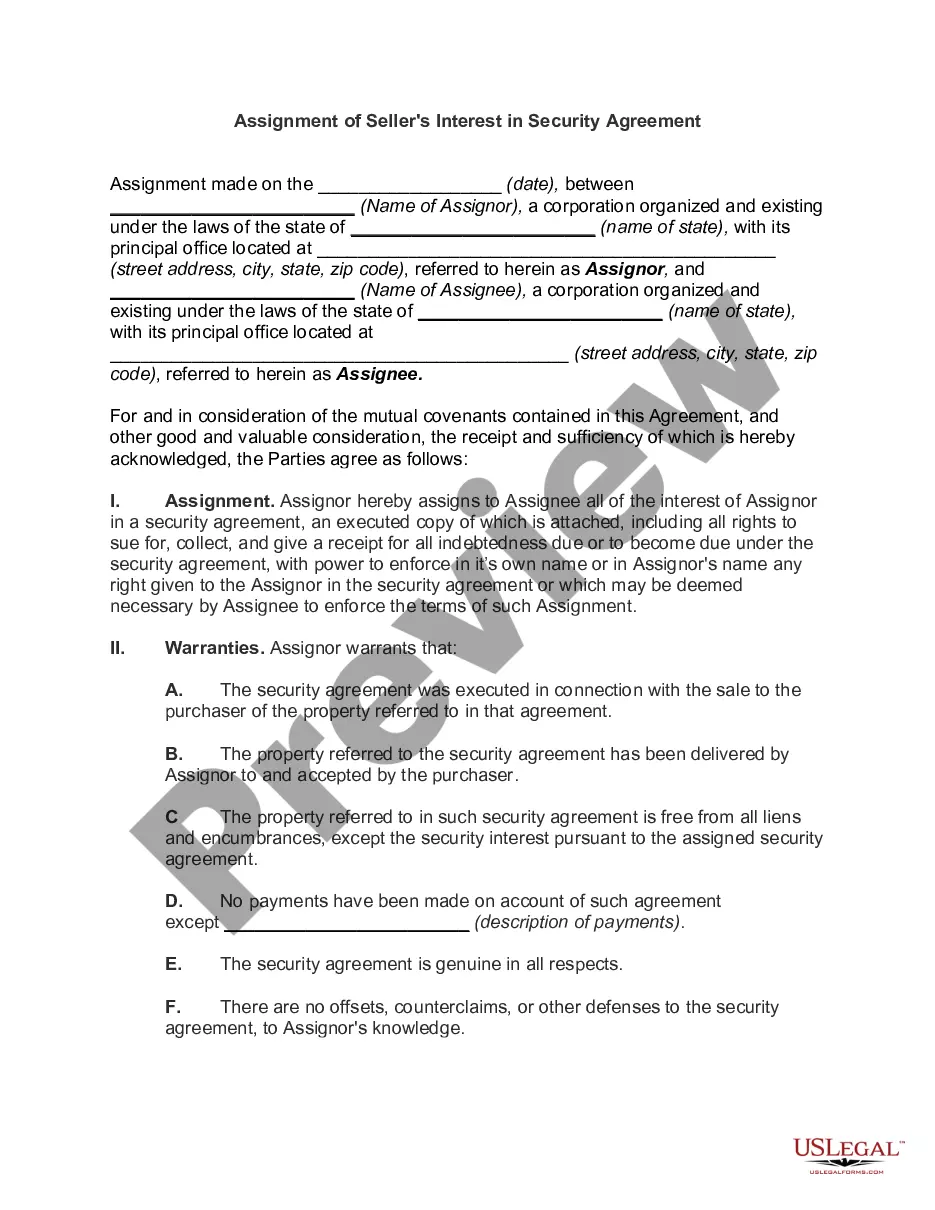

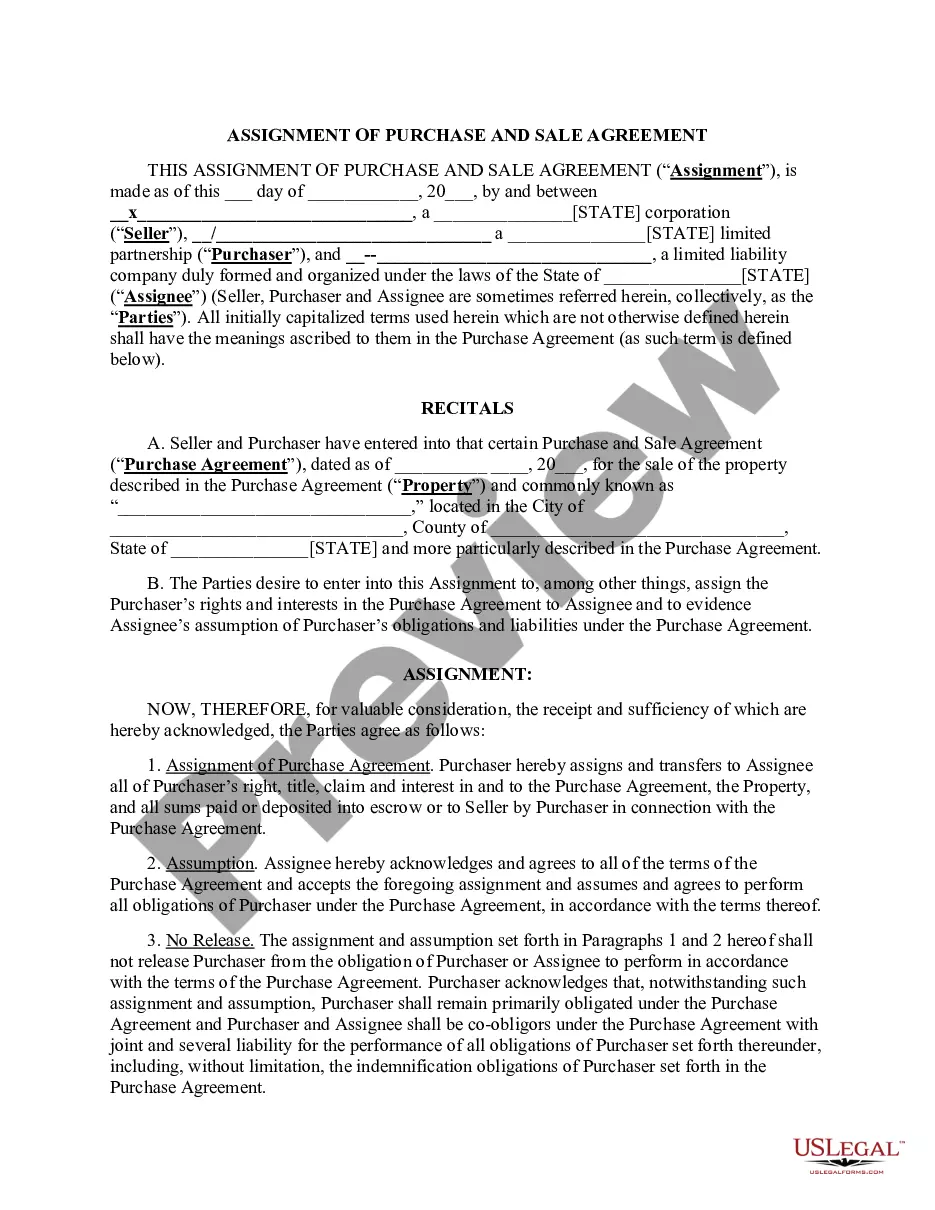

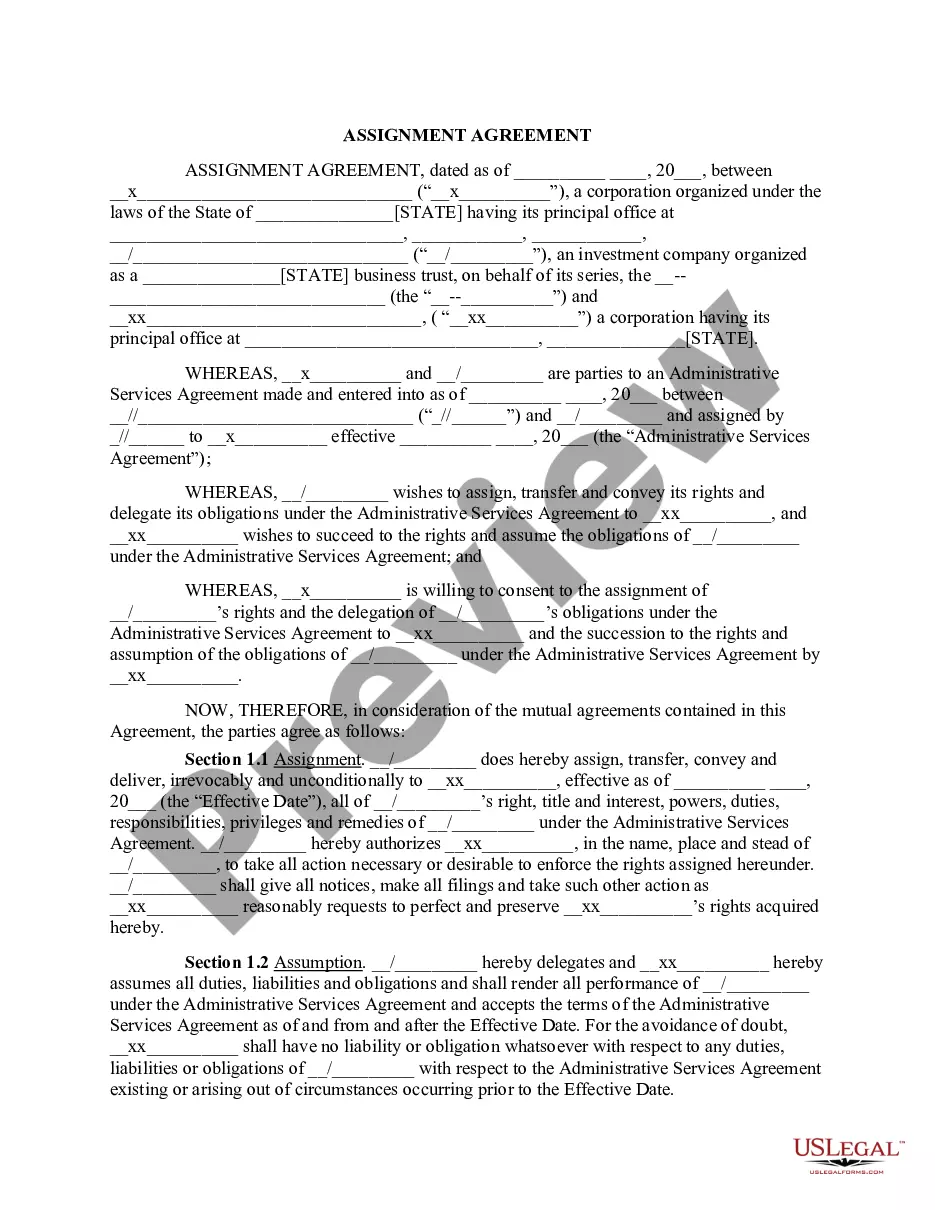

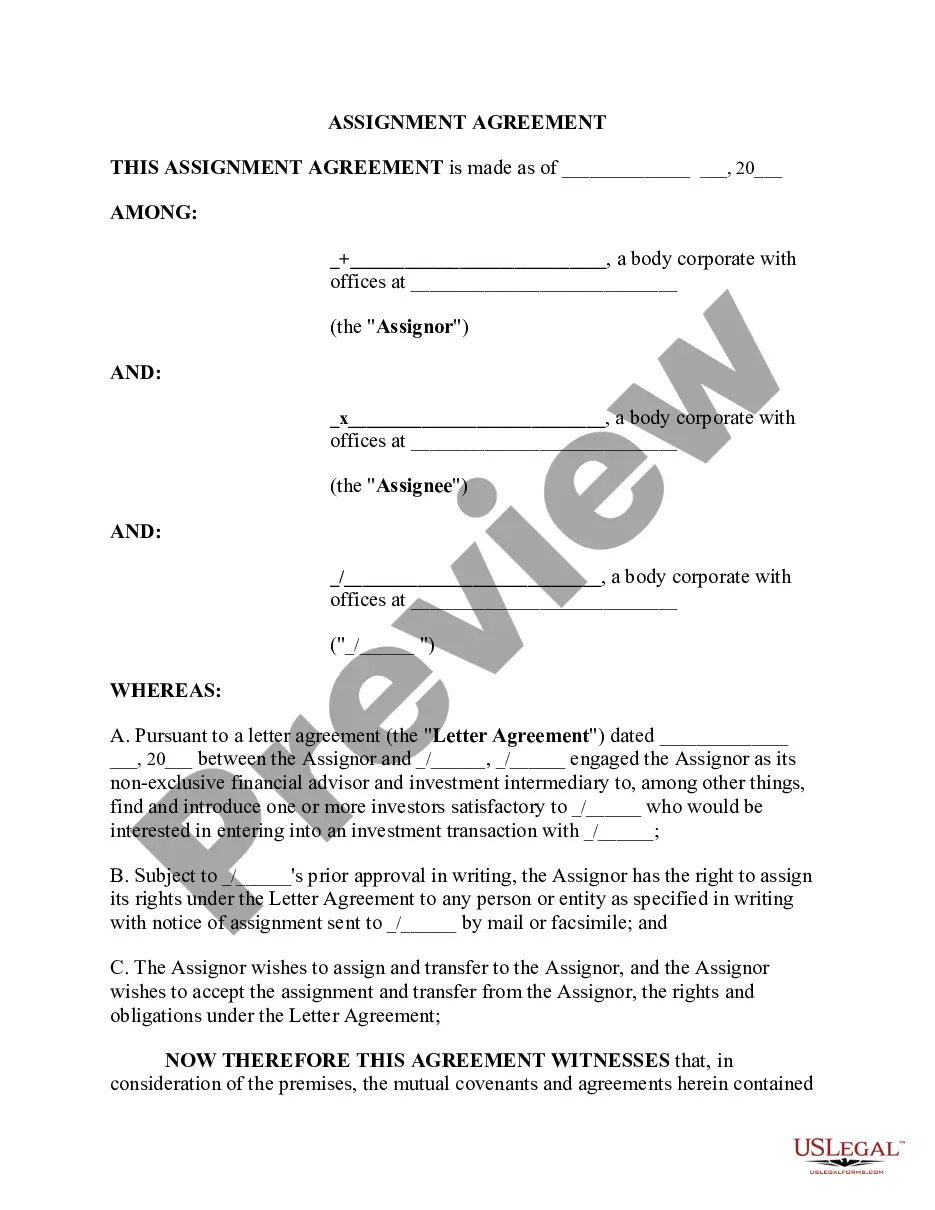

A certificate of deposit is a certificate or document issued by a bank acknowledging the receipt of money with a promise to pay to the depositor the amount of the deposit plus interest. This form is a collateral assignment of a certificate of deposit to secure a debt or some other obligation.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.