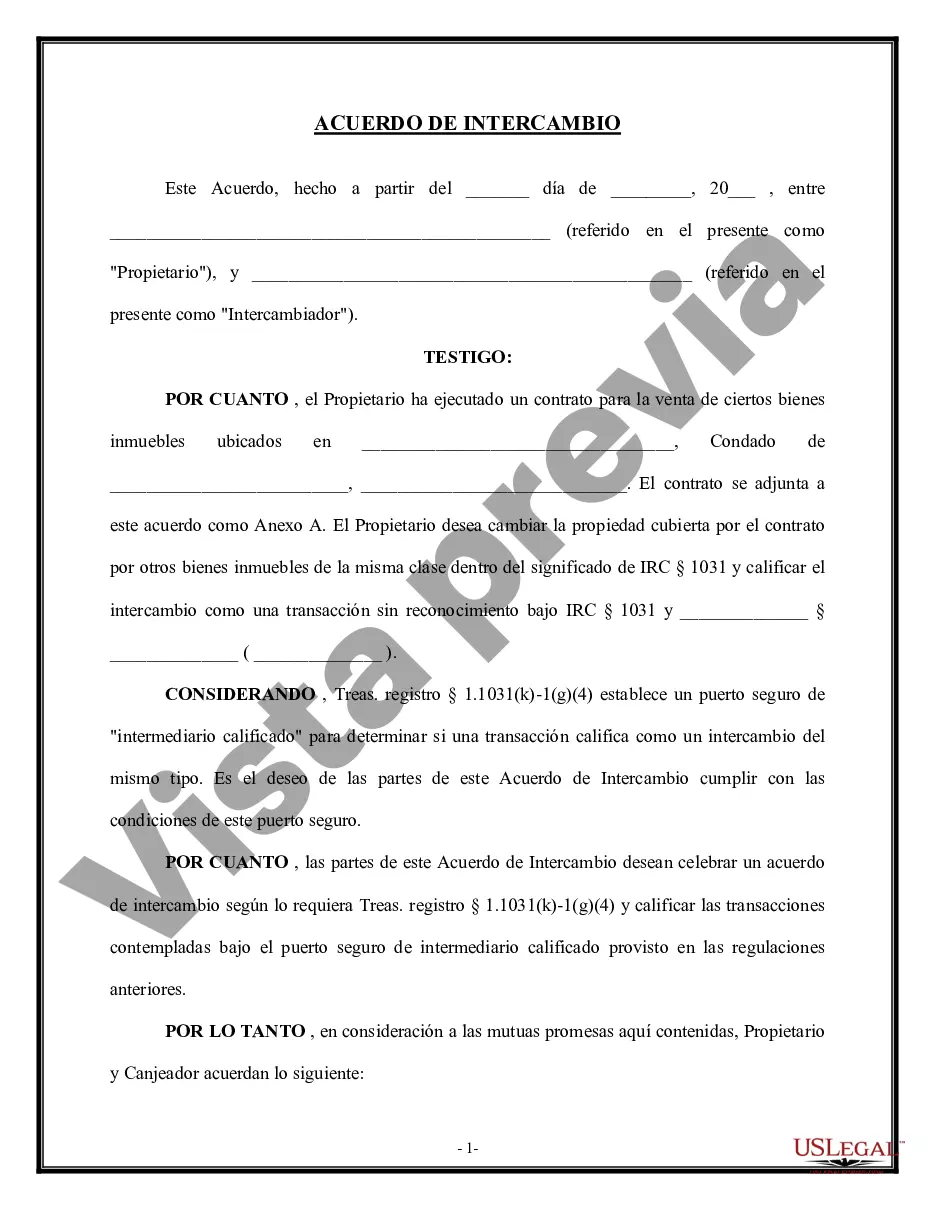

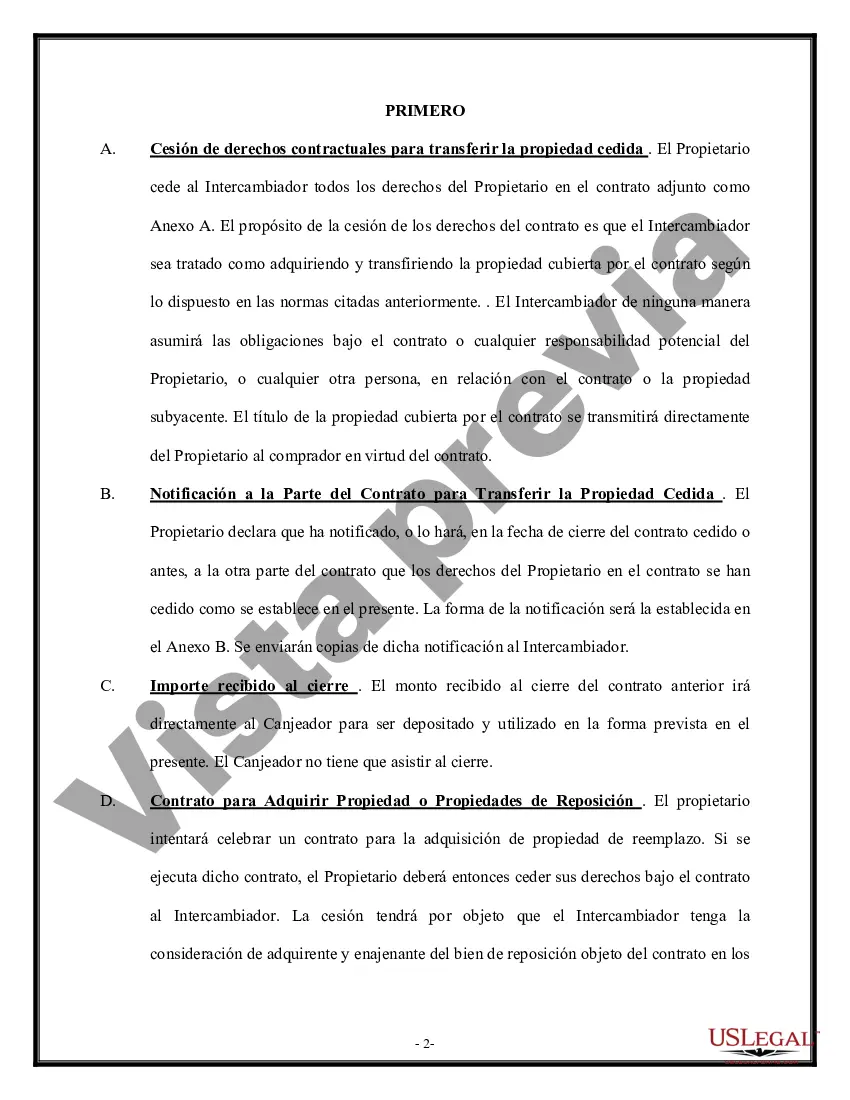

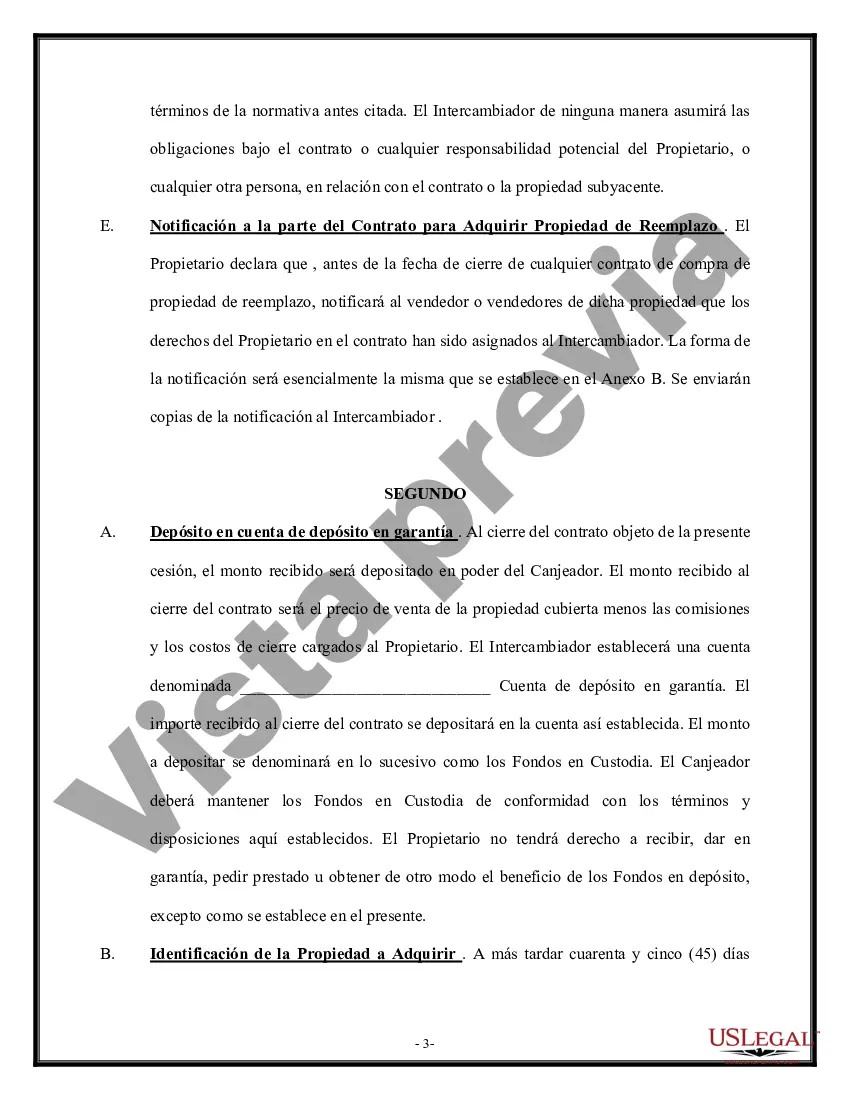

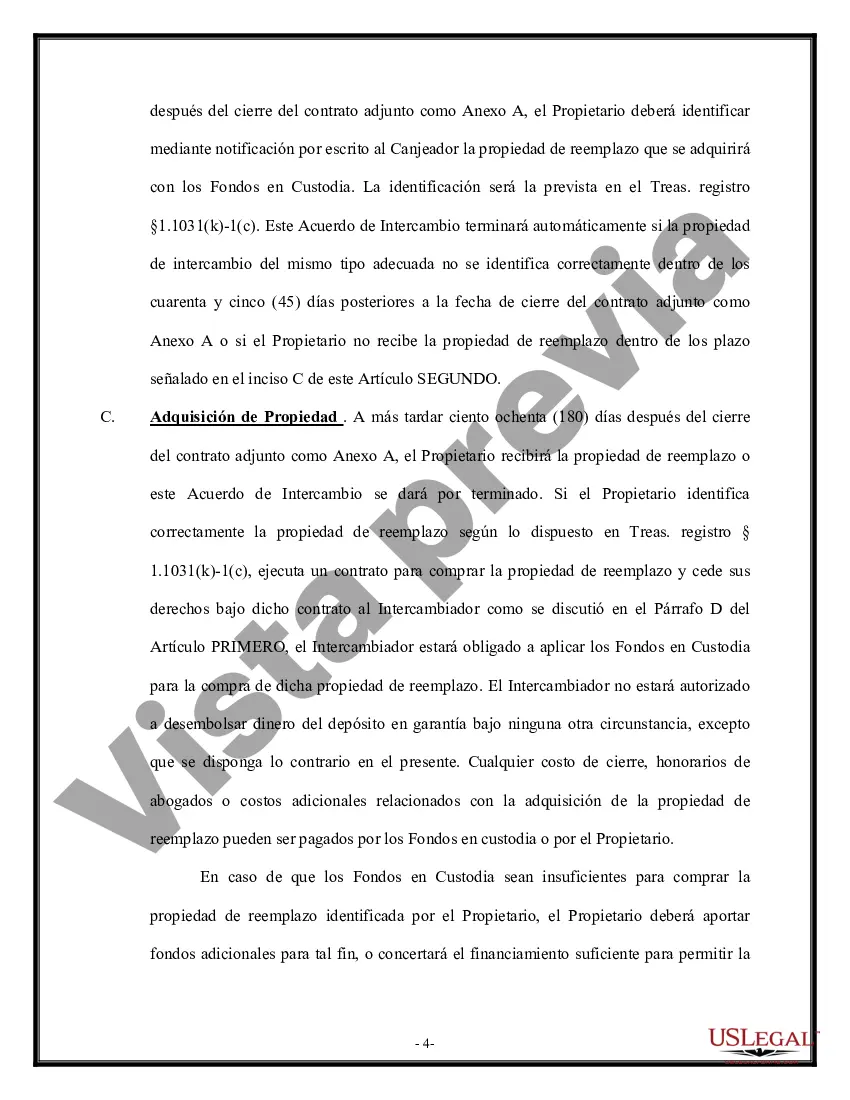

The Wisconsin Tax Free Exchange Agreement Section 1031 is a provision that allows individuals and businesses to dispose of their property and acquire a replacement property without incurring immediate tax liability on the capital gains. This exchange agreement, named after Section 1031 of the Internal Revenue Code, is widely used by taxpayers in Wisconsin to defer taxes on the sale of real estate, personal property, or other assets. Under the Wisconsin Tax Free Exchange Agreement Section 1031, taxpayers can defer paying capital gains taxes upon the sale of their property as long as they reinvest the proceeds into a like-kind replacement property. Like-kind refers to properties that are of the same nature or character, regardless of their quality or grade. This means that a taxpayer can exchange their commercial property for another commercial property, or even swap a residential property for a vacant land. There are several key benefits to utilizing the Wisconsin Tax Free Exchange Agreement Section 1031. Firstly, it allows taxpayers to defer the payment of capital gains taxes, potentially freeing up additional funds for investment purposes. Secondly, it provides individuals and businesses with the flexibility to reallocate their investments while preserving their equity. This provision encourages economic growth by fostering active property exchanges and stimulating investment activity. In Wisconsin, there are two primary types of tax-free exchange agreements that fall under Section 1031: simultaneous exchanges and delayed exchanges. 1. Simultaneous Exchange: In a simultaneous exchange, the taxpayer sells their property and acquires the replacement property in a single transaction. Both properties are transferred at the same time, ensuring a seamless exchange without the need for intermediaries or a delay in ownership. 2. Delayed Exchange: On the other hand, a delayed exchange, also known as a deferred exchange, occurs when the taxpayer sells their property first and subsequently purchases the replacement property within a specific timeframe. This timeframe is crucial and must be adhered to for the exchange to qualify for tax deferral. Within 45 days of selling their property, the taxpayer must identify potential replacement properties, and within 180 days, they must acquire one or more of the identified properties. In conclusion, the Wisconsin Tax Free Exchange Agreement Section 1031 provides individuals and businesses with a valuable opportunity to defer capital gains taxes by reinvesting proceeds into like-kind replacement properties. With simultaneous and delayed exchange options available, taxpayers have flexibility in executing these exchanges while enjoying the associated tax benefits. The provision's ability to stimulate economic growth and incentivize investment makes it a popular choice for taxpayers in Wisconsin.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Wisconsin Acuerdo de Intercambio Libre de Impuestos Sección 1031 - Tax Free Exchange Agreement Section 1031

Description

How to fill out Wisconsin Acuerdo De Intercambio Libre De Impuestos Sección 1031?

Are you in the place in which you require papers for sometimes organization or individual functions just about every day? There are plenty of authorized papers themes available on the net, but locating versions you can depend on is not straightforward. US Legal Forms provides thousands of kind themes, such as the Wisconsin Tax Free Exchange Agreement Section 1031, which can be written to satisfy federal and state needs.

If you are currently knowledgeable about US Legal Forms website and also have a free account, simply log in. After that, it is possible to down load the Wisconsin Tax Free Exchange Agreement Section 1031 design.

Unless you have an profile and want to begin using US Legal Forms, abide by these steps:

- Obtain the kind you need and ensure it is to the right metropolis/region.

- Take advantage of the Review option to review the shape.

- See the explanation to ensure that you have chosen the proper kind.

- If the kind is not what you are searching for, make use of the Lookup field to discover the kind that meets your requirements and needs.

- When you find the right kind, click Acquire now.

- Select the pricing strategy you would like, submit the desired information to make your account, and purchase the transaction using your PayPal or bank card.

- Pick a hassle-free data file formatting and down load your duplicate.

Locate each of the papers themes you may have bought in the My Forms menu. You may get a further duplicate of Wisconsin Tax Free Exchange Agreement Section 1031 at any time, if needed. Just click the needed kind to down load or printing the papers design.

Use US Legal Forms, by far the most considerable variety of authorized kinds, to save time as well as stay away from errors. The assistance provides skillfully manufactured authorized papers themes that you can use for a range of functions. Generate a free account on US Legal Forms and commence creating your daily life a little easier.