An AB trust is a trust created by a married couple to avoid probate and minimize federal estate tax. An AB trust is created by each spouse placing property into a trust and naming someone other than his or her spouse as the final beneficiary of that trust. Upon the death of the first spouse, the surviving spouse does not own the assets in that spouse's trust outright, but has a limited power over the assets in accordance with the terms of the trust. Such powers may include the right to receive interest or income earned by the trust, to use the trust property during his or her lifetime, e.g. to live in a house, and/or to use the trust principal for his or her health, education, or support. Upon the death of the second spouse, the trust passes to the final beneficiary of the trust. For estate tax purposes, the trust is included in the first, but not the second, spouse's estate and therefore, avoids double taxation.

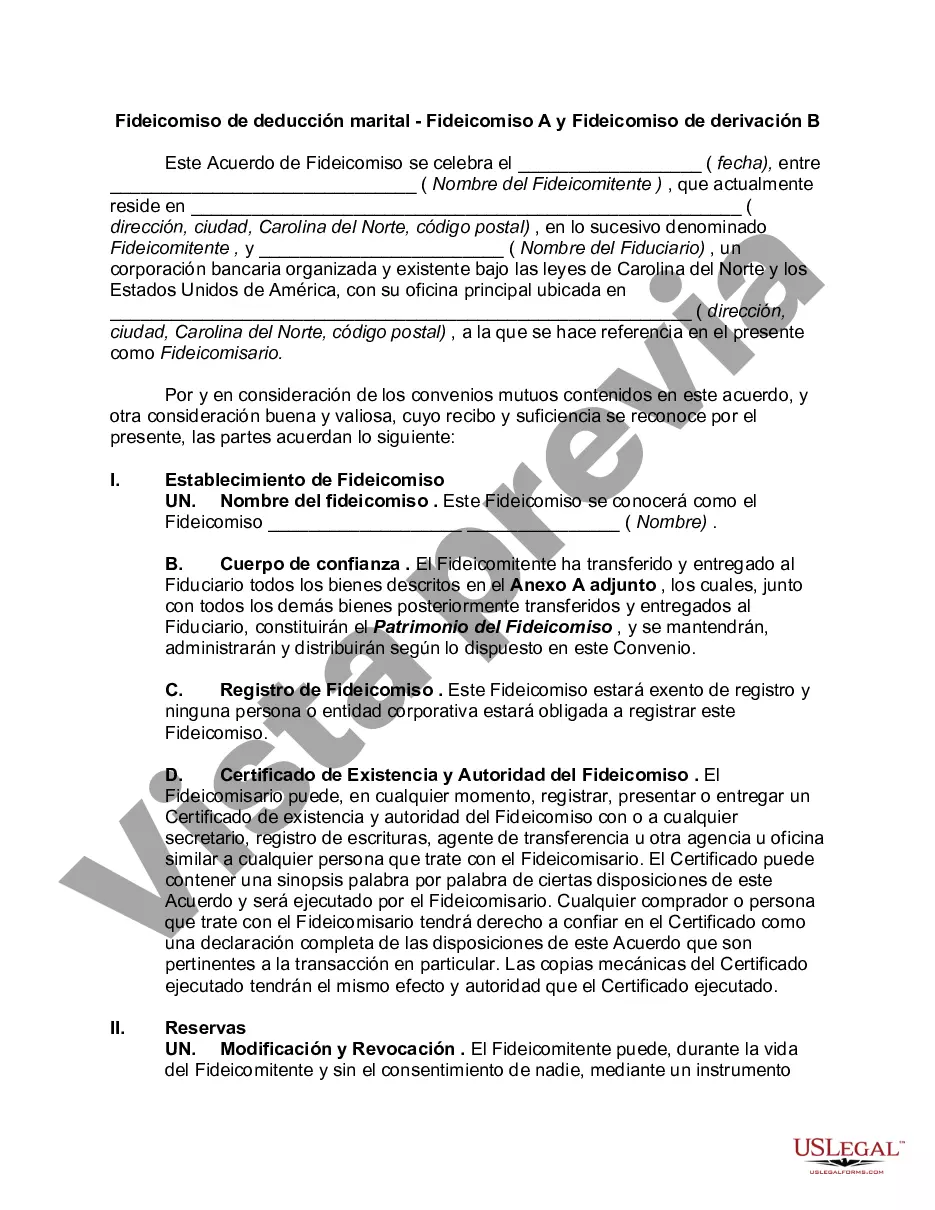

A Cary North Carolina Marital Deduction Trust is a type of trust designed to take advantage of the marital deduction available under federal estate tax laws. This estate planning tool allows married couples to reduce or eliminate estate taxes upon the death of the first spouse. Trust A and Bypass Trust B are two different types of trusts commonly used in conjunction with a Cary North Carolina Marital Deduction Trust. Trust A, also known as the Marital Trust or A Trust, is created to qualify for the marital deduction. It is established to hold assets for the benefit of the surviving spouse, ensuring that they receive income or distributions during their lifetime. The surviving spouse is usually the sole beneficiary of Trust A, with the ability to use and enjoy the trust assets. Bypass Trust B, also known as the Credit Shelter Trust or B Trust, is designed to take full advantage of the federal estate tax exemption. When the first spouse passes away, an amount equal to their estate tax exemption is transferred to Bypass Trust B, instead of passing directly to the surviving spouse. By doing so, the assets in this trust are excluded from the surviving spouse's estate and can be passed on to beneficiaries tax-free upon their death. This strategy maximizes the use of both spouses' estate tax exemptions, effectively reducing the overall estate tax liability. Additionally, there might be other variations of Cary North Carolina Marital Deduction Trusts available depending on the specific needs and objectives of the married couple. Some common variations include Qualified Terminable Interest Property (TIP) Trusts, which provide flexibility in distributing income and principal to the surviving spouse and other selected beneficiaries, and Generation-Skipping Trusts, which allow assets to skip a generation and minimize potential estate tax liabilities for future generations. In conclusion, a Cary North Carolina Marital Deduction Trust is a valuable tool for married couples to minimize estate taxes. Trust A, or the Marital Trust, provides for the surviving spouse's benefit, while Bypass Trust B ensures that both spouses' estate tax exemptions are fully utilized. Other variations of these trusts may also exist to suit specific circumstances and needs. It is advisable to consult with an estate planning attorney or financial advisor familiar with North Carolina's laws to determine the most suitable trust structures for your individual situation.A Cary North Carolina Marital Deduction Trust is a type of trust designed to take advantage of the marital deduction available under federal estate tax laws. This estate planning tool allows married couples to reduce or eliminate estate taxes upon the death of the first spouse. Trust A and Bypass Trust B are two different types of trusts commonly used in conjunction with a Cary North Carolina Marital Deduction Trust. Trust A, also known as the Marital Trust or A Trust, is created to qualify for the marital deduction. It is established to hold assets for the benefit of the surviving spouse, ensuring that they receive income or distributions during their lifetime. The surviving spouse is usually the sole beneficiary of Trust A, with the ability to use and enjoy the trust assets. Bypass Trust B, also known as the Credit Shelter Trust or B Trust, is designed to take full advantage of the federal estate tax exemption. When the first spouse passes away, an amount equal to their estate tax exemption is transferred to Bypass Trust B, instead of passing directly to the surviving spouse. By doing so, the assets in this trust are excluded from the surviving spouse's estate and can be passed on to beneficiaries tax-free upon their death. This strategy maximizes the use of both spouses' estate tax exemptions, effectively reducing the overall estate tax liability. Additionally, there might be other variations of Cary North Carolina Marital Deduction Trusts available depending on the specific needs and objectives of the married couple. Some common variations include Qualified Terminable Interest Property (TIP) Trusts, which provide flexibility in distributing income and principal to the surviving spouse and other selected beneficiaries, and Generation-Skipping Trusts, which allow assets to skip a generation and minimize potential estate tax liabilities for future generations. In conclusion, a Cary North Carolina Marital Deduction Trust is a valuable tool for married couples to minimize estate taxes. Trust A, or the Marital Trust, provides for the surviving spouse's benefit, while Bypass Trust B ensures that both spouses' estate tax exemptions are fully utilized. Other variations of these trusts may also exist to suit specific circumstances and needs. It is advisable to consult with an estate planning attorney or financial advisor familiar with North Carolina's laws to determine the most suitable trust structures for your individual situation.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.