Partnership agreements are written documents that explicitly detail the relationship between the business partners and their individual obligations and contributions to the partnership. Since partnership agreements should cover all possible business situations that could arise during the partnership's life, the documents are often complex; legal counsel in drafting and reviewing the finished contract is generally recommended. If a partnership does not have a partnership agreement in place when it dissolves, the guidelines of the Uniform Partnership Act and various state laws will determine how the assets and debts of the partnership are distributed.

Vermont Partnership Agreement Between Accountants: Detailed Overview and Types Introduction: A Vermont Partnership Agreement Between Accountants is a legally binding document that outlines the terms and conditions applicable to a partnership between two or more accountants or accounting firms operating in the state of Vermont, USA. This agreement serves as a vital tool in establishing the rights, responsibilities, profit sharing, decision-making processes, and dispute resolution mechanisms among the partners. Key Components of a Vermont Partnership Agreement Between Accountants: 1. Partnership Structure: The agreement clearly defines the partnership's structure, including the names and roles of all partners involved. It outlines the type of partnership, such as general partnership or limited liability partnership (LLP), and specifies the nature of the partnership's business activities. 2. Capital Contributions: The agreement elaborates on the initial capital contributions made by each partner for the establishment and ongoing operations of the partnership. It also outlines the procedures to be followed for subsequent capital contributions or changes to the partnership's capital structure. 3. Profit Sharing and Loss Distribution: The partnership agreement determines the method for allocating profits and losses among partners, which can be based on capital contributions, ownership percentage, or a predetermined formula. This section also addresses the distribution of profits among partners. 4. Decision-Making Authority: The agreement outlines the decision-making process within the partnership, specifying whether partners have equal voting rights or if certain partners possess greater decision-making authority based on factors such as capital contributions or seniority. It also clarifies the process for resolving disputes related to decision-making. 5. Partner Responsibilities and Duties: This section comprehensively defines the responsibilities and duties of each partner, including areas of expertise, client management, business development, and maintaining professional standards. It may also include provisions for non-competition or non-solicitation to protect the partnership's interests. 6. Partnership Management: The agreement outlines the procedures and responsibilities for managing the day-to-day operations of the partnership, such as financial management, accounting practices, record-keeping, and regulatory compliance. It may identify one or more partners who will act as managing partners responsible for overseeing these operations. Types of Vermont Partnership Agreements Between Accountants: 1. General Partnership Agreement: This is the most common type, where all partners share equal responsibility, authority, and liability. 2. Limited Liability Partnership (LLP) Agreement: With an LLP agreement, partners have limited personal liability for the partnership's debts and obligations, protecting their personal assets from business-related risks. 3. Professional Corporation Partnership Agreement: In certain cases, accountants form a professional corporation and use a partnership agreement that aligns with corporate rules and regulations while safeguarding their professional status. 4. Partnership Agreement for Mergers and Acquisitions: This type of agreement is utilized when two or more accounting firms merge or one firm acquires another, ensuring a smooth transition by outlining the terms, conditions, and responsibilities of the new partnership. Conclusion: A Vermont Partnership Agreement Between Accountants is an essential legal document that establishes the rules, responsibilities, and rights of partners in an accounting partnership within the state. By clearly defining these aspects, it helps mitigate conflicts, ensures smooth operations, and provides a solid framework for successful collaboration. Whether it is a general partnership, limited liability partnership, professional corporation partnership, or an agreement for mergers and acquisitions, this agreement serves as a foundation for a thriving and legally compliant accounting partnership in Vermont.Vermont Partnership Agreement Between Accountants: Detailed Overview and Types Introduction: A Vermont Partnership Agreement Between Accountants is a legally binding document that outlines the terms and conditions applicable to a partnership between two or more accountants or accounting firms operating in the state of Vermont, USA. This agreement serves as a vital tool in establishing the rights, responsibilities, profit sharing, decision-making processes, and dispute resolution mechanisms among the partners. Key Components of a Vermont Partnership Agreement Between Accountants: 1. Partnership Structure: The agreement clearly defines the partnership's structure, including the names and roles of all partners involved. It outlines the type of partnership, such as general partnership or limited liability partnership (LLP), and specifies the nature of the partnership's business activities. 2. Capital Contributions: The agreement elaborates on the initial capital contributions made by each partner for the establishment and ongoing operations of the partnership. It also outlines the procedures to be followed for subsequent capital contributions or changes to the partnership's capital structure. 3. Profit Sharing and Loss Distribution: The partnership agreement determines the method for allocating profits and losses among partners, which can be based on capital contributions, ownership percentage, or a predetermined formula. This section also addresses the distribution of profits among partners. 4. Decision-Making Authority: The agreement outlines the decision-making process within the partnership, specifying whether partners have equal voting rights or if certain partners possess greater decision-making authority based on factors such as capital contributions or seniority. It also clarifies the process for resolving disputes related to decision-making. 5. Partner Responsibilities and Duties: This section comprehensively defines the responsibilities and duties of each partner, including areas of expertise, client management, business development, and maintaining professional standards. It may also include provisions for non-competition or non-solicitation to protect the partnership's interests. 6. Partnership Management: The agreement outlines the procedures and responsibilities for managing the day-to-day operations of the partnership, such as financial management, accounting practices, record-keeping, and regulatory compliance. It may identify one or more partners who will act as managing partners responsible for overseeing these operations. Types of Vermont Partnership Agreements Between Accountants: 1. General Partnership Agreement: This is the most common type, where all partners share equal responsibility, authority, and liability. 2. Limited Liability Partnership (LLP) Agreement: With an LLP agreement, partners have limited personal liability for the partnership's debts and obligations, protecting their personal assets from business-related risks. 3. Professional Corporation Partnership Agreement: In certain cases, accountants form a professional corporation and use a partnership agreement that aligns with corporate rules and regulations while safeguarding their professional status. 4. Partnership Agreement for Mergers and Acquisitions: This type of agreement is utilized when two or more accounting firms merge or one firm acquires another, ensuring a smooth transition by outlining the terms, conditions, and responsibilities of the new partnership. Conclusion: A Vermont Partnership Agreement Between Accountants is an essential legal document that establishes the rules, responsibilities, and rights of partners in an accounting partnership within the state. By clearly defining these aspects, it helps mitigate conflicts, ensures smooth operations, and provides a solid framework for successful collaboration. Whether it is a general partnership, limited liability partnership, professional corporation partnership, or an agreement for mergers and acquisitions, this agreement serves as a foundation for a thriving and legally compliant accounting partnership in Vermont.

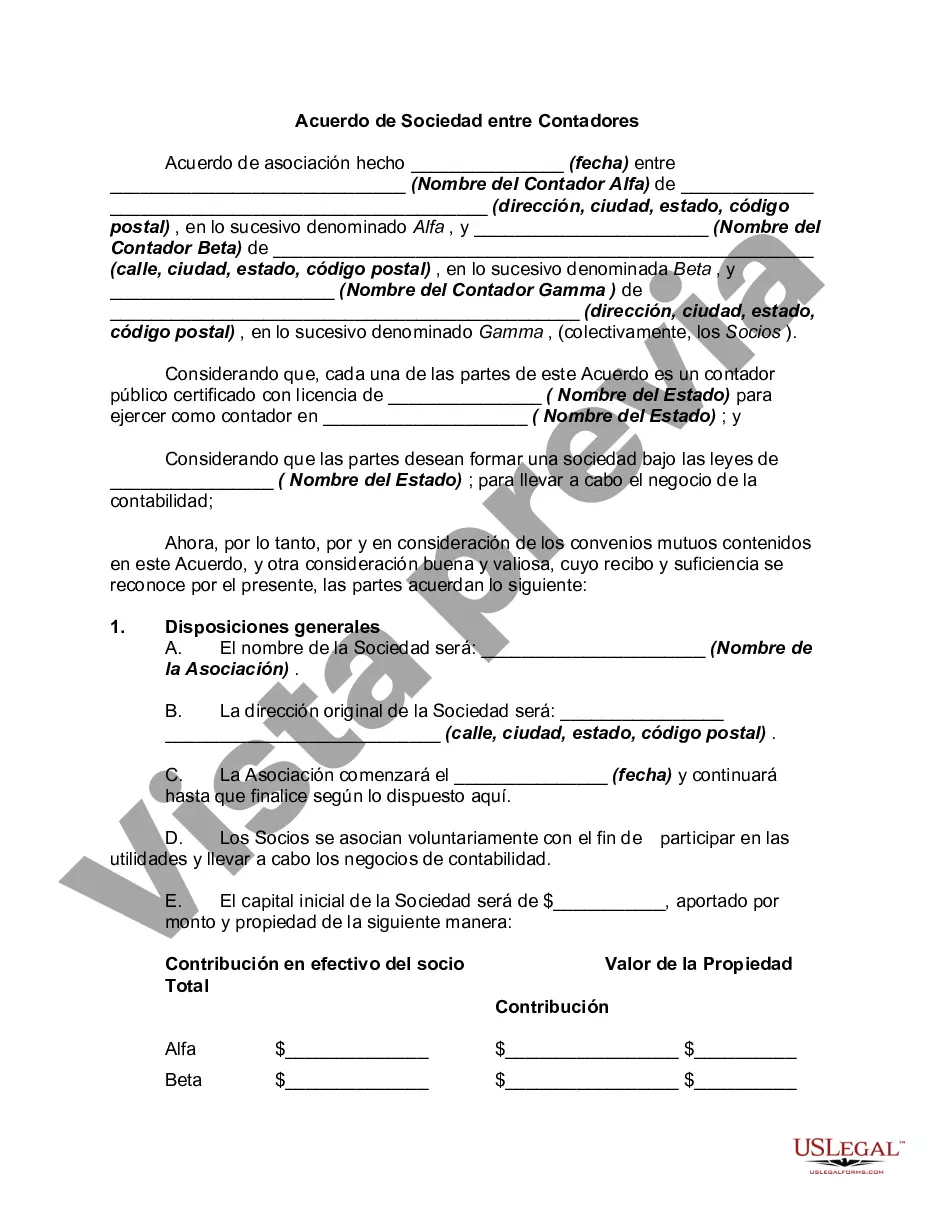

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.