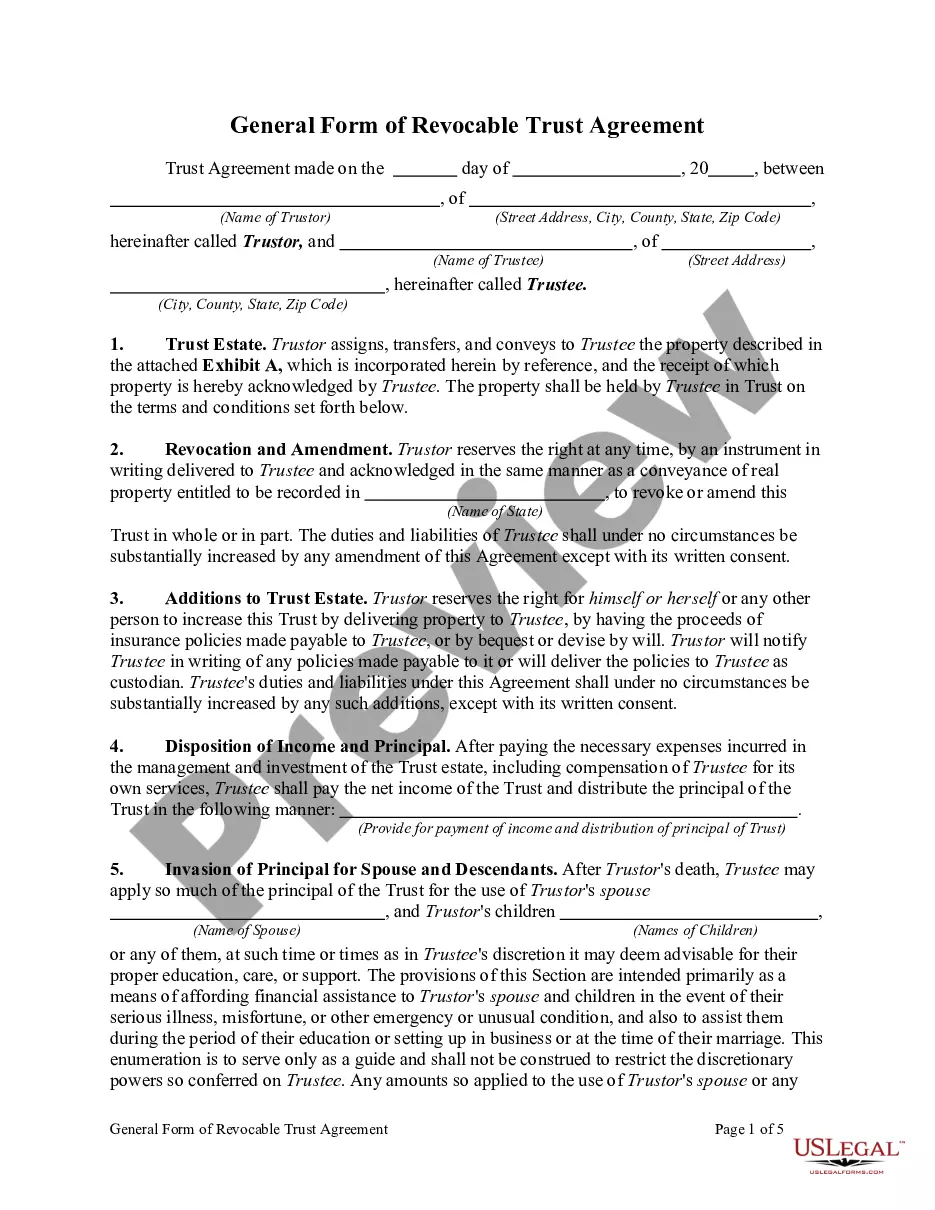

West Virginia Qualifying Subchapter-S Revocable Trust Agreement

Description

How to fill out Qualifying Subchapter-S Revocable Trust Agreement?

Locating the appropriate legal document format can be challenging.

Of course, there are numerous templates accessible online, but how do you acquire the official form you require.

Utilize the US Legal Forms website. This service offers a vast array of templates, such as the West Virginia Qualifying Subchapter-S Revocable Trust Agreement, which can be utilized for both business and personal purposes.

First, ensure you have selected the correct form for your city/region. You can check the document using the Preview option and review the document description to confirm it is suitable for you. If the form does not meet your requirements, utilize the Search feature to find the correct form. Once you are confident that the document is appropriate, click the Purchase now button to obtain the form. Select the pricing plan you prefer and enter the necessary information. Create your account and pay for the order using your PayPal account or credit card. Choose the document format and download the legal document template to your device. Complete, edit, print, and sign the received West Virginia Qualifying Subchapter-S Revocable Trust Agreement. US Legal Forms is the largest repository of legal forms where you can find various document templates. Utilize the service to download properly crafted documents that comply with state requirements.

- All forms are reviewed by professionals and comply with federal and state regulations.

- If you are currently registered, sign in to your account and click the Download option to obtain the West Virginia Qualifying Subchapter-S Revocable Trust Agreement.

- Utilize your account to search for the legal forms you have previously acquired.

- Navigate to the My documents section of your account to obtain another copy of the documents you need.

- If you are a new user of US Legal Forms, here are simple instructions for you to follow.

Form popularity

FAQ

The trust's current income beneficiary must make the QSST election under Sec. 1361(d)(2), by filing a statement with the information and in the manner prescribed by Regs.

The fundamental problem is that trusts and S corporations do not play well together. Although a trust (including a Living Trust) can be a permitted shareholder in an S corporation, only certain kinds of trusts are so permitted under Section 1361 of the Internal Revenue Code.

The main difference between an ESBT and a QSST is that an ESBT may have multiple income beneficiaries, and the trust does not have to distribute all income. Unlike with the QSST, the trustee, rather than the beneficiary, must make the election.

An irrevocable trust that is setup as a grantor trust, qualified subchapter S trust or as an electing small business trust may own shares of an S corporation.

TRUSTS COMMONLY USED TO HOLD S CORPORATION STOCK Three commonly used types of ongoing trusts qualify as S corporation shareholders: grantor trusts, qualified subchapter S trusts (QSSTs) and electing small business trusts (ESBTs).

A Qualified Subchapter S Trust, commonly referred to as a QSST Election, or a Q-Sub election, is a Qualified Subchapter S Subsidiary Election made on behalf of a trust that retains ownership as the shareholder of an S corporation, a corporation in the United States which votes to be taxed.

The regulations allow in Secs. 1.1361-1(m)(2)(iii) and (j)(6)(iii) for the ESBT election to be made within the two-months-and-15-day period beginning on the day the trust received the S corporation stock. The election is made by completing and filing the statement described in Reg. Sec.

In the most common scenario, in order for a grantor trust, such as a joint revocable trust, to remain an S-corporation shareholder, the trust should allow for the distribution of the S-corporation stock to a permissible shareholder within two years after your death.

A trust can hold stock in an S corp only if it (1) is treated as owned by its grantor for income tax purposes under us grantor trust rules, (2) was a grantor trust immediately before its grantor's death (the trust can be a shareholder only for two years from that date), (3) received stock from the will of a decedent (

Since a revocable trust is not treated as separate from the grantor, it is an eligible S corporation shareholder while the grantor is alive.