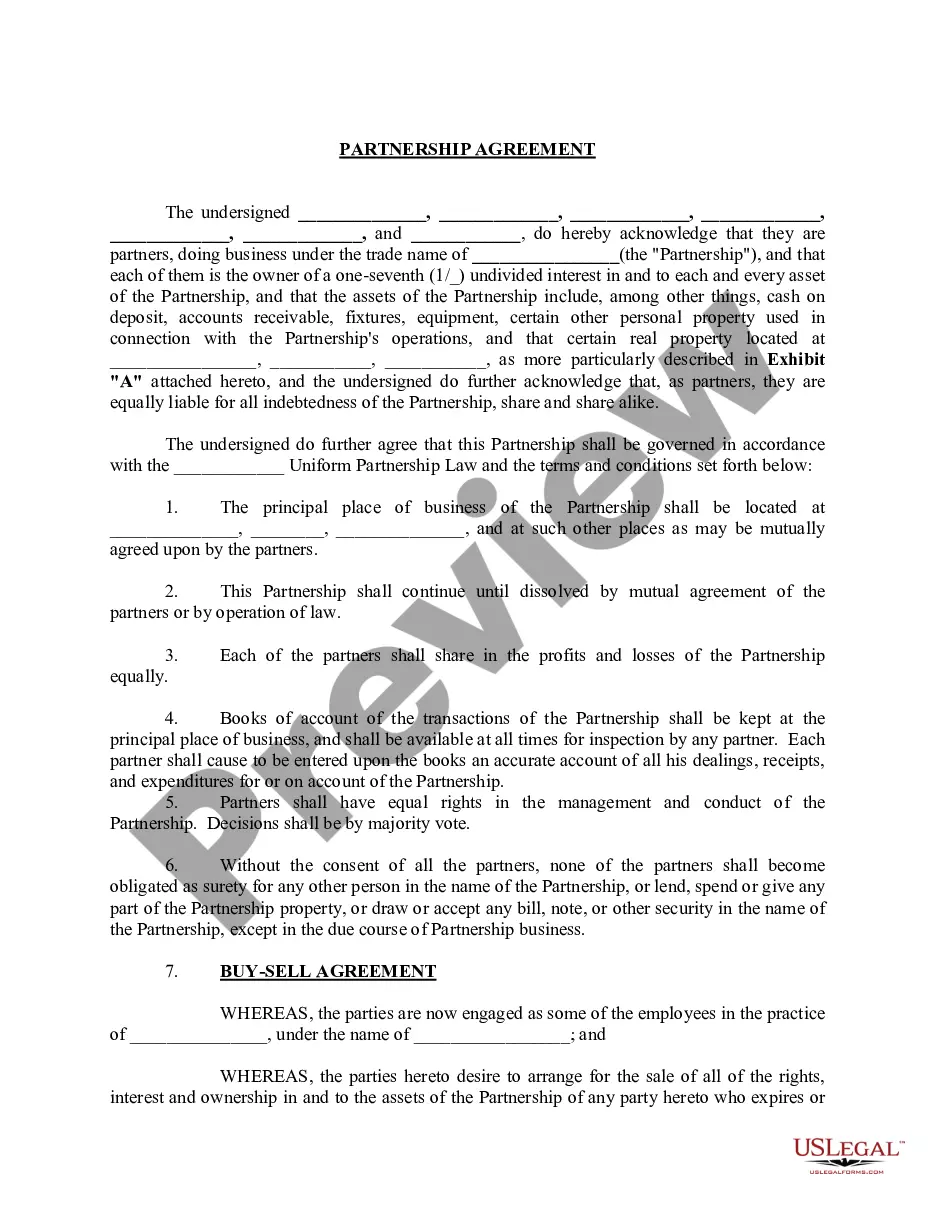

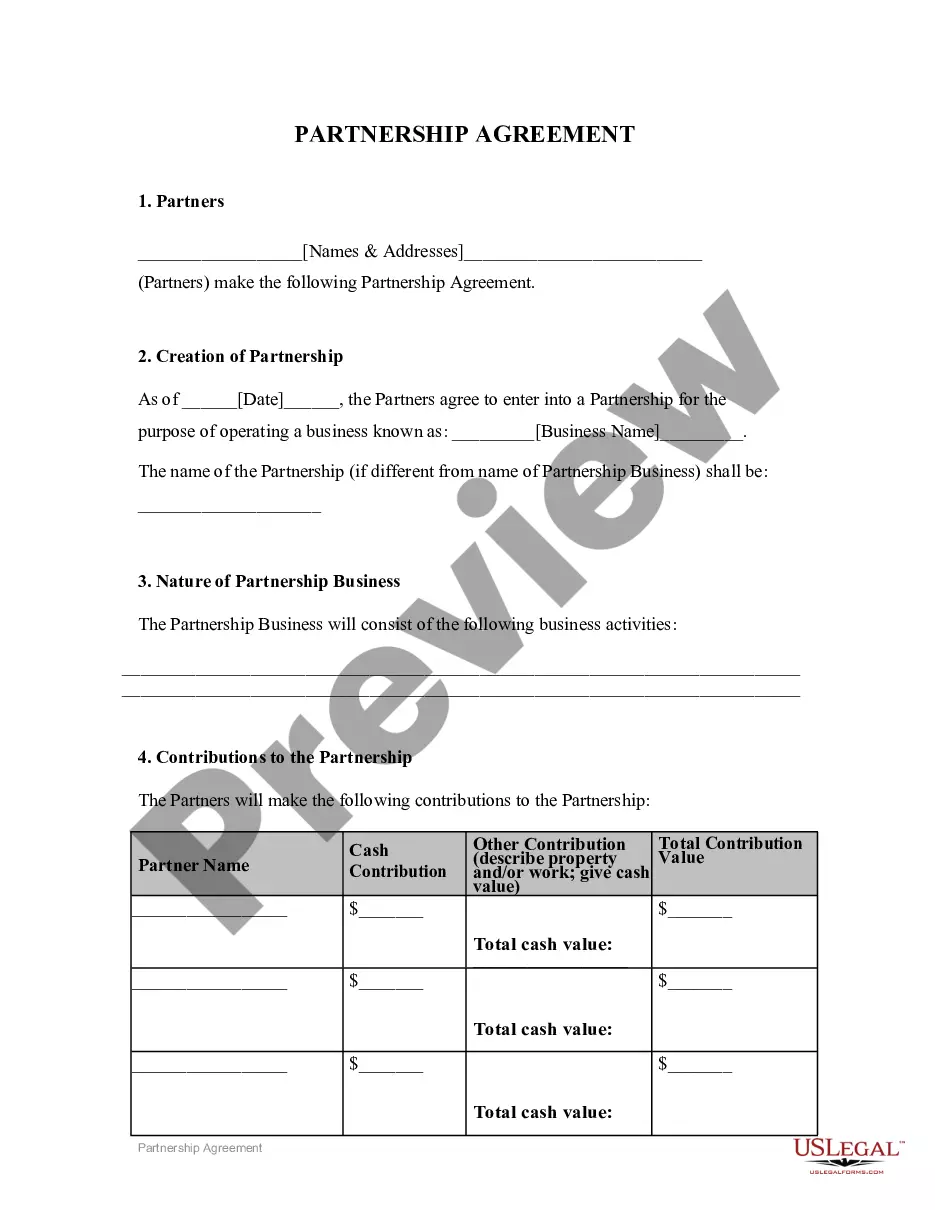

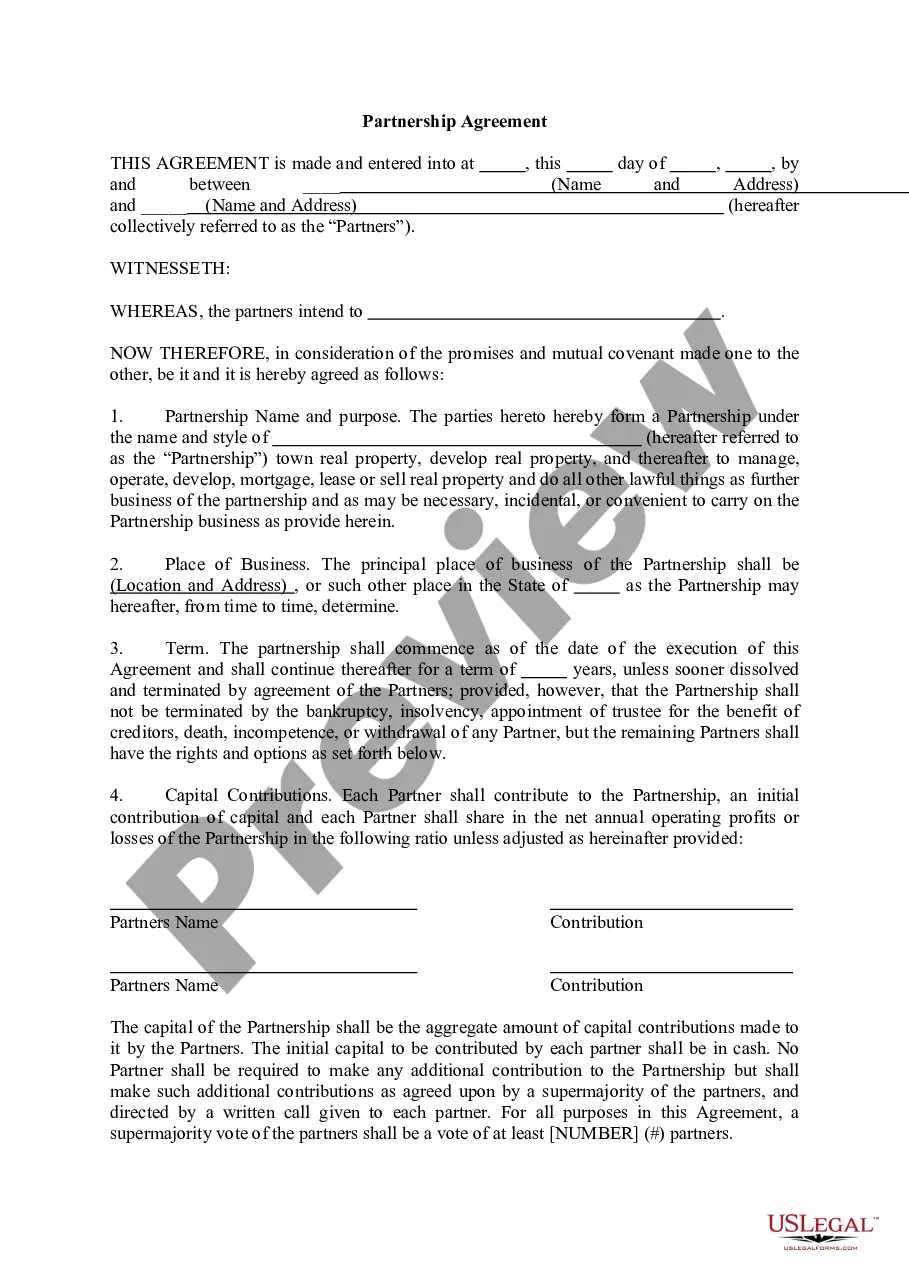

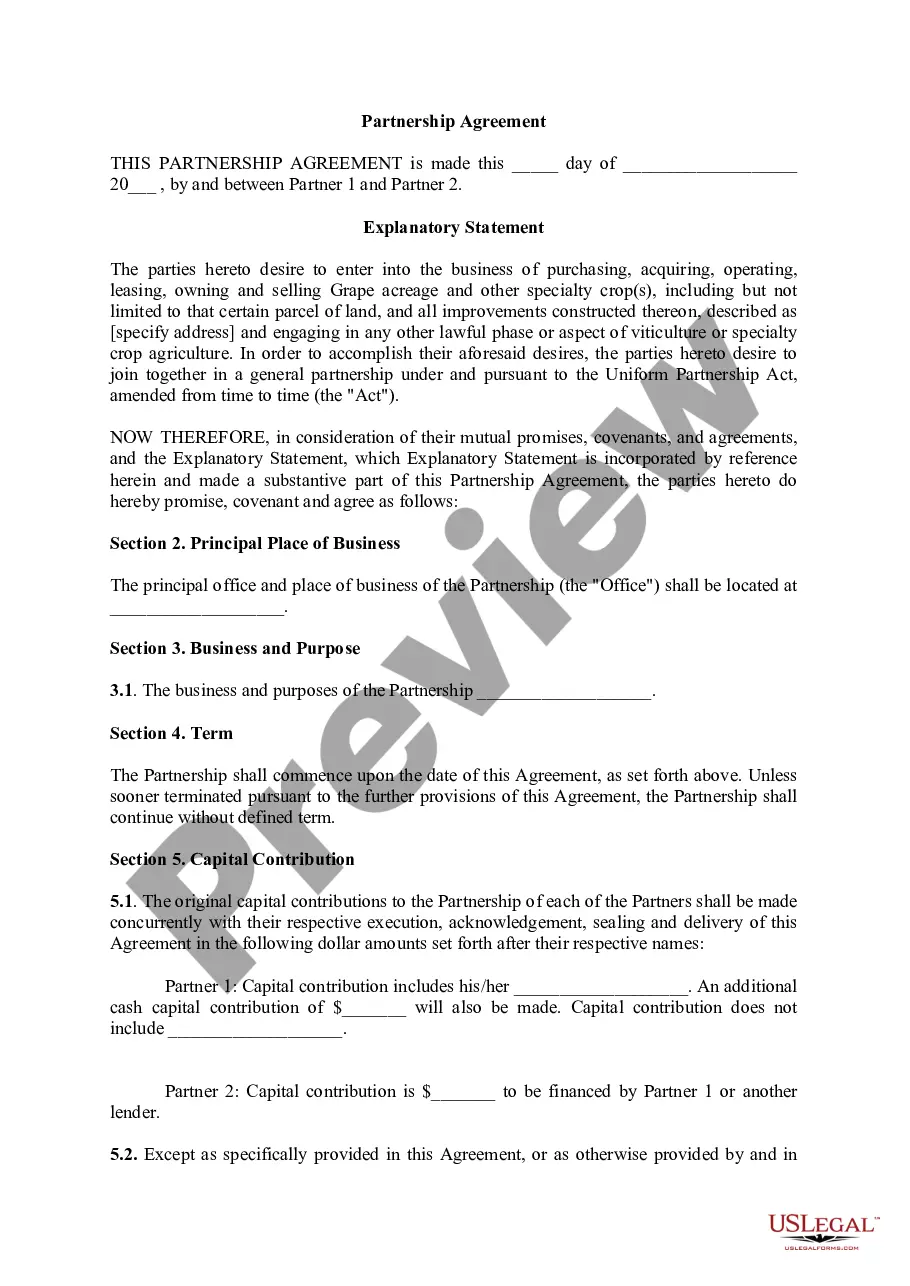

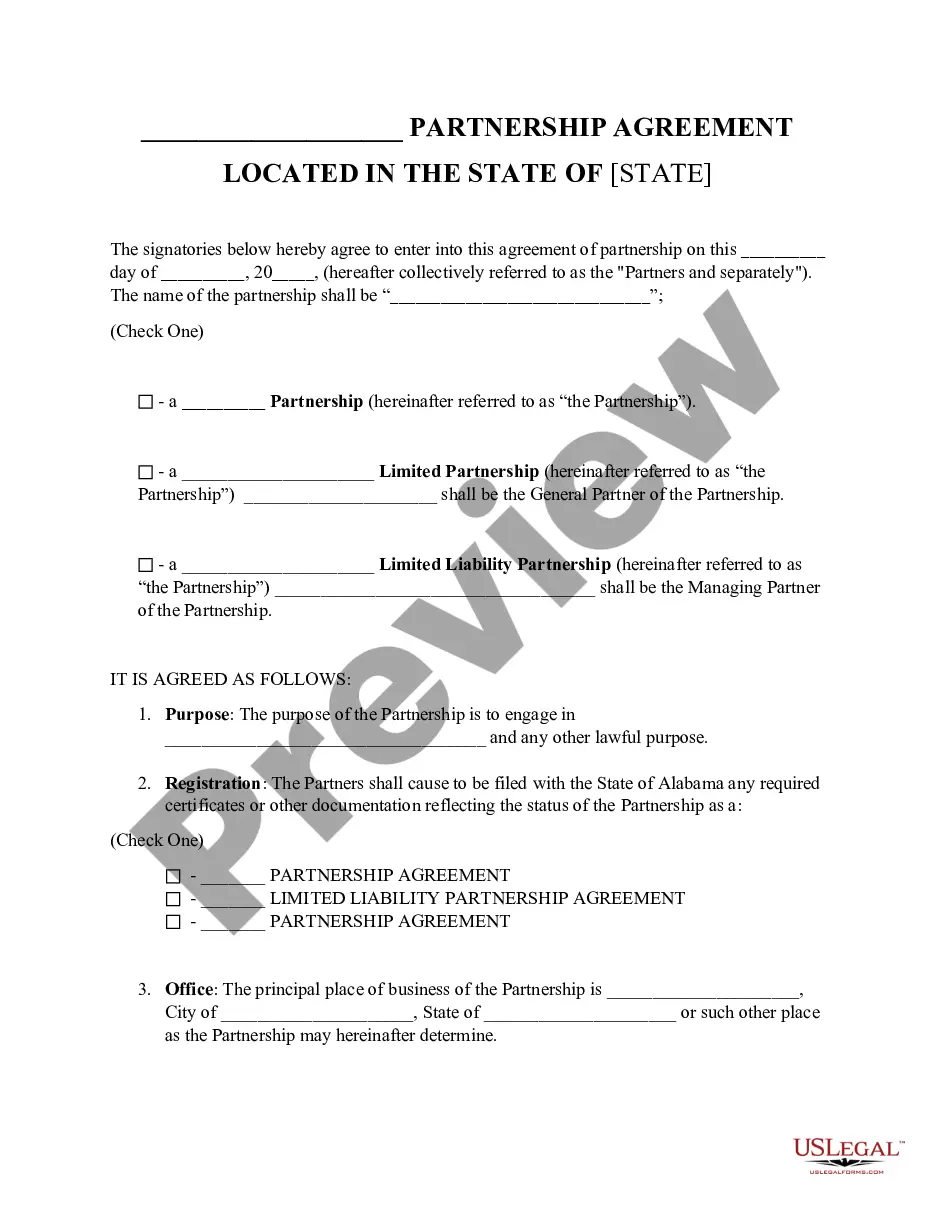

Partnership agreements are written documents that explicitly detail the relationship between the business partners and their individual obligations and contributions to the partnership. Since partnership agreements should cover all possible business situations that could arise during the partnership's life, the documents are often complex; legal counsel in drafting and reviewing the finished contract is generally recommended. If a partnership does not have a partnership agreement in place when it dissolves, the guidelines of the Uniform Partnership Act and various state laws will determine how the assets and debts of the partnership are distributed.

South Carolina Partnership Agreement Between Accountants

Instant download

Description

Free preview

How to fill out Partnership Agreement Between Accountants?

If you wish to finalize, obtain, or print lawful documents templates, utilize US Legal Forms, the largest collection of legal forms available online.

Employ the site's straightforward and user-friendly search to find the documents you require.

A selection of templates for business and personal purposes are organized by categories and states, or keywords.

Step 4. After you have found the form you need, click on the Buy now button. Choose the payment plan you prefer and enter your information to register on an account.

Step 5. Complete the transaction. You can use your Visa, Mastercard, or PayPal account to finalize the purchase.

- Utilize US Legal Forms to acquire the South Carolina Partnership Agreement Between Accountants in just a few clicks.

- If you are already a US Legal Forms client, Log In to your account and click the Acquire button to access the South Carolina Partnership Agreement Between Accountants.

- You can also access forms you previously saved in the My documents section of your account.

- If you are using US Legal Forms for the first time, refer to the instructions provided below.

- Step 1. Ensure you have selected the form for the correct city/state.

- Step 2. Use the Preview option to examine the form’s details. Don't forget to review the description.

- Step 3. If you are not satisfied with the form, use the Search area at the top of the screen to find other types of your legal form template.

Form popularity

FAQ

The meaning of a partnership agreement refers to a legal document that defines the relationship between business partners. This agreement aligns all parties on expectations, contributions, and management roles. It serves not only to protect individual interests but also to enhance cooperation towards common goals. In the context of the South Carolina Partnership Agreement Between Accountants, this document becomes even more significant for accountants seeking a successful partnership.

The main purpose of a partnership agreement is to clearly outline the terms of the relationship between partners. It minimizes misunderstandings by specifying each partner's roles, responsibilities, and profit distribution. This legal document acts as a safeguard against disputes, promoting a healthy working environment. When creating a South Carolina Partnership Agreement Between Accountants, it is essential to address key elements that suit your specific business needs.

A partnership agreement in accounting serves as a written agreement that formalizes the collaboration between accountants. It typically includes information about ownership percentages, financial contributions, and methods for resolving disagreements. This document is vital for establishing expectations and fostering mutual understanding among partners. A South Carolina Partnership Agreement Between Accountants ensures you are properly aligned and prepares you for future challenges.

An example of a partnership agreement could involve two accountants forming a business to provide tax services collaboratively. The agreement would detail profit sharing, decision-making processes, and conflict resolution methods. This clear framework helps each party know their rights and obligations, which contributes to a harmonious working relationship. For accountants in South Carolina, a customized South Carolina Partnership Agreement Between Accountants is crucial to laying out these specifics.

The General Partnership Act in South Carolina governs the formation and operation of partnerships in the state. It sets forth the legal standards and required provisions for partnership agreements, including liability and management structures. Understanding this act is essential for accountants seeking to form a partnership, as it ensures compliance with state laws. A well-drafted South Carolina Partnership Agreement Between Accountants can help partners adhere to these regulations.

A partnership agreement in accounting is a formal contract between two or more accountants who agree to work together in a business venture. This document outlines the roles, responsibilities, and financial arrangements of each partner. By establishing clear terms, it helps reduce potential conflicts and ensures smooth operation of the partnership. Utilizing a South Carolina Partnership Agreement Between Accountants can provide a solid foundation for your collaborative efforts.

South Carolina does not officially recognize domestic partnerships in the same manner that some other states do. However, domestic partnership laws can vary significantly, so it is important to consult local regulations. Accountants entering into partnerships may benefit from creating a formal South Carolina Partnership Agreement Between Accountants to clearly define the rights and responsibilities within their arrangement. This can provide essential protection and clarity.

To fill out a partnership agreement, begin by including the names of the partners, details about the business operations, and the distribution of profits and losses among partners. Additionally, it is essential to outline the decision-making process and procedures for dispute resolution. By clearly defining these elements, partnerships can avoid future conflicts. A well-documented South Carolina Partnership Agreement Between Accountants can serve as a vital tool in ensuring smooth operations.

Filling out a partnership form requires detailed information about the partnership, including its name, address, and the business activities it undertakes. Each partner’s share of income, losses, and other contributions must also be clearly documented. It's advisable to gather all necessary financial records prior to filling out the form. Furthermore, templates and guidance from uslegalforms can simplify this process for those drafting a South Carolina Partnership Agreement Between Accountants.

Yes, South Carolina recognizes the federal extension for partnerships, which means if a partnership has filed for an extension federally, it is generally accepted at the state level. This is convenient for partnerships operating in multiple jurisdictions, including accountants who navigate both federal and state requirements. It streamlines the filing process and helps maintain compliance. Be sure to check for any state-specific requirements when operating under a South Carolina Partnership Agreement Between Accountants.