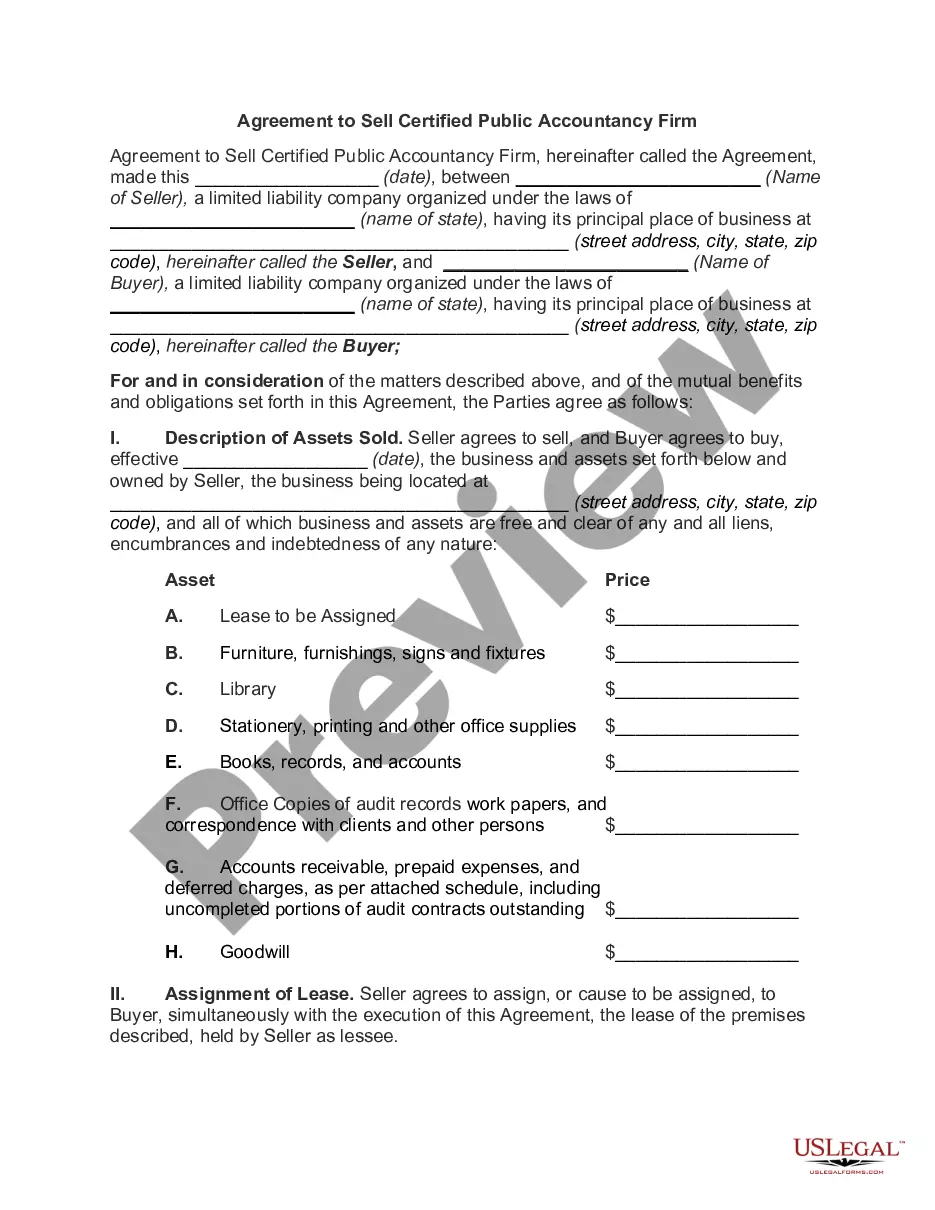

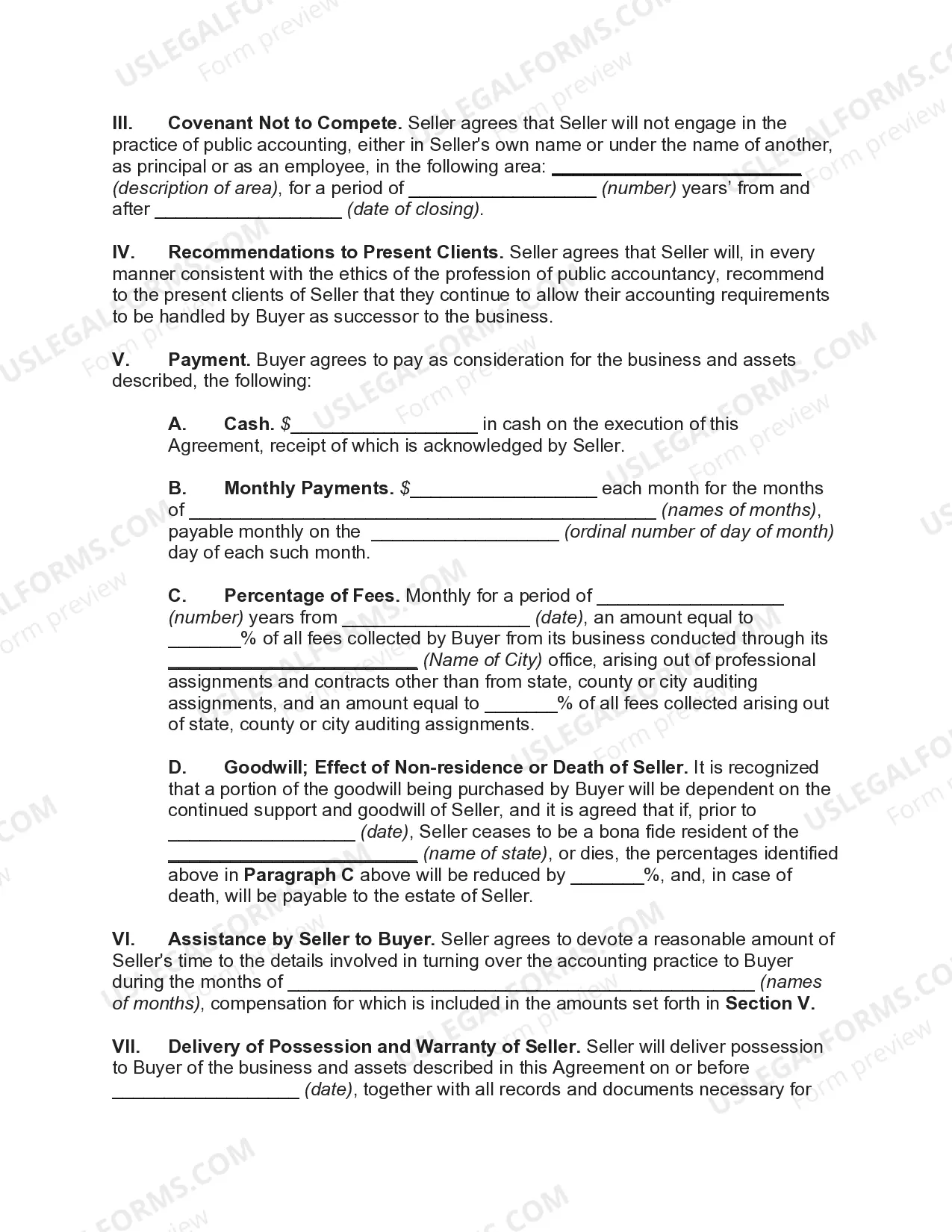

An Agreement to Sell Certified Public Accountancy Firm is an agreement between the seller of a Certified Public Accountancy (CPA) firm and the buyer. This agreement covers the terms and conditions of the sale, including the purchase price, payment method, transfer of assets, liabilities, and obligations. It also sets out the responsibilities of both parties during the sale process and beyond. The Agreement to Sell Certified Public Accountancy Firm is typically set up in two parts: the first part covers the purchase of the assets of the CPA firm, such as client lists, office space, equipment, and other tangible assets; the second part covers the sale of the firm's stock. Depending on the specific agreement, there may be other provisions included in the agreement, such as indemnity clauses, restrictive covenants, and warranties. There are three main types of Agreement to Sell Certified Public Accountancy Firm: an Asset Purchase Agreement, a Stock Purchase Agreement, and a Merger Agreement. An Asset Purchase Agreement is a contract between the seller and buyer in which the buyer agrees to purchase only the assets of the CPA firm; a Stock Purchase Agreement is an agreement between the seller and buyer in which the buyer agrees to purchase only the shares of the CPA firm; and a Merger Agreement is an agreement between the seller and buyer in which the seller and buyer agree to merge the CPA firm with another entity.

Agreement to Sell Certified Public Accountancy Firm

Description

How to fill out Agreement To Sell Certified Public Accountancy Firm?

Coping with legal paperwork requires attention, precision, and using properly-drafted templates. US Legal Forms has been helping people across the country do just that for 25 years, so when you pick your Agreement to Sell Certified Public Accountancy Firm template from our library, you can be certain it complies with federal and state laws.

Working with our service is easy and fast. To obtain the necessary paperwork, all you’ll need is an account with a valid subscription. Here’s a brief guide for you to find your Agreement to Sell Certified Public Accountancy Firm within minutes:

- Make sure to attentively examine the form content and its correspondence with general and law requirements by previewing it or reading its description.

- Search for an alternative formal blank if the previously opened one doesn’t suit your situation or state regulations (the tab for that is on the top page corner).

- Log in to your account and download the Agreement to Sell Certified Public Accountancy Firm in the format you prefer. If it’s your first time with our service, click Buy now to continue.

- Register for an account, decide on your subscription plan, and pay with your credit card or PayPal account.

- Decide in what format you want to obtain your form and click Download. Print the blank or add it to a professional PDF editor to submit it paper-free.

All documents are drafted for multi-usage, like the Agreement to Sell Certified Public Accountancy Firm you see on this page. If you need them in the future, you can fill them out without re-payment - just open the My Forms tab in your profile and complete your document whenever you need it. Try US Legal Forms and prepare your business and personal paperwork quickly and in full legal compliance!