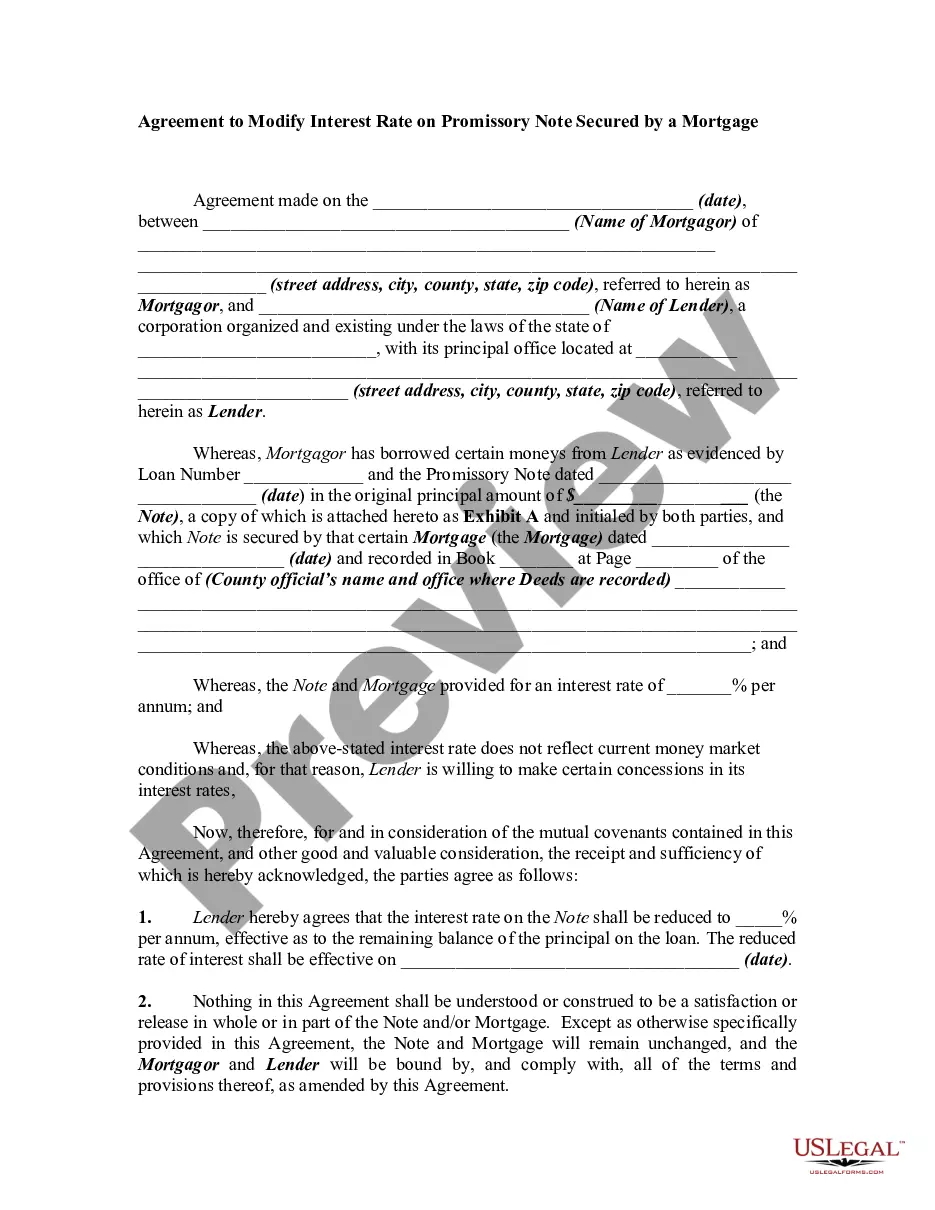

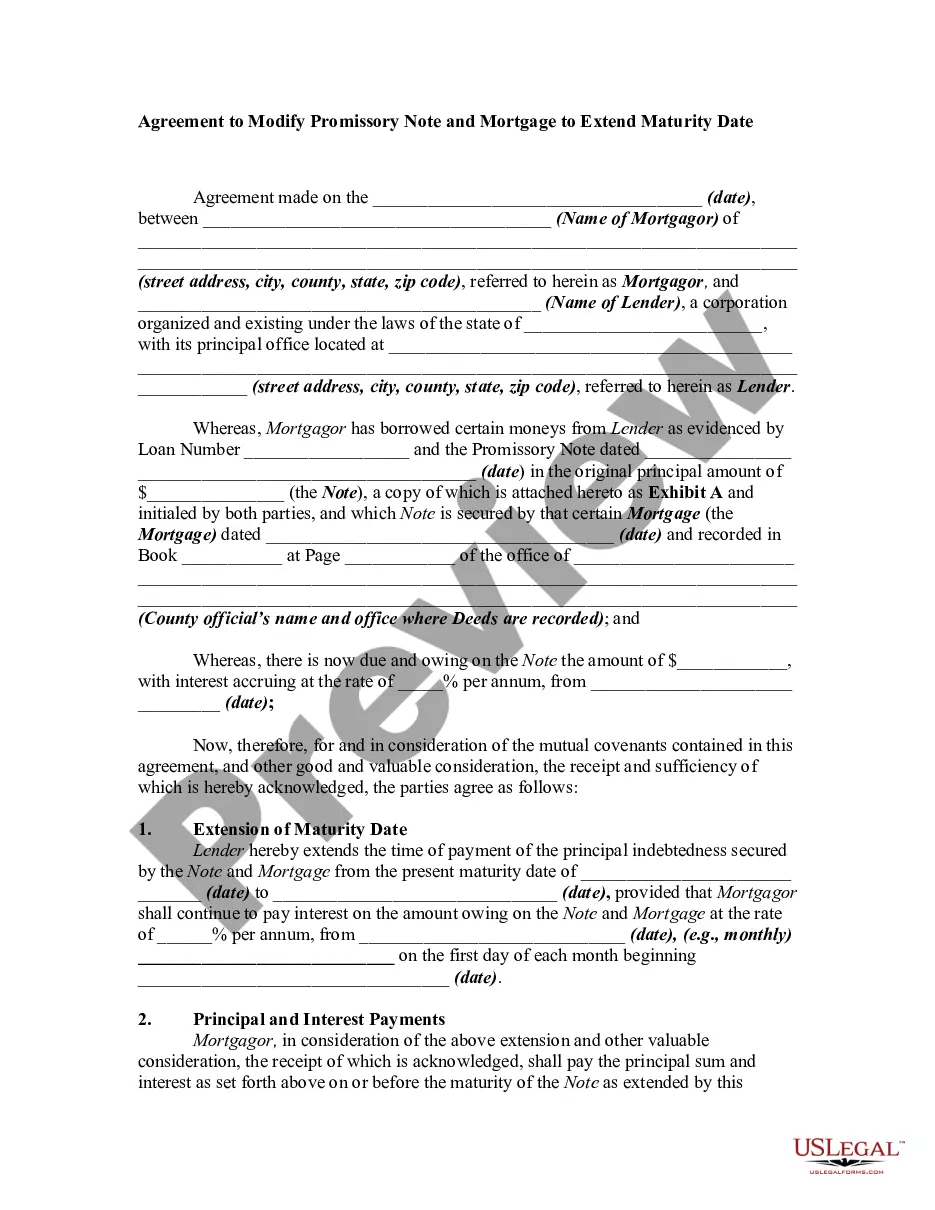

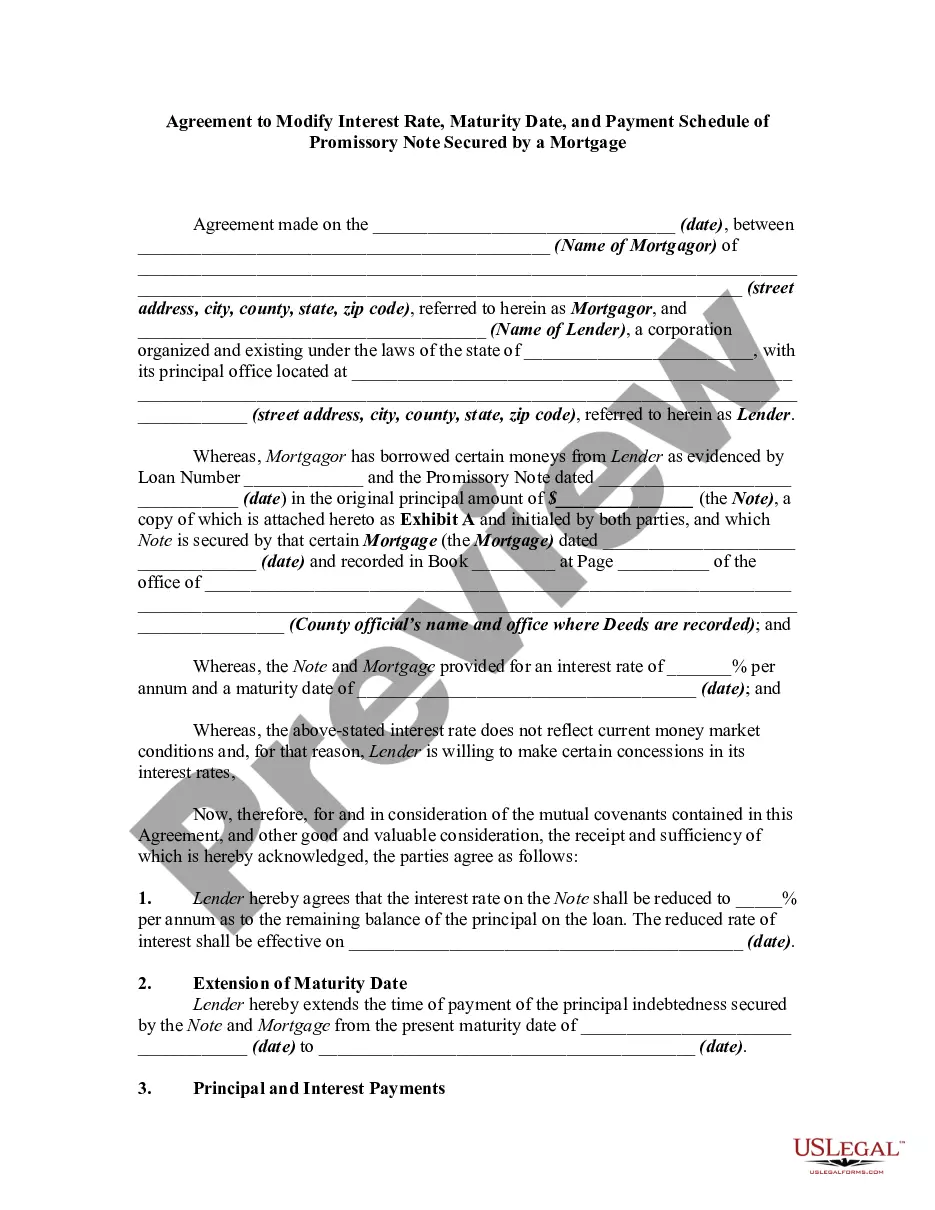

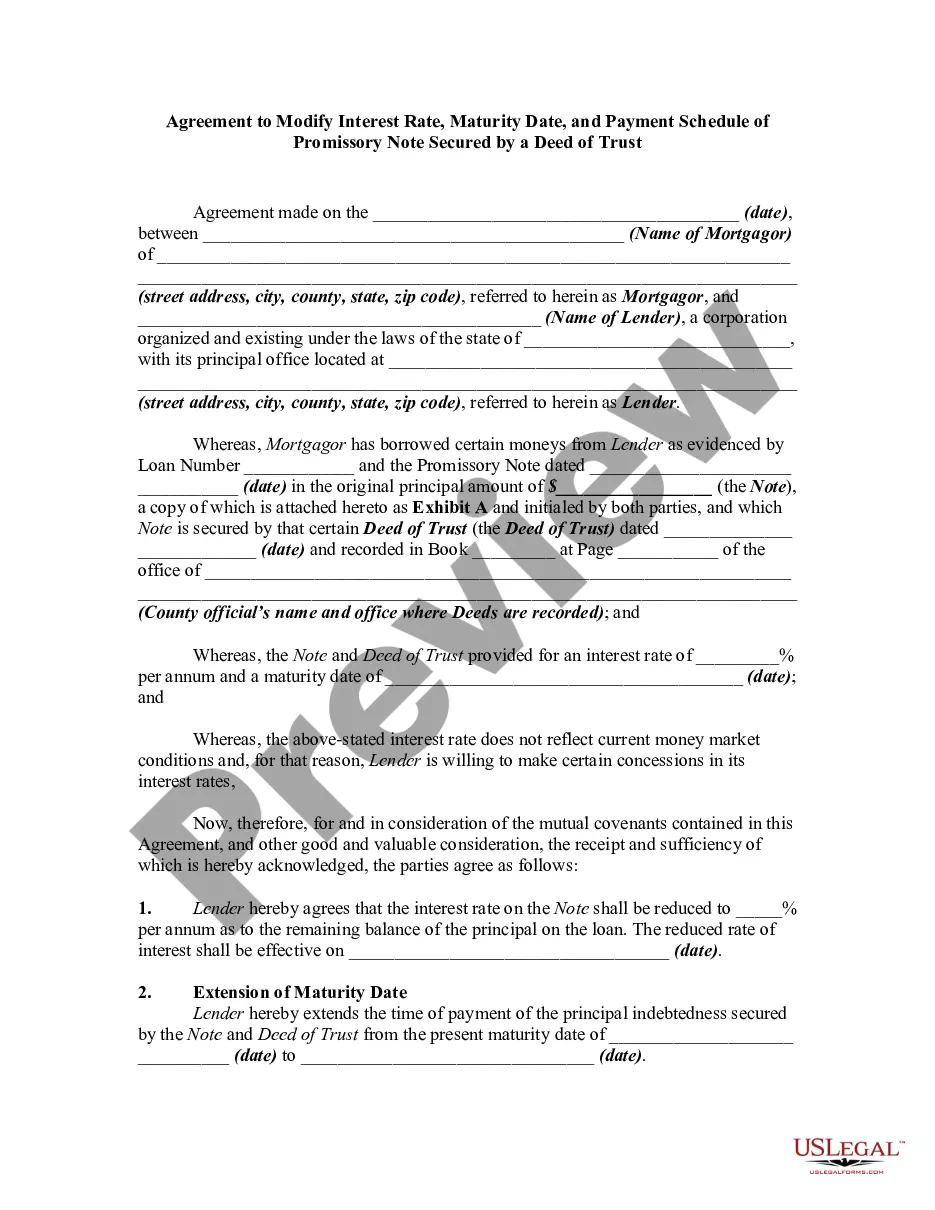

Agreement to Modify Promissory Note Secured by a Mortgage

What is this form?

The Agreement to Modify Promissory Note Secured by a Mortgage is a legal document that allows two parties involved in a loan agreement to modify the terms of the existing promissory note and mortgage. This agreement is essential when changes to interest rates or payment terms are necessary, reflecting current financial conditions. Unlike a typical mortgage modification, this form also specifically addresses the need to document the alterations formally and ensure they are recorded with the appropriate authorities.

Key components of this form

- Date of agreement and identification of parties involved.

- Reduction of the interest rate and its effective date.

- Extension of the maturity date for the loan repayment.

- Details on payment terms, including amounts and due dates.

- Clauses addressing the continuation of the original note and mortgage terms.

- Provision for notice requirements and governing law.

Common use cases

This form should be used when the lender agrees to modify the terms of an existing promissory note secured by a mortgage. Common scenarios include fluctuating interest rates impacting the affordability of payments or the need to extend the repayment period due to financial hardship. Using this agreement can ensure that all modifications are legally documented and enforceable.

Who this form is for

- Borrowers (Mortgagors) seeking to negotiate changes to their loan repayment terms.

- Lenders (financial institutions or corporations) who are willing to amend the original terms of the promissory note.

- Both parties involved in a mortgage transaction looking to adjust terms in light of changing market conditions.

Completing this form step by step

- Identify the parties by entering the names and addresses of both the Mortgagor and the Lender.

- Specify the date of the agreement.

- Enter the original terms of the promissory note, including the previous interest rate and maturity date.

- Input the new interest rate and the new maturity date as agreed upon by both parties.

- Detail the new payment terms, including the amount of installments and their due dates.

- Ensure both parties sign the agreement and have it notarized as required.

Does this document require notarization?

Notarization is required for this form to take effect. Our online notarization service, powered by Notarize, lets you verify and sign documents remotely through an encrypted video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to date the agreement properly.

- Not including all necessary signatures or forgetting to notarize the document.

- Incorrectly calculating the new payment amounts based on the adjusted interest rate.

- Neglecting to send the modified agreement for recording to the appropriate office.

- Assuming verbal agreements are sufficient; all modifications must be documented in writing.

Why complete this form online

- Convenience of downloading the form anytime and from anywhere.

- Editability allows users to customize terms easily before finalizing the agreement.

- Access to attorney-drafted templates ensures compliance with legal standards.

- Time-saving compared to traditional methods of acquiring legal forms.

Looking for another form?

Form popularity

FAQ

The mortgage modification agreement is a legal document between a lender and borrower to change an existing loan's terms. A typical modification may include reducing the interest rate, extending the repayment term, lowering monthly payments, or even forgiving part of the debt.

Amendments to a promissory note may only be made with consent from the lender and will be considered binding by all parties involved. Amendments can be made for significant changes and should be done in a formal manner to minimize liability and confusion with the contract moving forward.

Secured promissory notes The property that secures a note is called collateral, which can be either real estate or personal property. A promissory note secured by collateral will need a second document. If the collateral is real property, there will be either a mortgage or a deed of trust.

True, The borrower signs a promissory note pledging to repay the debt and gives the lender a mortgage, which is security for the property. When a property is mortgaged, the owner must execute both a promissory note and a security instrument.

A home mortgage secures a promissory note with the title to the property as collateral. This is done in case the lender ever needs to foreclose and sell the property because the homeowner did not make loan payments. Your lender will keep the original promissory note until your loan is paid off.

A promissory note is a document between the lender and the borrower in which the borrower promises to pay back the lender, it is a separate contract from the mortgage. The mortgage is a legal document that ties or "secures" a piece of real estate to an obligation to repay money.

A home mortgage secures a promissory note with the title to the property as collateral. This is done in case the lender ever needs to foreclose and sell the property because the homeowner did not make loan payments. Your lender will keep the original promissory note until your loan is paid off.

Promissory notes can be secured using a financing statement, deed of trust, or a mortgage. If a promissory note includes these terms, then it is a secured promissory note. So, the inclusion of collateral is the only real difference between secured promissory notes and unsecured promissory notes.