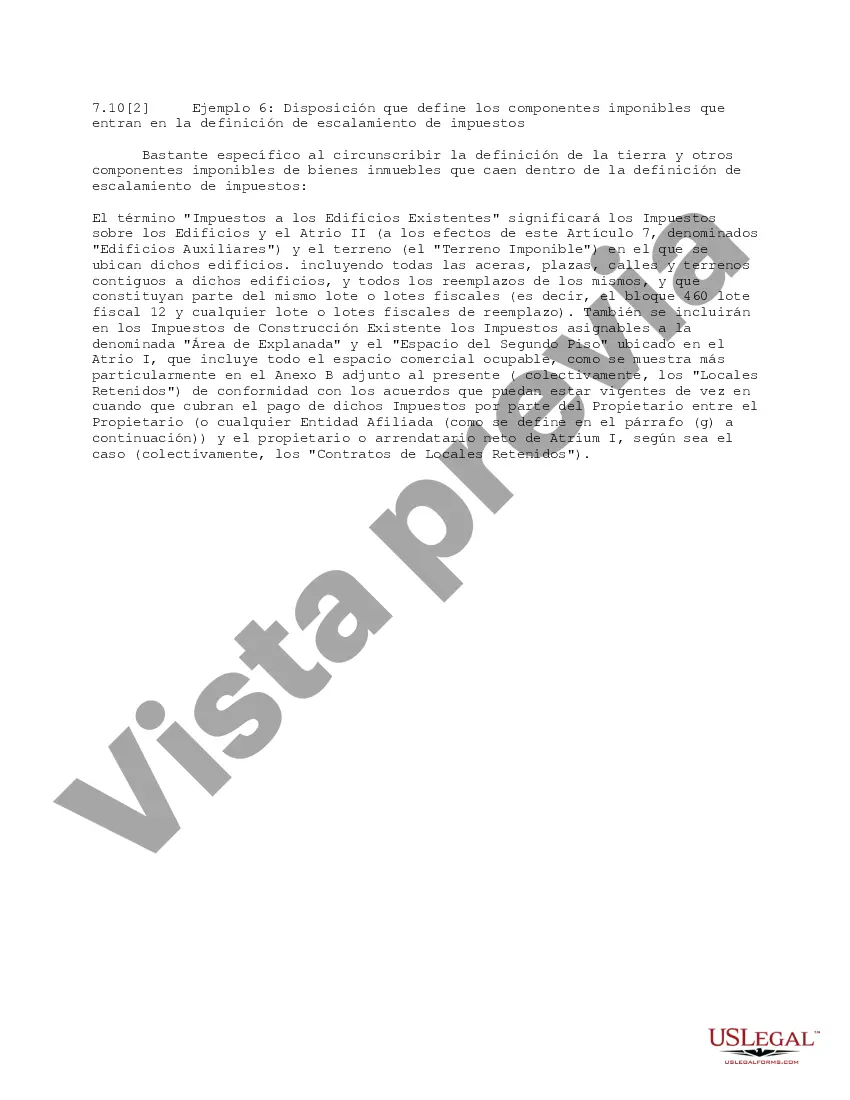

Tennessee Provision Defining the Taxable Components Falling into the Escalation Definition of Taxes In the state of Tennessee, the provision for defining the taxable components falling into the escalation definition of taxes plays a crucial role in determining the tax liabilities for individuals and businesses. This provision, implemented by the Tennessee Department of Revenue, outlines the specific components that are subject to taxation, ensuring an efficient and fair tax system. The taxable components falling into the escalation definition of taxes in Tennessee encompass various aspects of income, sales, excise, and property taxes. Let's explore the key components defined by this provision: 1. Income Taxes: Under the Tennessee provision, income taxes are levied on various sources of income, including wages, salaries, tips, interest, dividends, and rental income. Capital gains, royalties, and business profits also fall within the purview of taxable components. The provision establishes guidelines and rates for the calculation of income tax liabilities. 2. Sales Taxes: Tennessee imposes sales taxes on a broad range of goods and services sold within the state. The provision defines which products and services should be subject to taxation, such as consumer goods, electronics, clothing, food, and utilities. Additionally, it may specify exemptions or reduced tax rates for certain items like groceries, prescription drugs, or essential services. 3. Excise Taxes: Excise taxes are imposed on specific goods or activities deemed to carry a social cost or require special regulation. The Tennessee provision identifies the taxable components for excise taxes, such as gasoline, tobacco products, alcohol, gambling, and certain activities like amusement parks or the rental of certain equipment or properties. 4. Property Taxes: Under the Tennessee provision, property taxes are levied on real estate holdings, including land, buildings, and structures. These taxes contribute to funding local government services and infrastructure developments. It outlines the assessment methods, valuation procedures, and tax rates applicable to different types of properties. 5. Other relevant components: The provision may also address other taxable components, such as business taxes, inheritance or estate taxes, or vehicle taxes. Each component's definition, assessment methods, and tax rates may vary according to the specific type of tax. It's important to note that the Tennessee provision defining taxable components may be further categorized based on different types of taxes levied. These could include the Tennessee Personal Income Tax Provision, Tennessee Sales Tax Provision, Tennessee Excise Tax Provision, and Tennessee Property Tax Provision, among others. Each provision focuses on the specific tax type, defining the taxable components falling within its scope. By clearly defining taxable components falling into the escalation definition of taxes, the Tennessee provision enables individuals, businesses, and tax authorities to better understand their rights and obligations, ensuring a transparent and consistent tax system for all. It is advisable to consult professional tax advisors or refer directly to the Tennessee Department of Revenue for complete and up-to-date information on specific taxable components and related provisions.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Tennessee Disposición que define los componentes imponibles que caen en la definición de escalamiento de los impuestos - Provision Defining the Taxable Components Falling into the Escalation Definition of Taxes

Description

How to fill out Tennessee Disposición Que Define Los Componentes Imponibles Que Caen En La Definición De Escalamiento De Los Impuestos?

If you need to full, obtain, or printing legitimate record templates, use US Legal Forms, the greatest collection of legitimate forms, which can be found online. Take advantage of the site`s basic and hassle-free look for to find the documents you will need. A variety of templates for enterprise and personal purposes are sorted by categories and claims, or key phrases. Use US Legal Forms to find the Tennessee Provision Defining the Taxable Components Falling into the Escalation Definition of Taxes within a handful of clicks.

When you are presently a US Legal Forms consumer, log in for your bank account and click the Acquire button to obtain the Tennessee Provision Defining the Taxable Components Falling into the Escalation Definition of Taxes. You can also gain access to forms you formerly acquired in the My Forms tab of your respective bank account.

If you use US Legal Forms the first time, follow the instructions listed below:

- Step 1. Make sure you have selected the shape to the correct town/land.

- Step 2. Utilize the Review solution to examine the form`s information. Never forget to learn the explanation.

- Step 3. When you are not satisfied using the type, take advantage of the Look for field on top of the display to discover other versions of your legitimate type web template.

- Step 4. After you have located the shape you will need, go through the Buy now button. Select the rates strategy you like and include your accreditations to sign up to have an bank account.

- Step 5. Process the financial transaction. You may use your bank card or PayPal bank account to finish the financial transaction.

- Step 6. Select the format of your legitimate type and obtain it on your product.

- Step 7. Complete, edit and printing or indication the Tennessee Provision Defining the Taxable Components Falling into the Escalation Definition of Taxes.

Every single legitimate record web template you buy is your own for a long time. You have acces to every single type you acquired in your acccount. Click on the My Forms portion and choose a type to printing or obtain yet again.

Remain competitive and obtain, and printing the Tennessee Provision Defining the Taxable Components Falling into the Escalation Definition of Taxes with US Legal Forms. There are many skilled and state-distinct forms you can utilize for the enterprise or personal requires.