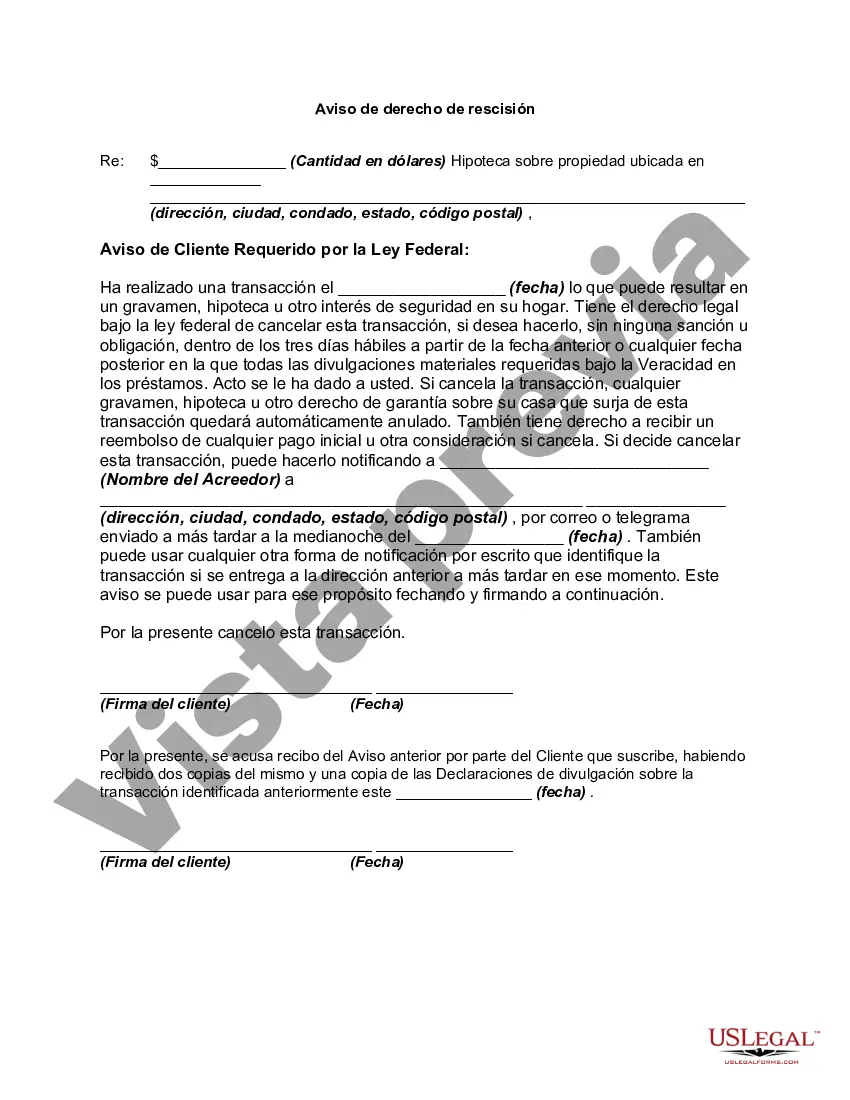

In a credit transaction in which a security interest is or will be retained or acquired in a consumer's principal dwelling, each consumer whose ownership is or will be subject to the security interest has the right to rescind the transaction. Lenders are required to deliver two copies of the notice of the right to rescind and one copy of the disclosure statement to each consumer entitled to rescind. The notice must be on a separate document that identifies the rescission period on the transaction and must clearly and conspicuously:

" disclose the retention or acquisition of a security interest in the consumer's principal dwelling;

" the consumer's right to rescind the transaction; and

" how the consumer may exercise the right to rescind with a form for that purpose.

Utah Right to Rescind When Security Interest in Consumer's Principal Dwelling is Involved — Rescission In Utah, consumers have specific rights when it comes to rescinding a contract that involves a security interest in their principal dwelling. Rescission refers to the action of canceling or undoing a contract, allowing the consumer to withdraw from the agreement without penalty. In the context of a security interest in the consumer's principal dwelling, this right becomes even more crucial, as it directly impacts homeownership and financial stability. When a consumer enters into a contract that includes a security interest in their principal dwelling (such as a mortgage or home equity loan), the Utah Right to Rescind is particularly relevant. This right offers consumers the opportunity to reconsider and potentially cancel the agreement within a specified time frame, provided certain conditions are met. One important aspect of the Utah Right to Rescind is the period within which a consumer must exercise this right. The federal Truth in Lending Act (TILL) typically provides consumers with three business days to rescind a contract involving their principal dwelling. However, there may be additional state-specific provisions that extend the rescission period in Utah. It is essential for consumers to be aware of these time limits and act accordingly to protect their rights. It is crucial to note that the Utah Right to Rescind applies specifically to contracts involving a security interest in the consumer's principal dwelling. This includes various types of loans like mortgages, home equity lines of credit (Helots), and refinancing agreements. However, it may not extend to other types of contracts, such as personal loans or credit card agreements. While the Utah Right to Rescind primarily refers to the act of canceling or ending a contract within a particular timeframe, there are no specific alternative types of rescission beyond the standard right to rescind. However, the conditions under which the right to rescind can be exercised may vary based on the nature of the contract or the terms specified by the lender. It is advisable for consumers to carefully review their contract terms and consult legal assistance if they have any doubts or concerns regarding their right to rescind. Keywords: Utah Right to Rescind, security interest, consumer's principal dwelling, Rescission, contract cancellation, financial stability, homeownership, mortgage, home equity loan, Truth in Lending Act, TILL, time limits, loans, home equity lines of credit, Helots, refinancing agreements, personal loans, credit card agreements.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.