As most commonly used in legal settings, an audit is an examination of financial records and documents and other evidence by a trained accountant. Audits are conducted of records of a business or governmental entity, with the aim of ensuring proper accounting practices, recommendations for improvements, and a balancing of the books. An audit performed by employees is called "internal audit," and one done by an independent (outside) accountant is an "independent audit." Auditors may refuse to sign the audit to guarantee its accuracy if only limited records are produced.

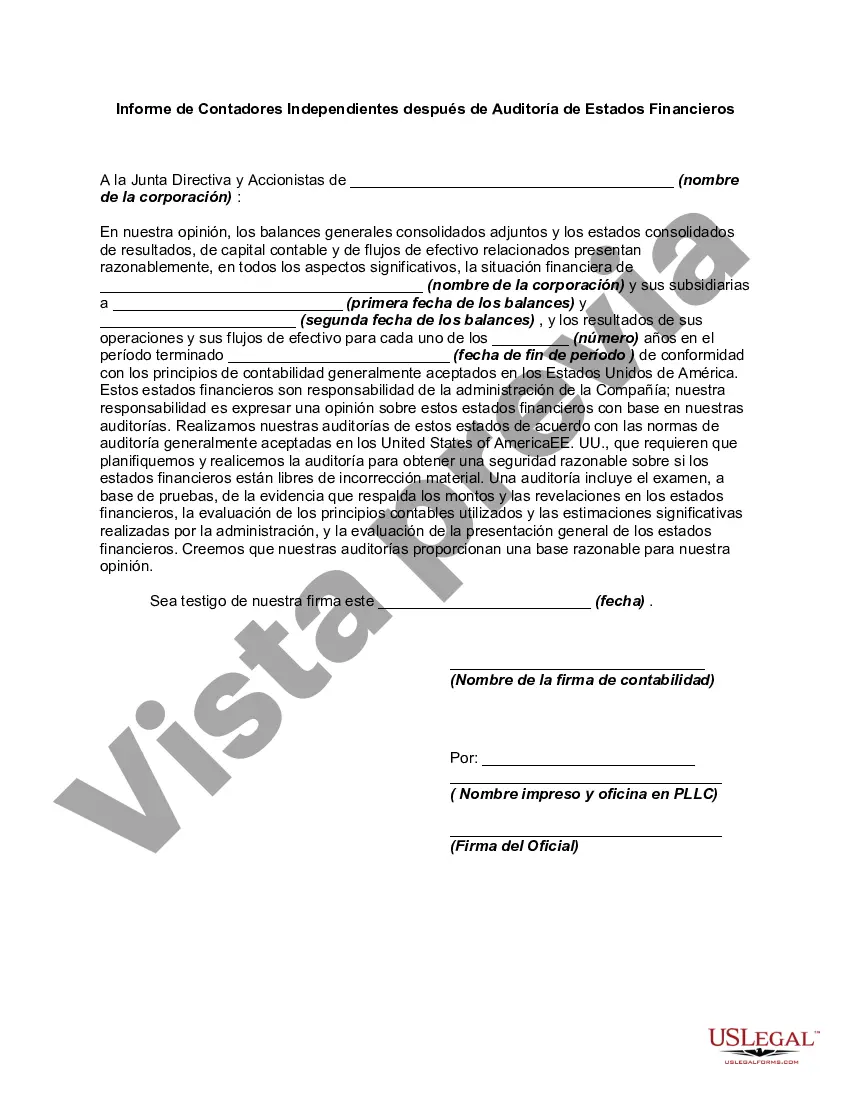

A Wyoming Report of Independent Accountants after Audit of Financial Statements is a document that summarizes the results of an independent audit conducted on the financial statements of an entity based in Wyoming. This report is prepared by an independent accounting firm and serves as a critical tool for stakeholders, including shareholders, investors, creditors, and regulatory bodies, to evaluate the financial performance, transparency, and compliance of the audited organization. The primary objective of the Wyoming Report of Independent Accountants after Audit of Financial Statements is to provide an impartial opinion on the fairness and accuracy of the financial information presented by the audited entity. The report typically includes the following key components: 1. Title: The report is titled "Report of Independent Accountants after Audit of Financial Statements" or a variation that includes the name of the accounting firm and the specific period covered by the audit. 2. Addressee: The report explicitly states to whom it is addressed, typically the board of directors, shareholders, or other intended users. 3. Introductory Paragraph: This section provides a brief overview of the audit engagement, including the scope and objectives of the audit. 4. Management's Responsibility for Financial Statements: This portion delineates the responsibilities of the audited entity's management in preparing the financial statements and maintaining internal controls. 5. Auditor's Responsibility: The report discusses the responsibilities of the independent accounting firm, which includes conducting the audit in accordance with relevant auditing standards, obtaining sufficient and appropriate audit evidence, and forming an opinion on the financial statements. 6. Opinion Paragraph: The Utah Report of Independent Accountants after Audit of Financial Statements concludes with the auditor's opinion on the fairness of the financial statements. The opinion can be one of the following types: a. Unqualified Opinion: This is the most desirable type of opinion and indicates that the financial statements are presented fairly, in all material respects, in accordance with the applicable financial reporting framework. b. Qualified Opinion: A qualified opinion is issued when the auditor identifies a limitation or disagreement in applying accounting principles, scope restriction in the audit, or an inadequate presentation of information. This opinion indicates that the financial statements may not be fully in accordance with the applicable financial reporting framework. c. Adverse Opinion: An adverse opinion is the most severe type of opinion, indicating that the financial statements are not presented fairly, in all material respects, in accordance with the applicable financial reporting framework. d. Disclaimer of Opinion: In rare cases, if the auditor is unable to obtain sufficient evidence or encounters significant scope limitations, they may issue a disclaimer of opinion, indicating that no opinion can be expressed on the financial statements. 7. Other Reporting Paragraphs: The Wyoming Report of Independent Accountants after Audit of Financial Statements may also include additional reporting paragraphs, such as emphasis of matters, going concern considerations, or explanatory paragraphs regarding significant accounting policies or practices. It is crucial to note that the specific content and structure of the Wyoming Report of Independent Accountants after Audit of Financial Statements may vary depending on the applicable auditing standards and regulations, the complexity and size of the audited entity, and specific reporting requirements. Professional judgment and adherence to professional standards are essential during the preparation and issuance of this report.A Wyoming Report of Independent Accountants after Audit of Financial Statements is a document that summarizes the results of an independent audit conducted on the financial statements of an entity based in Wyoming. This report is prepared by an independent accounting firm and serves as a critical tool for stakeholders, including shareholders, investors, creditors, and regulatory bodies, to evaluate the financial performance, transparency, and compliance of the audited organization. The primary objective of the Wyoming Report of Independent Accountants after Audit of Financial Statements is to provide an impartial opinion on the fairness and accuracy of the financial information presented by the audited entity. The report typically includes the following key components: 1. Title: The report is titled "Report of Independent Accountants after Audit of Financial Statements" or a variation that includes the name of the accounting firm and the specific period covered by the audit. 2. Addressee: The report explicitly states to whom it is addressed, typically the board of directors, shareholders, or other intended users. 3. Introductory Paragraph: This section provides a brief overview of the audit engagement, including the scope and objectives of the audit. 4. Management's Responsibility for Financial Statements: This portion delineates the responsibilities of the audited entity's management in preparing the financial statements and maintaining internal controls. 5. Auditor's Responsibility: The report discusses the responsibilities of the independent accounting firm, which includes conducting the audit in accordance with relevant auditing standards, obtaining sufficient and appropriate audit evidence, and forming an opinion on the financial statements. 6. Opinion Paragraph: The Utah Report of Independent Accountants after Audit of Financial Statements concludes with the auditor's opinion on the fairness of the financial statements. The opinion can be one of the following types: a. Unqualified Opinion: This is the most desirable type of opinion and indicates that the financial statements are presented fairly, in all material respects, in accordance with the applicable financial reporting framework. b. Qualified Opinion: A qualified opinion is issued when the auditor identifies a limitation or disagreement in applying accounting principles, scope restriction in the audit, or an inadequate presentation of information. This opinion indicates that the financial statements may not be fully in accordance with the applicable financial reporting framework. c. Adverse Opinion: An adverse opinion is the most severe type of opinion, indicating that the financial statements are not presented fairly, in all material respects, in accordance with the applicable financial reporting framework. d. Disclaimer of Opinion: In rare cases, if the auditor is unable to obtain sufficient evidence or encounters significant scope limitations, they may issue a disclaimer of opinion, indicating that no opinion can be expressed on the financial statements. 7. Other Reporting Paragraphs: The Wyoming Report of Independent Accountants after Audit of Financial Statements may also include additional reporting paragraphs, such as emphasis of matters, going concern considerations, or explanatory paragraphs regarding significant accounting policies or practices. It is crucial to note that the specific content and structure of the Wyoming Report of Independent Accountants after Audit of Financial Statements may vary depending on the applicable auditing standards and regulations, the complexity and size of the audited entity, and specific reporting requirements. Professional judgment and adherence to professional standards are essential during the preparation and issuance of this report.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.