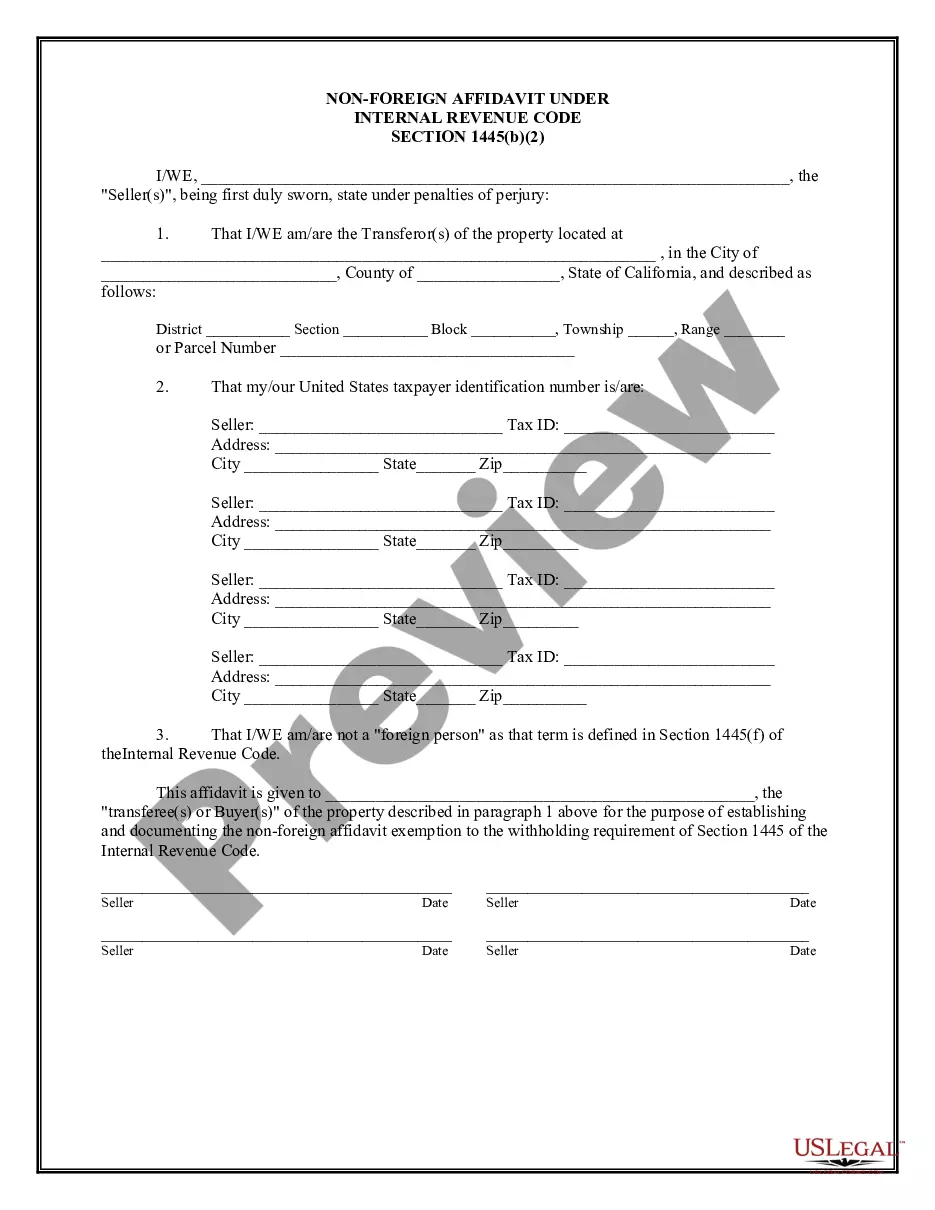

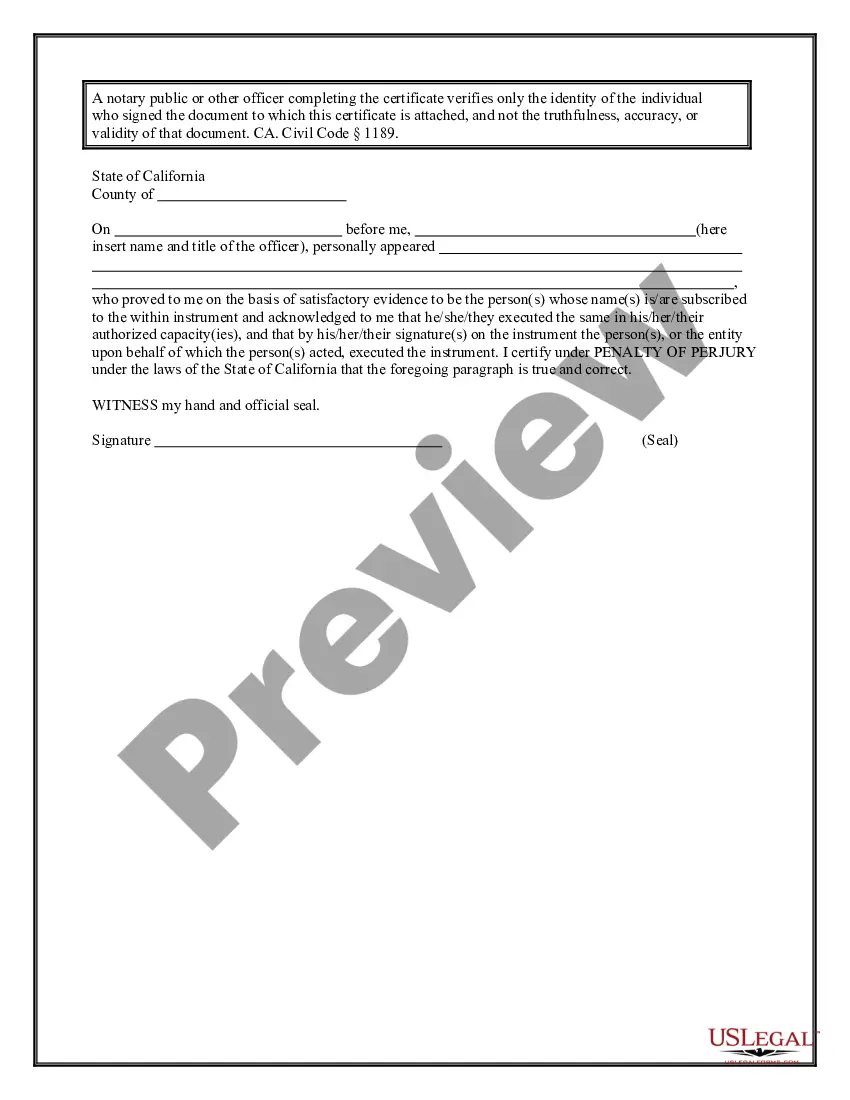

This Non-Foreign Affdavit Under Internal Revenue Code 1445 is for a seller of real property to sign stating that he or she is not a foreign person as defined by the Internal Revenue Code Section 26 USC 1445. This document must be signed and notarized.

A Santa Maria California Non-Foreign Affidavit Under IRC 1445 is a legal document that is necessary to be filed by a non-foreign individual or entity involved in real estate transactions in Santa Maria, California. This affidavit is required by the Internal Revenue Code (IRC) section 1445, which deals with the withholding of tax on dispositions by foreign persons of U.S. real property interests. The purpose of the Santa Maria California Non-Foreign Affidavit Under IRC 1445 is to certify that the seller of the real property is not a foreign person as defined by the IRC. This declaration is crucial as it determines whether the buyer or other withholding agent needs to withhold tax on the disposition of the property. In Santa Maria, there are different types of Non-Foreign Affidavits Under IRC 1445, depending on the specific circumstances of the real estate transaction: 1. Individual Non-Foreign Affidavit: This type of affidavit is used when the seller is an individual (U.S. citizen, lawful permanent resident, or resident alien for tax purposes) and is not considered a foreign person under the IRC. 2. Entity Non-Foreign Affidavit: If the seller is an entity, such as a corporation, partnership, trust, or estate, this affidavit is required to declare that the entity is not a foreign person and should not be subject to foreign withholding tax. 3. Trust Non-Foreign Affidavit: When a trust is involved in the sale of the property, a Trust Non-Foreign Affidavit is necessary to ensure that the trust is not considered a foreign person under the IRC guidelines. 4. Estate Non-Foreign Affidavit: In the case of a property being sold as part of an estate, an Estate Non-Foreign Affidavit is filed to verify that the estate is not a foreign person according to IRC regulations. It is important to note that failure to comply with the requirements of filing a Santa Maria California Non-Foreign Affidavit Under IRC 1445 can lead to penalties, fines, and potential legal complications for all parties involved in the real estate transaction. Therefore, it is advisable for sellers and their legal representatives to carefully review the IRS regulations and seek professional assistance to accurately complete the required affidavit.A Santa Maria California Non-Foreign Affidavit Under IRC 1445 is a legal document that is necessary to be filed by a non-foreign individual or entity involved in real estate transactions in Santa Maria, California. This affidavit is required by the Internal Revenue Code (IRC) section 1445, which deals with the withholding of tax on dispositions by foreign persons of U.S. real property interests. The purpose of the Santa Maria California Non-Foreign Affidavit Under IRC 1445 is to certify that the seller of the real property is not a foreign person as defined by the IRC. This declaration is crucial as it determines whether the buyer or other withholding agent needs to withhold tax on the disposition of the property. In Santa Maria, there are different types of Non-Foreign Affidavits Under IRC 1445, depending on the specific circumstances of the real estate transaction: 1. Individual Non-Foreign Affidavit: This type of affidavit is used when the seller is an individual (U.S. citizen, lawful permanent resident, or resident alien for tax purposes) and is not considered a foreign person under the IRC. 2. Entity Non-Foreign Affidavit: If the seller is an entity, such as a corporation, partnership, trust, or estate, this affidavit is required to declare that the entity is not a foreign person and should not be subject to foreign withholding tax. 3. Trust Non-Foreign Affidavit: When a trust is involved in the sale of the property, a Trust Non-Foreign Affidavit is necessary to ensure that the trust is not considered a foreign person under the IRC guidelines. 4. Estate Non-Foreign Affidavit: In the case of a property being sold as part of an estate, an Estate Non-Foreign Affidavit is filed to verify that the estate is not a foreign person according to IRC regulations. It is important to note that failure to comply with the requirements of filing a Santa Maria California Non-Foreign Affidavit Under IRC 1445 can lead to penalties, fines, and potential legal complications for all parties involved in the real estate transaction. Therefore, it is advisable for sellers and their legal representatives to carefully review the IRS regulations and seek professional assistance to accurately complete the required affidavit.