An Elgin Illinois Installments Fixed Rate Promissory Note Secured by Personal Property is a legal document that outlines the terms and conditions of a loan agreement between a lender and a borrower. This type of promissory note is specific to the city of Elgin in Illinois, and is often used when the borrower wishes to secure the loan using their personal property as collateral. The Elgin Illinois Installments Fixed Rate Promissory Note secures the loan by establishing a lien on the borrower's personal property, such as a vehicle, real estate, or valuable possessions. This provides the lender with a level of security, as they can claim the collateral in case the borrower defaults on the loan. The promissory note details the repayment terms, including the principal amount, interest rate, installment amounts, and the frequency of payments. It also specifies the consequences of defaulting on the loan, such as additional fees, penalties, or legal action. Different types of Elgin Illinois Installments Fixed Rate Promissory Note Secured by Personal Property may vary based on the specific terms of the loan, the type of personal property being used as collateral, and any additional agreements or clauses included in the document. For instance, there might be variations in interest rates, loan durations, or clauses related to prepayment options, late payments, or refinancing. By including specific keywords related to the topic, we can enhance the content's relevance and search engine visibility: 1. Elgin Illinois Installments Fixed Rate Promissory Note: This is the main type of promissory note used in Elgin, Illinois, and typically involves the repayment of a loan in regular installments at a fixed interest rate over a specific period. 2. Personal Property Collateral: This refers to the assets owned by the borrower, like vehicles, valuables, or real estate, that are used to secure the loan. 3. Loan Agreement: The promissory note serves as a formal agreement between the lender and borrower, outlining the terms, conditions, and repayment obligations. 4. Lien: The promissory note establishes a lien on the borrower's personal property, ensuring that the lender has a legal claim on those assets if the borrower defaults on payment. 5. Default: When the borrower fails to fulfill the obligations outlined in the promissory note, such as missing payments or breaching the terms, it is considered a default. 6. Interest Rate: This refers to the percentage charged by the lender on the principal loan amount, which is an important factor in determining the overall cost of the loan for the borrower. 7. Installment Payments: The borrower is required to make regular installment payments, often monthly or quarterly, to repay the loan over a specified period. 8. Prepayment Options: Some promissory notes may provide the borrower with the option to make additional lump-sum payments before the due date or pay off the loan in full without incurring penalties. It is important to seek legal advice or consult with professionals when dealing with promissory notes, as variations may exist in specific terms and regulations across different areas and jurisdictions.

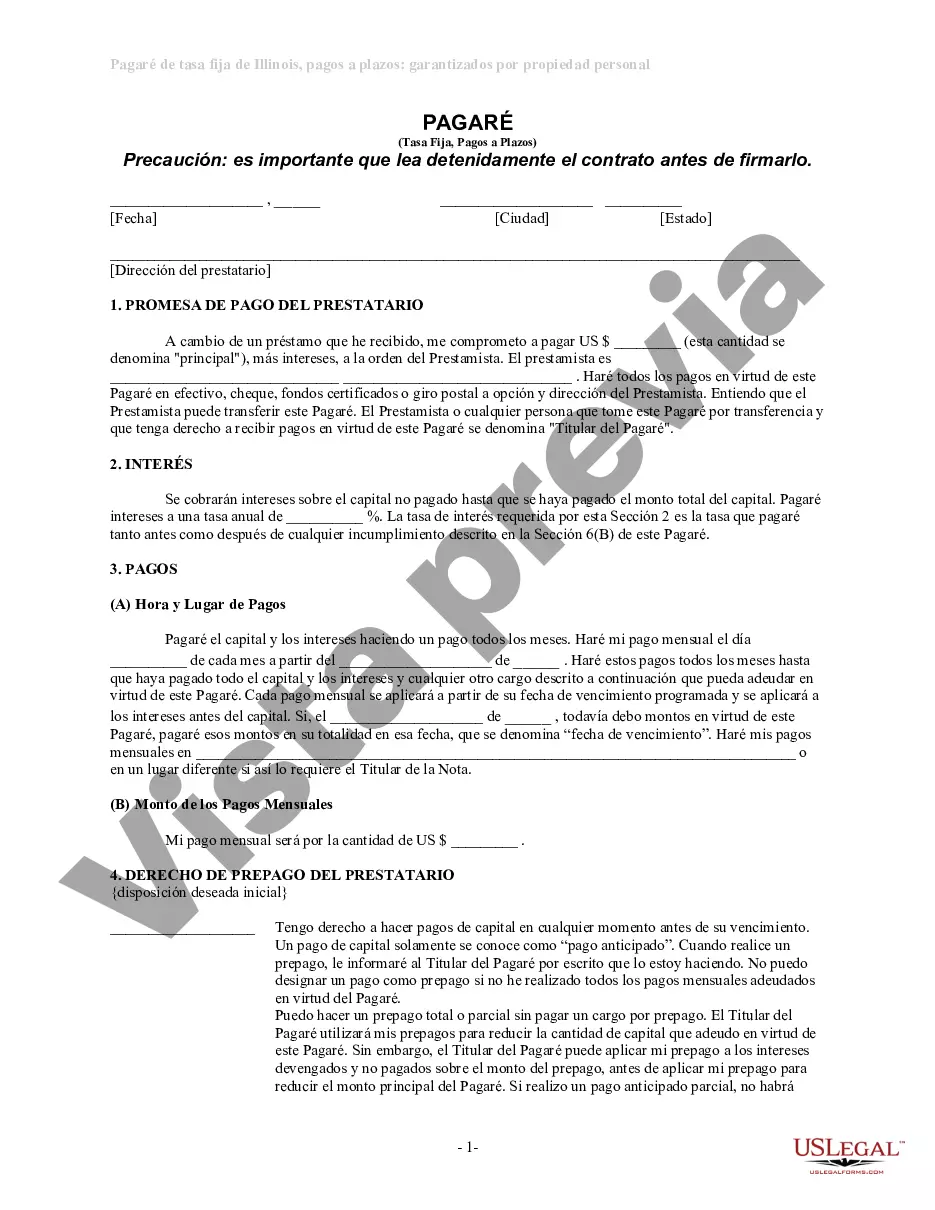

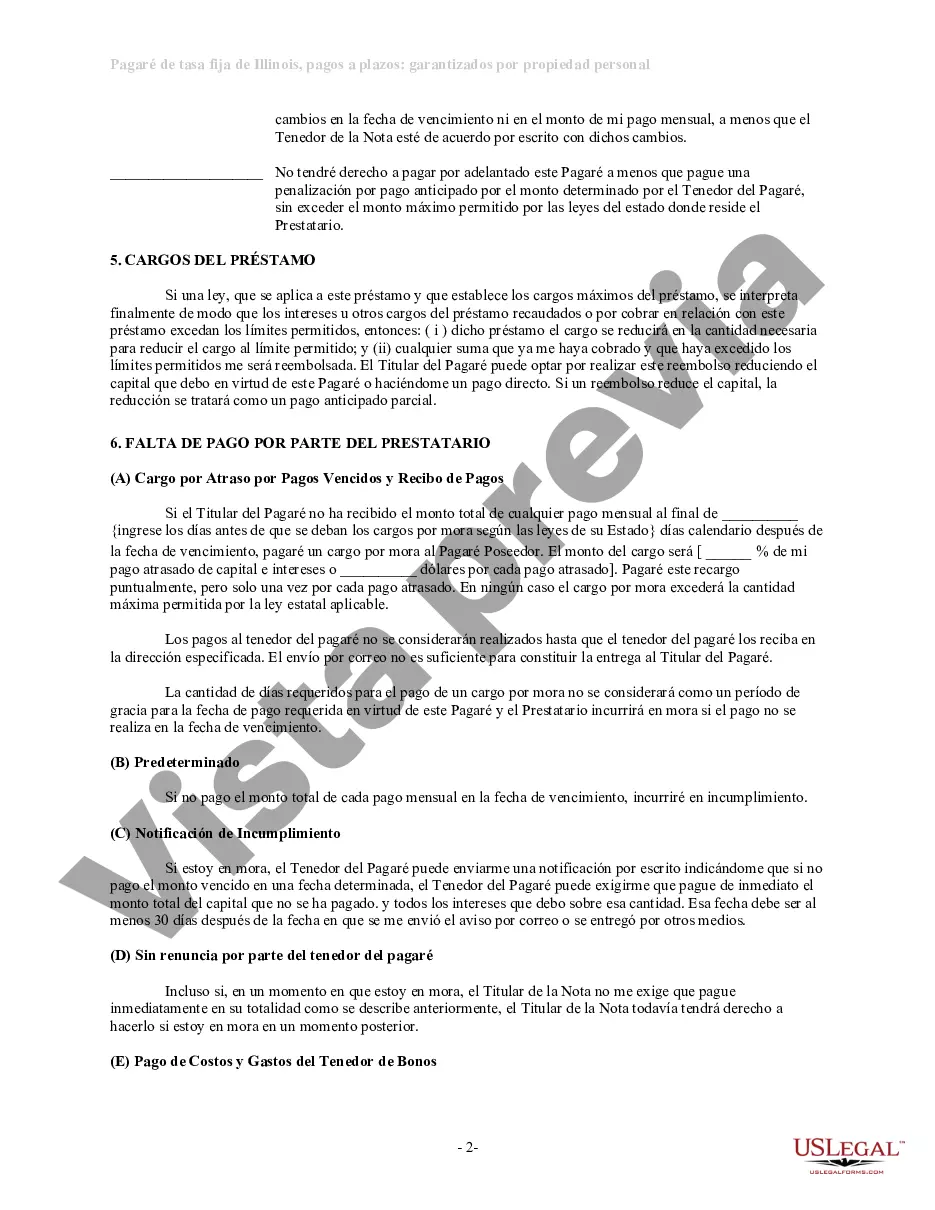

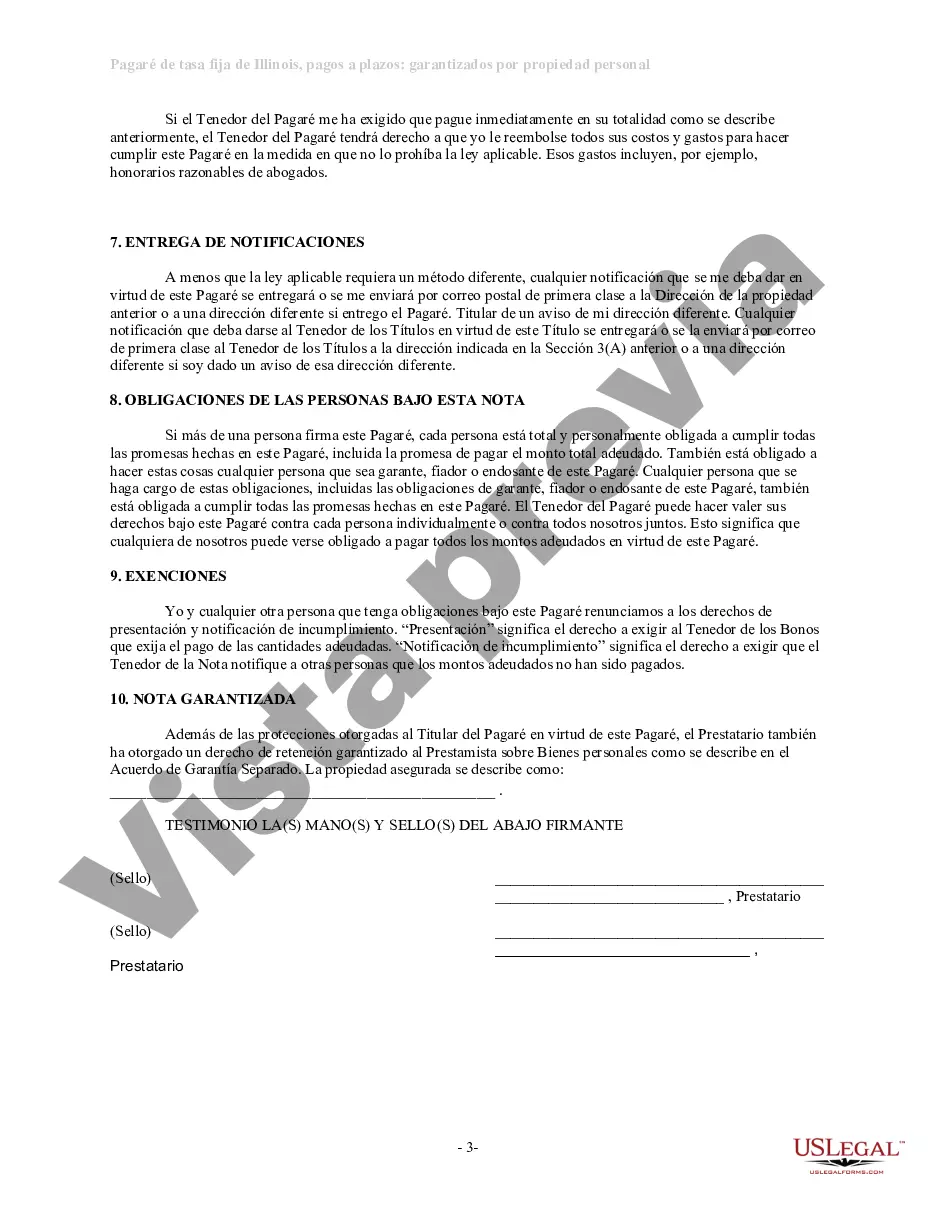

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Elgin Pagaré de tasa fija a plazos de Illinois garantizado por propiedad personal - Illinois Installments Fixed Rate Promissory Note Secured by Personal Property

Description

How to fill out Elgin Pagaré De Tasa Fija A Plazos De Illinois Garantizado Por Propiedad Personal?

No matter the social or professional status, filling out legal documents is an unfortunate necessity in today’s world. Too often, it’s practically impossible for someone with no legal education to create such paperwork cfrom the ground up, mostly due to the convoluted jargon and legal nuances they entail. This is where US Legal Forms comes to the rescue. Our service offers a huge library with over 85,000 ready-to-use state-specific documents that work for pretty much any legal case. US Legal Forms also is a great asset for associates or legal counsels who want to save time using our DYI forms.

Whether you require the Elgin Illinois Installments Fixed Rate Promissory Note Secured by Personal Property or any other document that will be valid in your state or area, with US Legal Forms, everything is at your fingertips. Here’s how you can get the Elgin Illinois Installments Fixed Rate Promissory Note Secured by Personal Property quickly employing our trustworthy service. If you are presently a subscriber, you can go ahead and log in to your account to download the appropriate form.

Nevertheless, if you are unfamiliar with our library, ensure that you follow these steps before obtaining the Elgin Illinois Installments Fixed Rate Promissory Note Secured by Personal Property:

- Ensure the template you have chosen is good for your location since the regulations of one state or area do not work for another state or area.

- Preview the form and read a quick description (if available) of scenarios the paper can be used for.

- In case the form you chosen doesn’t meet your requirements, you can start over and search for the necessary form.

- Click Buy now and pick the subscription option that suits you the best.

- with your credentials or create one from scratch.

- Select the payment gateway and proceed to download the Elgin Illinois Installments Fixed Rate Promissory Note Secured by Personal Property once the payment is through.

You’re good to go! Now you can go ahead and print the form or complete it online. If you have any issues locating your purchased documents, you can quickly find them in the My Forms tab.

Whatever situation you’re trying to sort out, US Legal Forms has got you covered. Give it a try today and see for yourself.