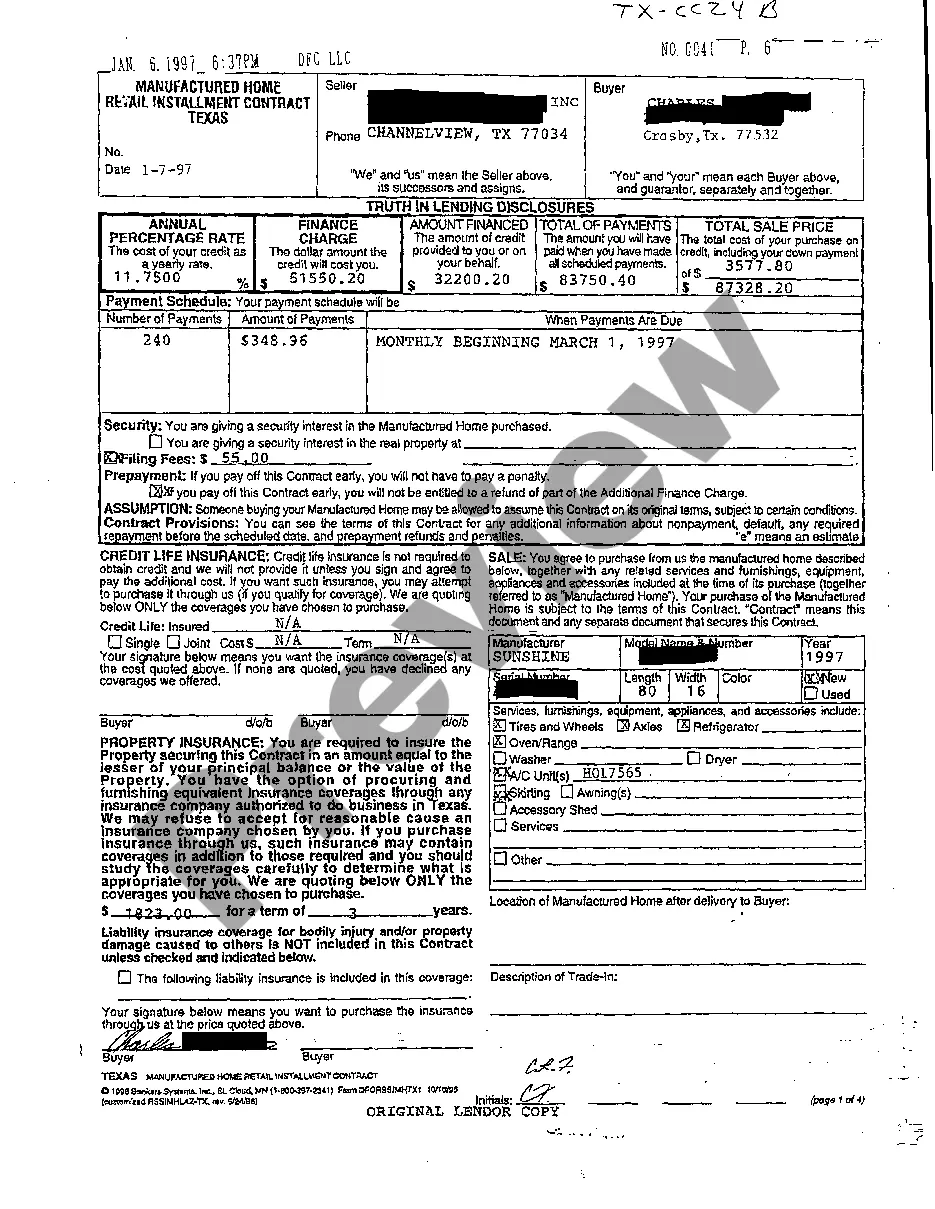

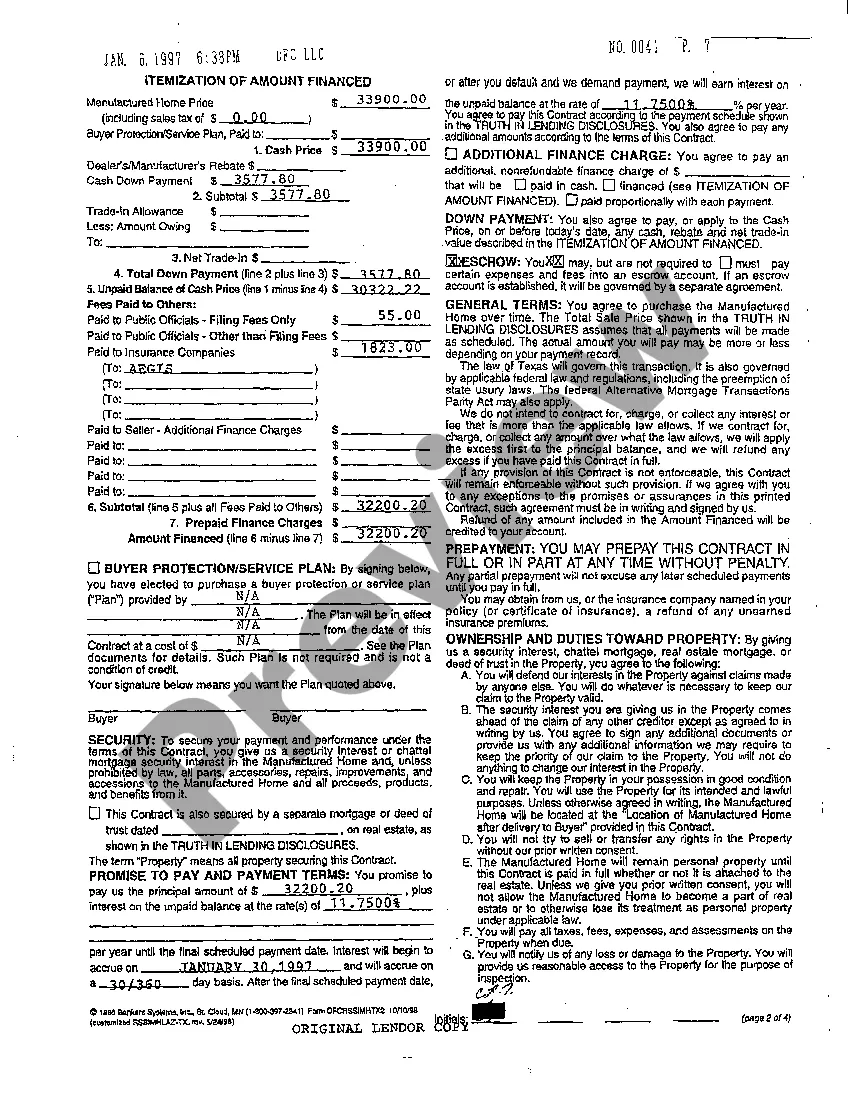

League City, Texas Truth In Lending Disclosures refer to the mandatory information provided by lenders to borrowers regarding the terms and costs associated with their loan agreements. These disclosures ensure transparency and enable borrowers to make informed decisions. Adhering to federal laws, such as the Truth In Lending Act (TILL), these disclosures outline key facets, including interest rates, fees, repayment schedules, and potential penalties. League City, Texas follows the same Truth In Lending Disclosures regulations as other cities across the United States. However, it is important to note that certain municipalities may have additional local ordinances regarding lending practices. The main goal of these disclosures is to protect consumers from deceptive lending practices and provide a fair lending environment. The disclosure statements are comprehensive and typically consist of various documents. Some essential Truth In Lending Disclosures include the: 1. Loan Estimate: This document is provided to borrowers within three business days of applying for a loan. It outlines the loan's important terms and estimated costs, such as interest rates, monthly payments, closing costs, and total loan amount. 2. Closing Disclosure: Borrowers receive this document at least three business days before closing on the loan. It includes the final terms, costs, and other financial details. The purpose of providing this document in advance is to give borrowers ample time to review and compare the disclosed information with the Loan Estimate. 3. Annual Percentage Rate (APR) Disclosure: Lenders must disclose the APR, representing the cost of borrowing over a year, including interest and specific fees. The APR allows borrowers to compare loan offers across different lenders accurately. 4. Total of Payments Disclosure: This document illustrates the total amount a borrower will pay over the life of the loan, including principal, interest, and any associated fees. 5. Payment Schedule: Lenders must provide a detailed payment schedule, outlining the number of payments, their amounts, due dates, and any potential late payment fees or penalties. 6. Prepayment Penalty Statement (if applicable): If there are any penalties associated with prepaying the loan before the agreed-upon timeframe, lenders must disclose them. This allows borrowers to understand the financial implications of paying the loan off early. League City, Texas Truth In Lending Disclosures play a crucial role in protecting borrowers' rights and promoting fair lending practices. These disclosures empower borrowers to make informed decisions while considering mortgage loans, auto loans, personal loans, or other credit transactions. It is vital for lenders to comply with these regulations to ensure transparency and prevent fraudulent practices.

League City Texas Truth In Lending Disclosures

Description

How to fill out League City Texas Truth In Lending Disclosures?

Take advantage of the US Legal Forms and obtain instant access to any form template you need. Our beneficial platform with a large number of documents simplifies the way to find and obtain almost any document sample you need. You can save, fill, and certify the League City Texas Truth In Lending Disclosures in a couple of minutes instead of browsing the web for hours looking for the right template.

Using our library is a great way to increase the safety of your document submissions. Our professional legal professionals on a regular basis review all the documents to make certain that the forms are appropriate for a particular region and compliant with new laws and regulations.

How do you get the League City Texas Truth In Lending Disclosures? If you have a profile, just log in to the account. The Download option will be enabled on all the samples you view. Furthermore, you can get all the earlier saved records in the My Forms menu.

If you haven’t registered an account yet, follow the tips listed below:

- Find the template you need. Make certain that it is the form you were looking for: examine its headline and description, and utilize the Preview function if it is available. Otherwise, make use of the Search field to look for the needed one.

- Start the downloading procedure. Click Buy Now and choose the pricing plan you like. Then, create an account and pay for your order using a credit card or PayPal.

- Export the file. Pick the format to obtain the League City Texas Truth In Lending Disclosures and edit and fill, or sign it according to your requirements.

US Legal Forms is among the most significant and reliable template libraries on the internet. Our company is always ready to help you in virtually any legal process, even if it is just downloading the League City Texas Truth In Lending Disclosures.

Feel free to take full advantage of our service and make your document experience as straightforward as possible!