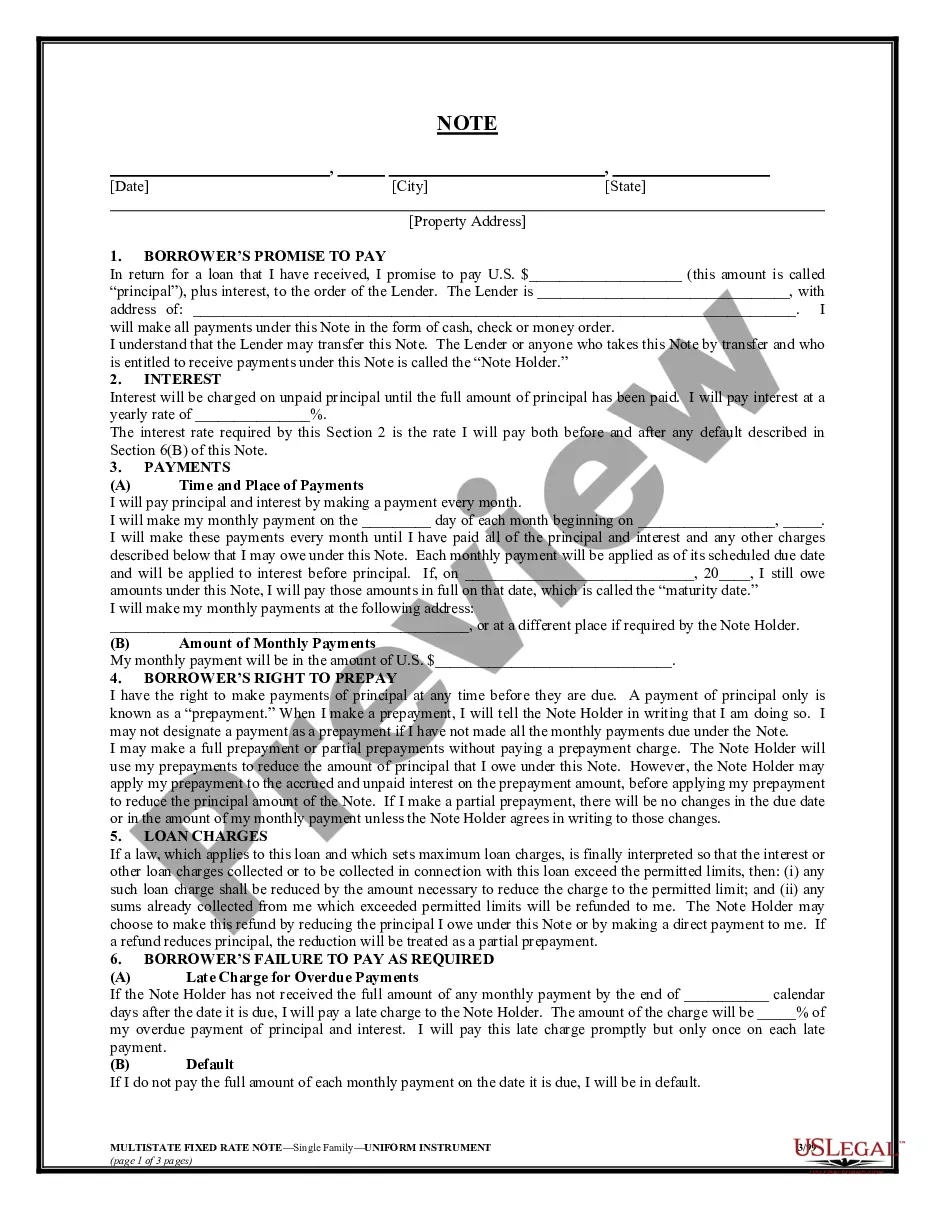

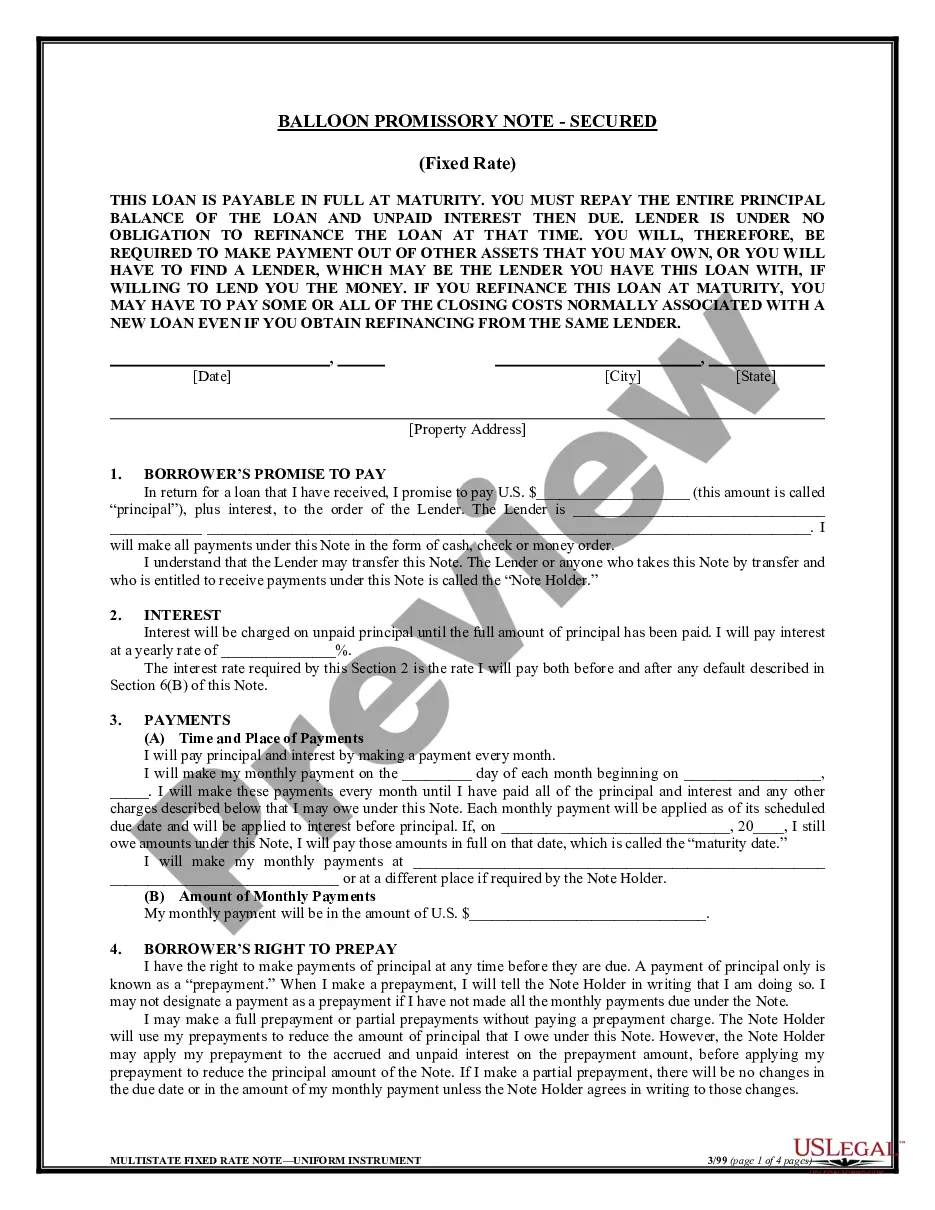

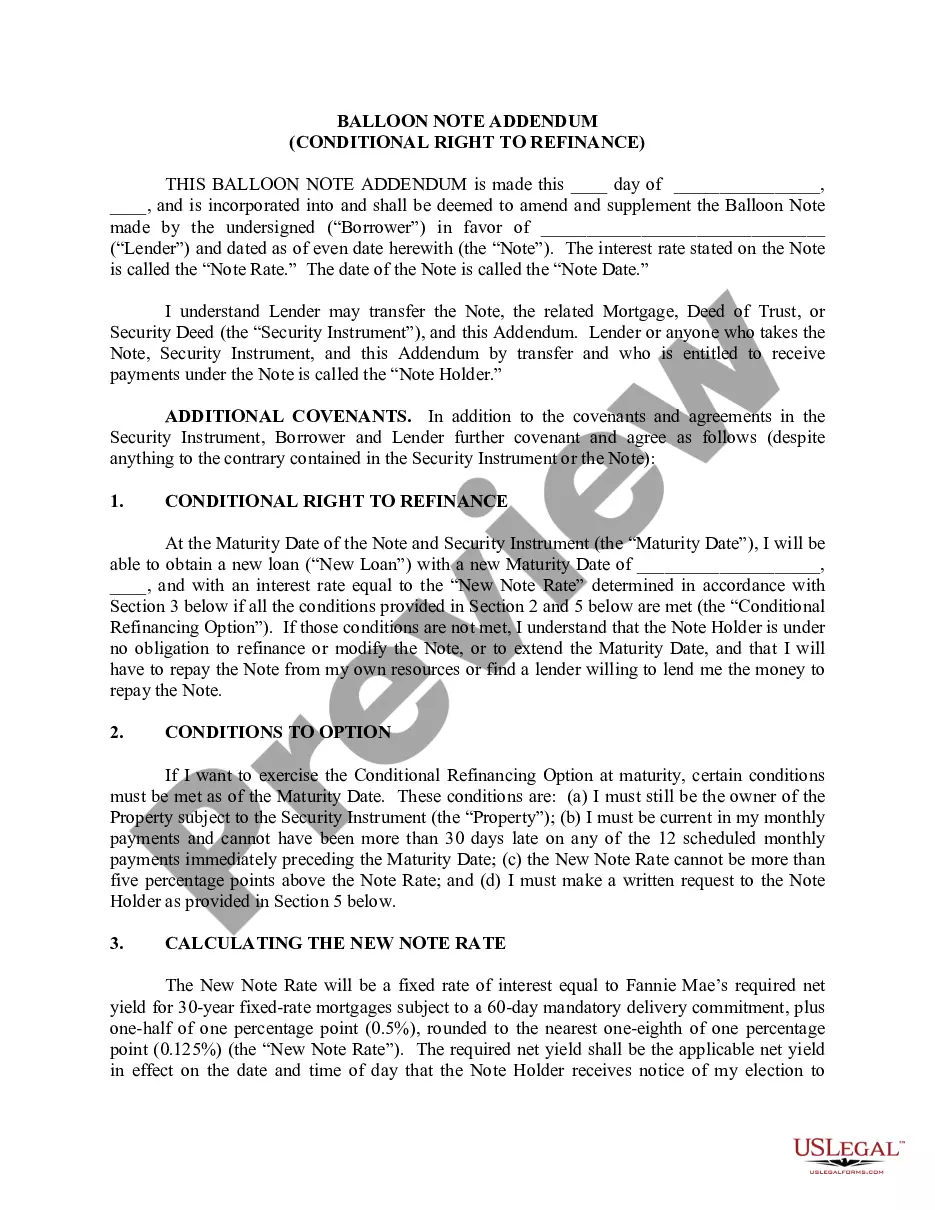

Multistate Balloon Fixed Rate Note - Single Family

About this form

The Multistate Balloon Fixed Rate Note for Single Family is a legal document used in real estate transactions. This note outlines the terms of a loan secured by a property, where the borrower agrees to make fixed-rate payments for a specific period before paying off the remaining balance in a lump sum at maturity. This form is commonly used for residential mortgages and differs from standard fixed-rate loans due to its unique balloon payment feature at the end of the term.

Key components of this form

- Fixed interest rate: Specifies the rate at which interest accrues on the principal amount.

- Prepayment provisions: Outlines terms for early payment of principal, including implications for accrued interest.

- Loan charges: Details conditions under which any loan charges must comply with applicable law.

- Default and late payment terms: Explains consequences of failing to make payments, including late fees and potential acceleration of the loan.

- Notification requirements: Instructions on how notices are to be delivered between the borrower and lender.

- Guarantees and waivers: Discusses obligations if multiple parties sign and rights they waive including presentment and notice of dishonor.

Common use cases

This form is essential when you are borrowing money to purchase a home or refinance an existing mortgage. It is applicable when the borrower wishes to secure a loan with a fixed interest rate that will culminate in a balloon payment at the end of the loan term. Use this form when you understand the implications of the balloon payment and are prepared for the associated financial commitments.

Intended users of this form

- Individuals seeking to purchase a single-family home with a balloon mortgage.

- Homeowners looking to refinance their existing mortgage with a fixed rate and balloon payment structure.

- Lenders who need a standardized document for issuing balloon fixed-rate loans.

Completing this form step by step

- Identify the parties involved: Include full names and addresses of the borrower and lender.

- Complete the loan details: Specify the loan amount, interest rate, and loan term.

- Enter payment schedule: Detail the frequency of payments and any prepayment terms that are agreed upon.

- Address default provisions: Clearly state the consequences of failing to make monthly payments on time.

- Sign and date the document: Ensure all parties sign and date the form to make it legally binding.

Notarization requirements for this form

In most cases, this form does not require notarization. However, some jurisdictions or signing circumstances might. US Legal Forms offers online notarization powered by Notarize, accessible 24/7 for a quick, remote process.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to specify the agreed-upon interest rate clearly.

- Not understanding the implications of the balloon payment due at the end of the term.

- Incomplete or incorrect party information, which can lead to legal issues later.

- Neglecting to address default terms adequately, leading to confusion if payments are missed.

Why complete this form online

- Convenience: Download and complete the form from anywhere, anytime.

- Editability: Easily fill out or revise the form as needed before finalizing.

- Reliability: Forms are drafted by licensed attorneys, ensuring they adhere to legal standards.

Key takeaways

- The Multistate Balloon Fixed Rate Note is essential for single-family home loans with a balloon payment option.

- Clear documentation of terms is crucial to avoid common pitfalls.

- Using this form online facilitates customization and expedience in real estate transactions.

Looking for another form?

Form popularity

FAQ

A balloon payment loan has lower monthly payments for a set period (generally three to 10 years) and one big "balloon" payment when the loan term ends. Because the balloon payment is significantly more than your regular monthly payment, these loans can be risky.

Since you'll be required to make a large payment at the end of the loan, balloon mortgages generally aren't a good idea for the average homebuyer. Your finances or life plans may not turn out how you predict. Balloon loans are also not widely available.

A balloon mortgage begins with fixed payments for a specific period and ends with a final lump-sum payment. The one-time payment is called a balloon payment because it's much larger than the beginning payments.

The biggest advantage of a balloon mortgage is it generally comes with lower interest rates, so you make smaller monthly mortgage payments. You also may qualify for a larger loan amount with a balloon mortgage than you would if you got an adjustable-rate or fixed-rate mortgage.

Balloon loans can be attractive to short-term borrowers because they typically carry lower interest rates than loans with longer terms. However, the borrower must be aware of refinancing risks as there's a possibility the loan may reset at a higher interest rate.

A balloon payment is a larger-than-usual one-time payment at the end of the loan term. If you have a mortgage with a balloon payment, your payments may be lower in the years before the balloon payment comes due, but you could owe a big amount at the end of the loan.

A balloon mortgage begins with fixed payments for a specific period and ends with a final lump-sum payment. The one-time payment is called a balloon payment because it's much larger than the beginning payments.

Who Files Form 3200? Form 3200 is the Multistate Fixed Rate Note. It must be completed by the borrower who confirms that the loan was received and that the interest and the principal amount will be paid to the lender ing to the agreement.