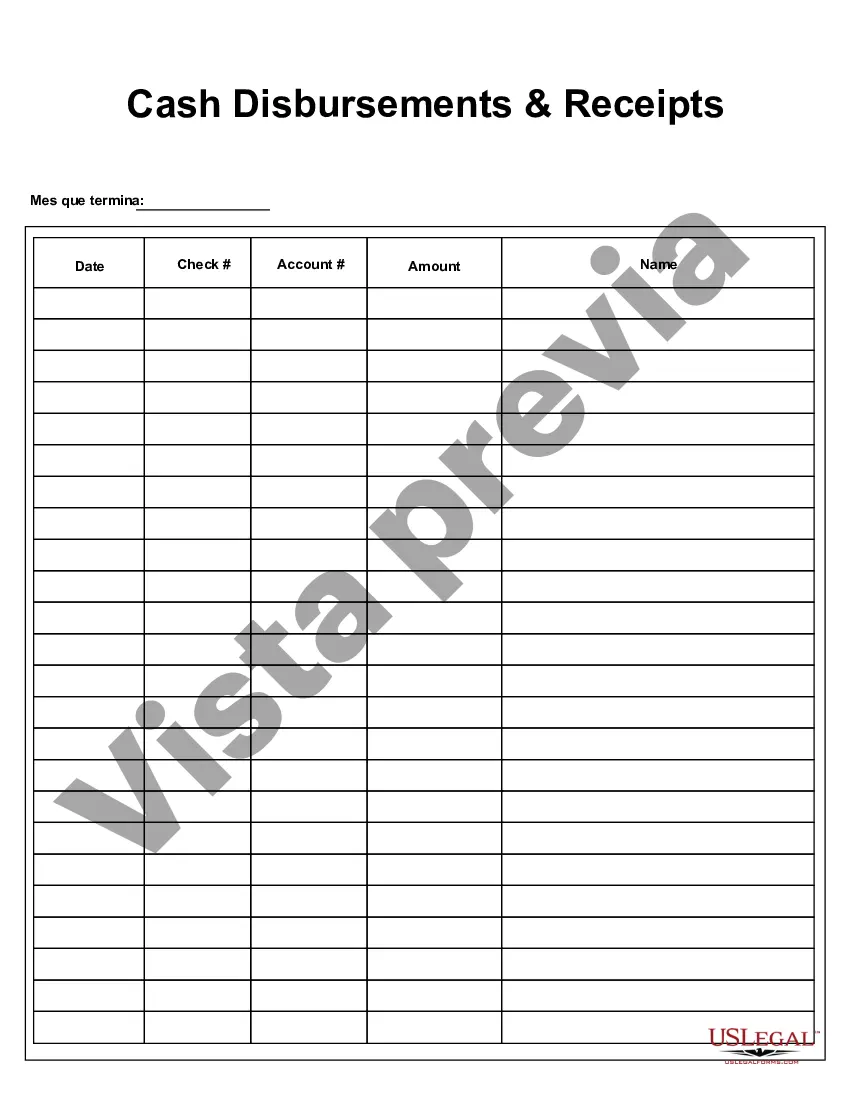

Wisconsin Cash Disbursements and Receipts are financial transactions that involve the payment and collection of funds or assets by the state of Wisconsin. These transactions are crucial for managing the state's budget and maintaining financial transparency. Cash disbursements refer to the outflow of funds from the state's treasury to pay for various expenses and obligations. These payments can include salaries and wages of government employees, payments to vendors and contractors, debt repayments, grants and subsidies, purchase of goods and services, and other expenditures authorized by the state legislature. The Wisconsin Department of Administration (DOA) oversees and ensures the proper disbursement of funds in accordance with established rules and regulations. On the other hand, cash receipts represent the inflow of funds or assets into the state's treasury. They primarily comprise revenue collected by the state government through taxes, fees, fines, licenses, and other sources. Cash receipts also include federal aid, donations, and other miscellaneous income. The Wisconsin Department of Revenue (FOR) plays a vital role in collecting, recording, and accounting for these receipts, ensuring compliance with tax laws and accounting standards. In terms of specific classifications, Wisconsin Cash Disbursements and Receipts can be further categorized into different types based on their nature and purpose. Some of these types include: 1. Personnel Service Payments: This category covers disbursements related to salaries, wages, and benefits of state employees, including regular pay, overtime, pension contributions, health insurance premiums, and other employment expenses. 2. Vendor Payments: This type encompasses disbursements to suppliers and contractors who provide goods, services, or construction-related activities to state agencies. These disbursements can include payments for office supplies, equipment, utilities, maintenance, and professional services. 3. Debt Service Payments: These disbursements consist of payments made towards the state's outstanding debts, such as principal and interest on loans, bonds, or other forms of financing. 4. Grants and Subsidies: This category includes disbursements made to organizations, non-profits, local governments, or individuals through various grant programs or subsidies administered by the state. These disbursements aim to support education, healthcare, infrastructure development, economic development, and social welfare initiatives. 5. Tax and Fee Collections: This type of cash receipt represents the revenue generated from taxes (e.g., income tax, sales tax, property tax) and fees (e.g., license fees, permit fees) imposed by the state on individuals, businesses, and other entities. 6. Federal Aid Receipts: Wisconsin receives federal funds for various programs and projects, including Medicaid, transportation, education, and emergency response. These funds are considered cash receipts and play a significant role in financing state initiatives. It is important for the state of Wisconsin to closely monitor and administer its cash disbursements and receipts to ensure fiscal responsibility and accountability. By properly managing these transactions, the state can effectively allocate resources, meet financial obligations, and support the welfare and development of its residents.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Wisconsin Desembolsos y recibos de efectivo - Cash Disbursements and Receipts

Description

How to fill out Wisconsin Desembolsos Y Recibos De Efectivo?

US Legal Forms - one of several most significant libraries of legal forms in the USA - provides an array of legal papers web templates it is possible to down load or printing. Utilizing the web site, you can find a huge number of forms for business and individual uses, categorized by types, states, or search phrases.You will find the newest models of forms such as the Wisconsin Cash Disbursements and Receipts in seconds.

If you currently have a subscription, log in and down load Wisconsin Cash Disbursements and Receipts from the US Legal Forms collection. The Obtain button will appear on each and every kind you view. You gain access to all in the past saved forms from the My Forms tab of the bank account.

If you would like use US Legal Forms for the first time, listed below are basic directions to help you started:

- Be sure you have picked out the right kind to your metropolis/region. Go through the Preview button to examine the form`s content. Browse the kind information to ensure that you have selected the correct kind.

- In the event the kind doesn`t fit your needs, use the Search discipline at the top of the display to find the one which does.

- If you are happy with the shape, confirm your selection by clicking on the Acquire now button. Then, choose the prices program you like and offer your qualifications to register on an bank account.

- Process the purchase. Make use of your credit card or PayPal bank account to perform the purchase.

- Find the formatting and down load the shape on your product.

- Make modifications. Fill out, modify and printing and indication the saved Wisconsin Cash Disbursements and Receipts.

Every single design you put into your bank account lacks an expiry time and is your own property forever. So, if you wish to down load or printing one more backup, just visit the My Forms section and click on about the kind you will need.

Gain access to the Wisconsin Cash Disbursements and Receipts with US Legal Forms, one of the most comprehensive collection of legal papers web templates. Use a huge number of professional and express-specific web templates that satisfy your small business or individual requirements and needs.