Vermont Retirement Cash Flow refers to a financial plan or strategy aimed at ensuring a steady and stable income during retirement for residents of Vermont, a state in the northeastern United States. Retirement cash flow is crucial for maintaining a comfortable lifestyle and meeting expenses after leaving the workforce. This comprehensive approach to retirement planning involves analyzing various sources of income, such as social security benefits, pension plans, investments, savings, and any other retirement account contributions. The objective is to create a cash flow system that covers essential expenses, including housing, healthcare, food, transportation, and recreational activities, while also accounting for unexpected expenses and inflation. Different types of Vermont Retirement Cash Flow may include: 1. Social Security Benefits: This government-provided program ensures retirees receive a monthly income based on their earnings history. Understanding how to optimize these benefits within the context of Vermont's specific policies is essential. 2. Pension Plans: Some retirees may have access to employer-sponsored pension plans, which provide regular payments during retirement. These plans vary in structure and payout options, including single life annuities or joint and survivor annuities. 3. Individual Retirement Accounts (IRAs): Vermont retirees may have traditional or Roth IRAs, which allow for tax-advantaged saving. Strategies such as converting traditional IRAs to Roth IRAs or adopting a systematic withdrawal plan help create a consistent cash flow during retirement. 4. Annuities: Retirees can turn a portion of their savings into annuities, either immediate or deferred, providing a steady stream of income for a specific period or even for a lifetime. 5. Investment Portfolios: Building a diversified investment portfolio tailored to retirement goals is crucial. It may include a mix of stocks, bonds, mutual funds, ETFs, and real estate investment trusts (Rests). Regular portfolio reviews and rebalancing optimize returns and manage risk. 6. Health Savings Accounts (Has): Has been tax-advantaged accounts intended to cover medical expenses. They offer potential long-term benefits, especially when used alongside retirement healthcare planning. 7. Part-time Employment or Consulting: Many retirees choose to work part-time or become consultants during retirement. This provides additional income while allowing for flexibility and potentially prolonging retirement savings. By considering the various facets of retirement cash flow, Vermont residents can develop personalized plans to achieve financial stability and security during their retirement years. It is crucial to seek professional advice from financial planners or retirement specialists who are knowledgeable about Vermont-specific regulations and programs. They can assist with creating a tailored retirement cash flow strategy aligned with an individual's goals, risk tolerance, and the unique aspects of Vermont retirement planning.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Vermont Flujo de caja de jubilación - Retirement Cash Flow

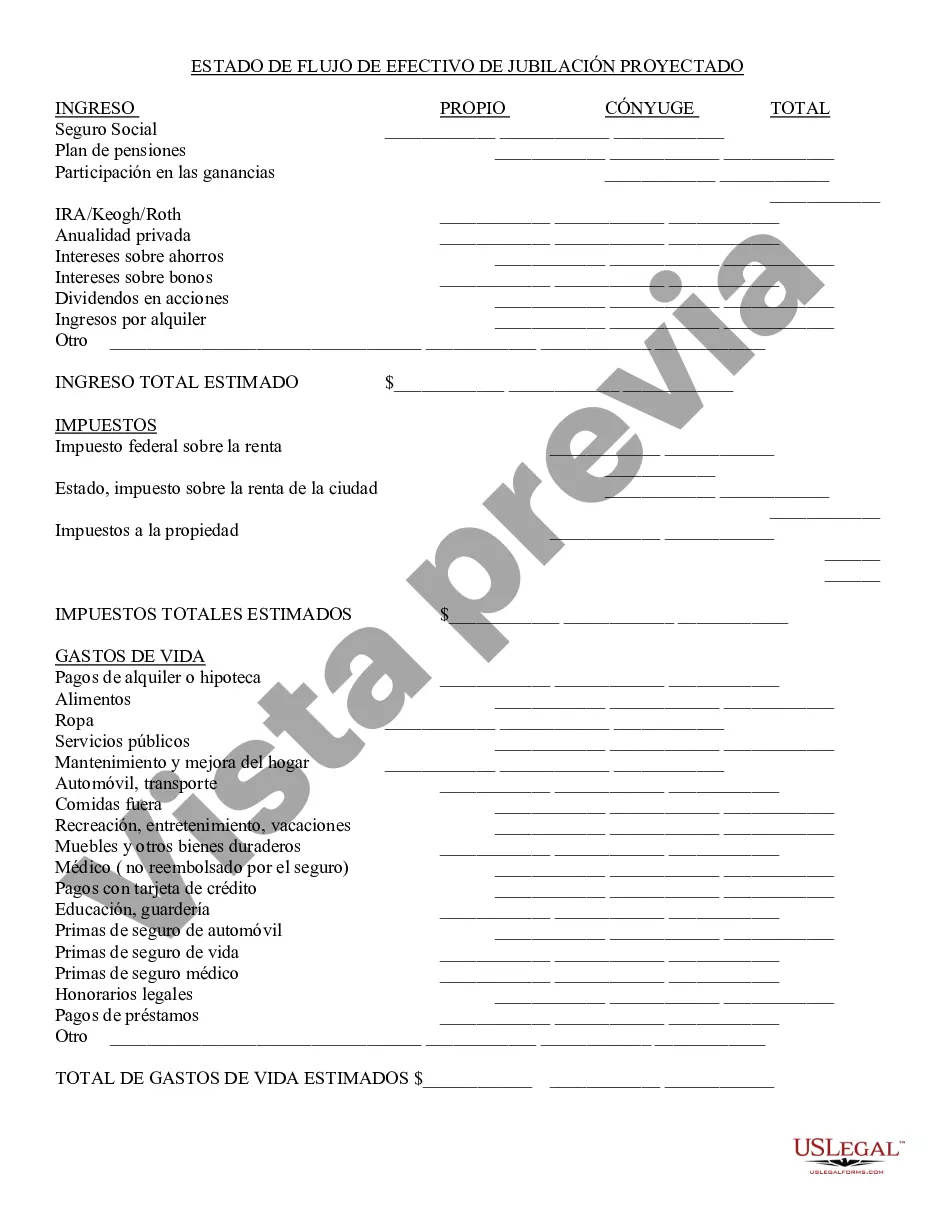

Description

How to fill out Vermont Flujo De Caja De Jubilación?

US Legal Forms - one of the largest libraries of legal forms in America - gives an array of legal record layouts it is possible to download or print out. Utilizing the web site, you may get 1000s of forms for enterprise and personal uses, categorized by categories, states, or search phrases.You will discover the most up-to-date versions of forms like the Vermont Retirement Cash Flow within minutes.

If you have a registration, log in and download Vermont Retirement Cash Flow from your US Legal Forms catalogue. The Down load button will appear on every single type you look at. You have access to all formerly saved forms within the My Forms tab of your bank account.

If you want to use US Legal Forms the very first time, listed below are simple directions to help you started:

- Be sure to have chosen the proper type for your personal city/county. Click the Review button to review the form`s information. Read the type information to actually have chosen the right type.

- When the type does not fit your specifications, make use of the Lookup field on top of the display to discover the one that does.

- In case you are pleased with the shape, verify your option by clicking on the Acquire now button. Then, opt for the costs strategy you like and provide your accreditations to sign up to have an bank account.

- Approach the financial transaction. Make use of Visa or Mastercard or PayPal bank account to finish the financial transaction.

- Select the file format and download the shape on the gadget.

- Make modifications. Load, change and print out and sign the saved Vermont Retirement Cash Flow.

Every single design you included in your bank account does not have an expiry particular date and is also the one you have eternally. So, if you would like download or print out another duplicate, just check out the My Forms portion and then click around the type you need.

Gain access to the Vermont Retirement Cash Flow with US Legal Forms, by far the most extensive catalogue of legal record layouts. Use 1000s of expert and express-particular layouts that fulfill your business or personal needs and specifications.