2. Date: Add the current date to establish the timeline of the dispute process. 3. Credit Bureau Information: Identify the specific credit bureau or bureaus (Equifax, Experian, TransUnion) that contain the inaccurate information. 4. Detailed Description: Clearly identify and explain the inaccurate information, including any supporting evidence or documents. 5. Dispute Request: Assert your rights under the FCRA and request the immediate removal or correction of the inaccurate information. 6. Supporting Documents: Enclose copies of any relevant documents supporting your dispute, such as payment receipts or identification documents. 7. Request Confirmation: Ask for written confirmation of the correction/removal within the time frame stipulated by the FCRA (typically 30 days). IV. Conclusion: By composing a well-crafted South Carolina letter to credit bureaus, consumers can assert their rights and initiate the process of rectifying any inaccurate information on their credit reports. It is crucial to remain patient during the dispute resolution process while retaining copies of all correspondences for personal records. Remember, accuracy in credit reporting is vital, and South Carolinians should take advantage of their rights to ensure their financial well-being. Keywords: South Carolina letter to credit bureaus, dispute errors, credit report accuracy, Fair Credit Reporting Act (FCRA), debt validation letter, personal information, credit bureau information, detailed description, dispute request, supporting documents, request confirmation. (Note: The specific types of South Carolina letters to credit bureaus may vary depending on the type of issue being addressed, but the primary focus remains on disputing inaccurate information.)Title: South Carolina Letter to Credit Bureau Requesting the Removal of Inaccurate Information Introduction: In South Carolina, consumers have the right to dispute inaccurate information on their credit reports. A letter to a credit bureau in South Carolina is an effective method for individuals to request the removal of any erroneous or outdated data from their credit profiles. This comprehensive guide will outline the necessary steps and provide a template to help you craft a well-structured South Carolina letter to credit bureaus to dispute inaccuracies. Key Keywords: South Carolina, letter, credit bureau, requesting removal, inaccurate information I. Understanding the Importance of Accuracy in Credit Reports — South Carolina consumers need accurate credit reports for financial stability and opportunities. — Inaccurate information can negatively impact credit scores, loan approvals, and interest rates. — The Fair Credit Reporting Act (FCRA) empowers consumers to dispute errors to credit bureaus. II. Types of South Carolina Letters to Credit Bureaus 1. Dispute Letter: This type of letter is used to challenge the accuracy of specific information on a credit report, such as incorrect personal details, account discrepancies, or unauthorized activities. 2. Debt Validation Letter: If South Carolina consumers believe they hold no responsibility for a particular debt, they can request validation from the credit bureau. This letter ensures the debt is justified before further collection actions are pursued. III. Crafting an Effective South Carolina Letter to Credit Bureaus 1. Personal Information: Include your full name, address, contact details, and social security number to ensure proper identification. 2. Date: Add the current date to establish the timeline of the dispute process. 3. Credit Bureau Information: Identify the specific credit bureau or bureaus (Equifax, Experian, TransUnion) that contain the inaccurate information. 4. Detailed Description: Clearly identify and explain the inaccurate information, including any supporting evidence or documents. 5. Dispute Request: Assert your rights under the FCRA and request the immediate removal or correction of the inaccurate information. 6. Supporting Documents: Enclose copies of any relevant documents supporting your dispute, such as payment receipts or identification documents. 7. Request Confirmation: Ask for written confirmation of the correction/removal within the time frame stipulated by the FCRA (typically 30 days). IV. Conclusion: By composing a well-crafted South Carolina letter to credit bureaus, consumers can assert their rights and initiate the process of rectifying any inaccurate information on their credit reports. It is crucial to remain patient during the dispute resolution process while retaining copies of all correspondences for personal records. Remember, accuracy in credit reporting is vital, and South Carolinians should take advantage of their rights to ensure their financial well-being. Keywords: South Carolina letter to credit bureaus, dispute errors, credit report accuracy, Fair Credit Reporting Act (FCRA), debt validation letter, personal information, credit bureau information, detailed description, dispute request, supporting documents, request confirmation. (Note: The specific types of South Carolina letters to credit bureaus may vary depending on the type of issue being addressed, but the primary focus remains on disputing inaccurate information.)

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.