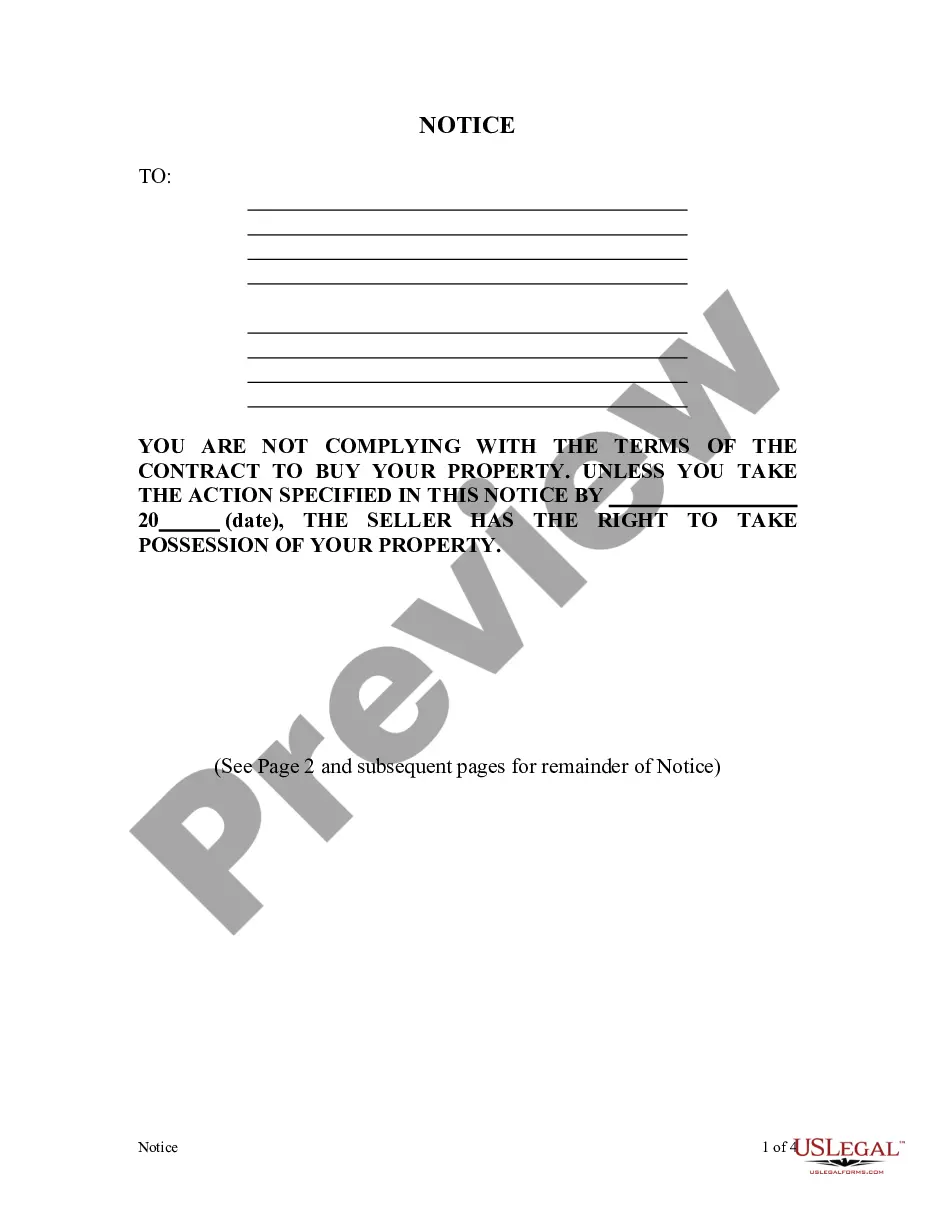

Texas Contract for Deed related forms. This is the Notice of Default form used when the Buyer has paid 40% of the principal of the contract or made a total of 48 or more payments. This form complies with the Texas law, and deal with matters related to Contract for Deed.

Grand Prairie Texas Contract for Deed Notice of Default When 40% of Loan Paid or 48 Payments Made

Category:

State:

Texas

City:

Grand Prairie

Control #:

TX-00470-10

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Texas Contract For Deed Notice Of Default When 40% Of Loan Paid Or 48 Payments Made?

If you have previously used our service, Log In to your account and store the Grand Prairie Texas Contract for Deed Notice of Default When 40% of Loan Settled or 48 Payments Made on your device by selecting the Download button. Ensure your subscription is active. If it isn’t, renew it based on your payment options.

If this is your initial encounter with our service, follow these straightforward steps to obtain your document.

You have continuous access to every document you have acquired: you can find it in your profile within the My documents menu whenever you need to use it again. Utilize the US Legal Forms service to swiftly locate and store any template for your personal or professional requirements!

- Confirm you’ve located an appropriate document. Review the description and utilize the Preview function, if possible, to verify if it fulfills your requirements. If it does not suit you, use the Search tab above to discover the right one.

- Purchase the template. Hit the Buy Now button and select a monthly or yearly subscription plan.

- Create an account and process your payment. Use your credit card information or the PayPal option to finalize the transaction.

- Acquire your Grand Prairie Texas Contract for Deed Notice of Default When 40% of Loan Settled or 48 Payments Made. Choose the file format for your document and save it to your device.

- Finalize your template. Print it or utilize professional online editors to complete it and sign it digitally.

Form popularity

FAQ

?Delivery? of a deed only requires that a grantor release its control over the deed to the grantee while simultaneously intending that the grantee receive the deed. This does not require that the grantor actually physically hand the deed over to the grantee.

Canceling a Door-to-Door Sale To obtain a full refund, you must do this before midnight of the third business day after the sale. Keep a copy of the form. Even if you miss the three-day deadline, your sale may be void if the salesperson failed to make certain disclosures or if certain other conditions are met. See Tex.

Cancelling for any reason: When you sign, the seller must inform you of your right to cancel for any reason within 14 days of signing. If you cancel, the notice must be written, signed, dated, and include the date of cancellation. Send it by certified mail, or hand deliver it to the seller (get receipt for delivery!).

Failure to make timely payments ? The penalty clause in the builder-buyer agreement must define the fine that the buyer will be subjected to in case of failure to disburse the payments in time.

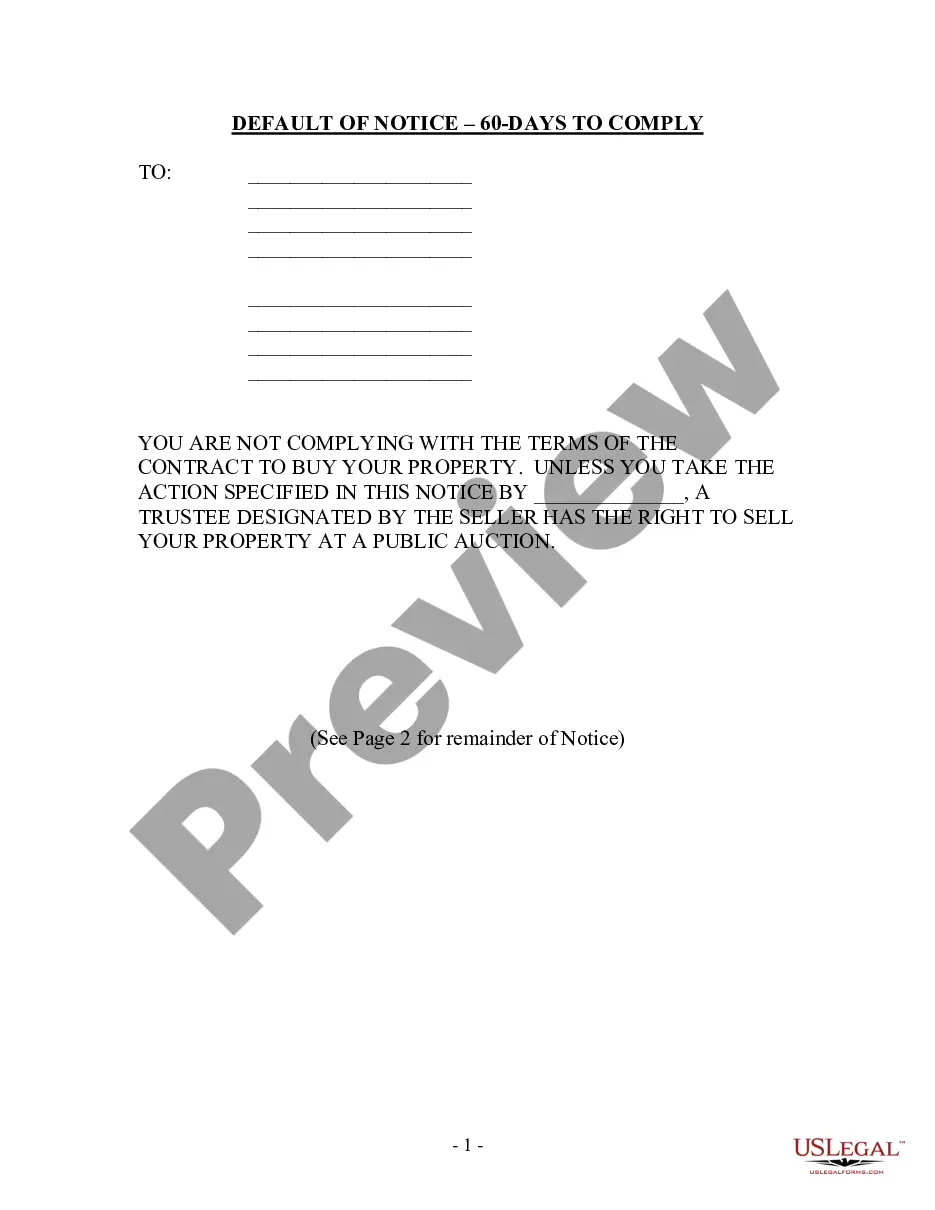

The long-term purchase contract requires the buyer to make monthly or other periodic payments over a long period of time. The contract provides that the seller will deed the property to the buyer after the buyer completes all payments. History of Contract-for-Deed Law in Texas.

A contract for deed is a contract in which the buyer pays for land by making monthly payments for a certain period of years. The buyer does not own or have title to the land until all the payments have been made under the contract.

A person cannot be passively removed from a deed. If the person is still living, you may ask them to remove themselves by signing a quitclaim, which is common after a divorce. The individual who signs and files a quitclaim is asking to have their name removed from the property deed.

You are allowed to back out of the contract for any reason during your option period but you will lose your option fee to the seller. Talk to your real estate agent or a lawyer if you cannot meet the financing terms in the contract.

Prop. Code § 5.077(d)(1); Failure by a Seller to transfer legal, recorded title to the property within 30 days after receiving the Buyer's final payment in violation of Prop. Code § 5.079, gives rise to liquidated damages of $250/day for days 31-90 (following receipt of final payment) and $500/day thereafter.