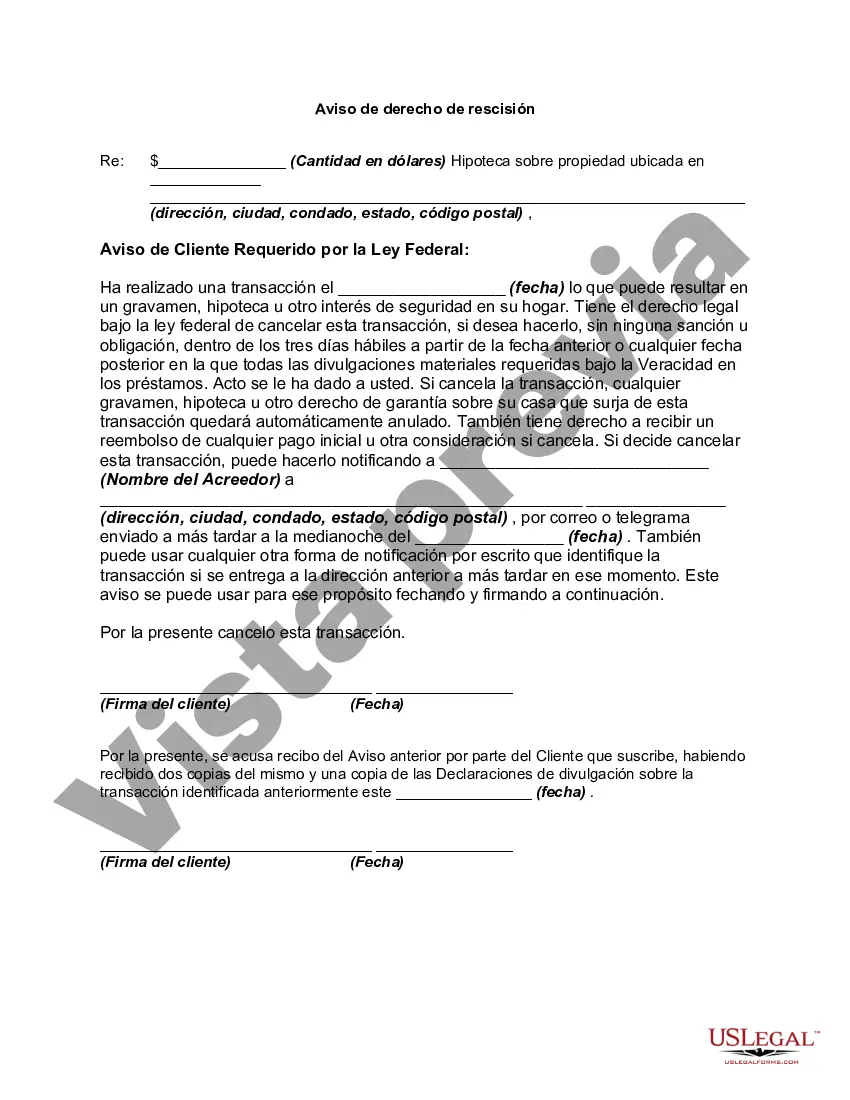

In a credit transaction in which a security interest is or will be retained or acquired in a consumer's principal dwelling, each consumer whose ownership is or will be subject to the security interest has the right to rescind the transaction. Lenders are required to deliver two copies of the notice of the right to rescind and one copy of the disclosure statement to each consumer entitled to rescind. The notice must be on a separate document that identifies the rescission period on the transaction and must clearly and conspicuously:

" disclose the retention or acquisition of a security interest in the consumer's principal dwelling;

" the consumer's right to rescind the transaction; and

" how the consumer may exercise the right to rescind with a form for that purpose.

The Texas Right to Rescind when a security interest in a consumer's principal dwelling is involved — Rescission is a legal provision that grants homeowners the ability to cancel certain transactions involving their homes within a specified period. This protection is enforceable under the Truth-in-Lending Act (TILL) and Regulation Z, which aims to offer consumers a way to reconsider and potentially avoid unfavorable agreements that could burden their financial well-being. When invoking the Texas Right to Rescind, there are several key factors and types of rescission to be aware of. One important aspect of the Texas Right to Rescind is the timeframe within which consumers can exercise this right. According to TILL, homeowners have until midnight of the third business day after completing the transaction to deliver written notice of their decision to rescind. This notice must be sent to the creditor or lender involved in the transaction, clearly expressing the homeowners' intent to cancel the agreement. When a security interest in a consumer's principal dwelling is involved, there are specific circumstances where the Texas Right to Rescind can be applied. Most commonly, this right is triggered when homeowners secure a mortgage or other loan using their primary residence as collateral. By doing so, they grant the lender a security interest in their dwelling, making it subject to the right of rescission. However, it is crucial to note that not all transactions involving a security interest in a consumer's principal dwelling qualify for rescission. Certain exemptions apply, such as loans used to purchase the property or loans arranged by government agencies. In addition to the standard application of the Texas Right to Rescind, there are two distinct types of rescission that may be relevant in this context: unilateral rescission and bilateral rescission. Unilateral rescission refers to situations where consumers exercise their right to rescind independently, without the need for any agreement or cooperation from the lender or creditor involved. On the other hand, bilateral rescission occurs when both parties mutually agree to cancel the transaction, typically as a result of renegotiating the terms or identifying discrepancies that require resolution. In summary, the Texas Right to Rescind when a security interest in a consumer's principal dwelling is involved — Rescission provides homeowners with a safeguard against unfavorable transactions that could potentially jeopardize their home and financial stability. By understanding the timing restrictions, circumstances triggering this right, and the potential application of unilateral and bilateral rescission, Texas homeowners can make informed decisions to protect their rights and financial interests.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.