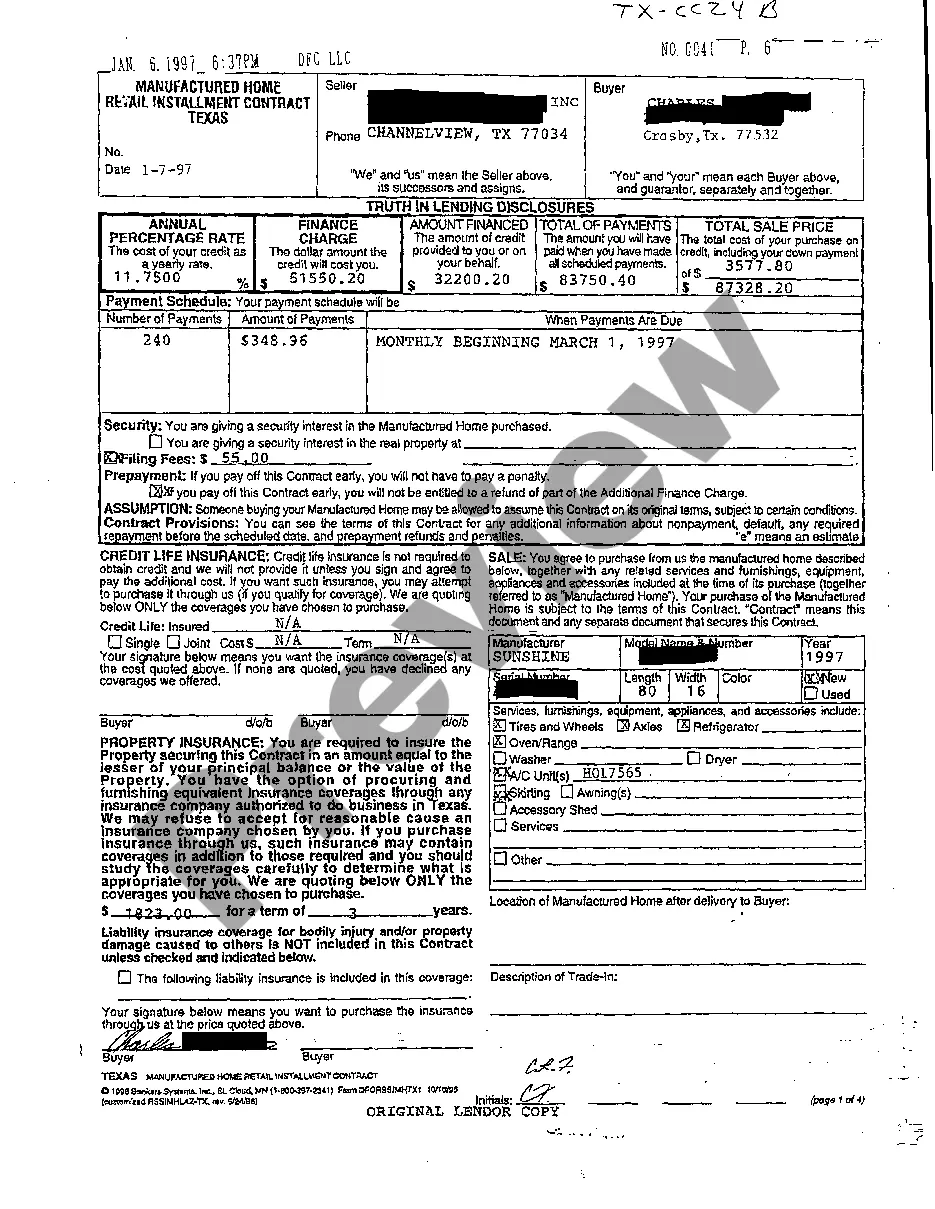

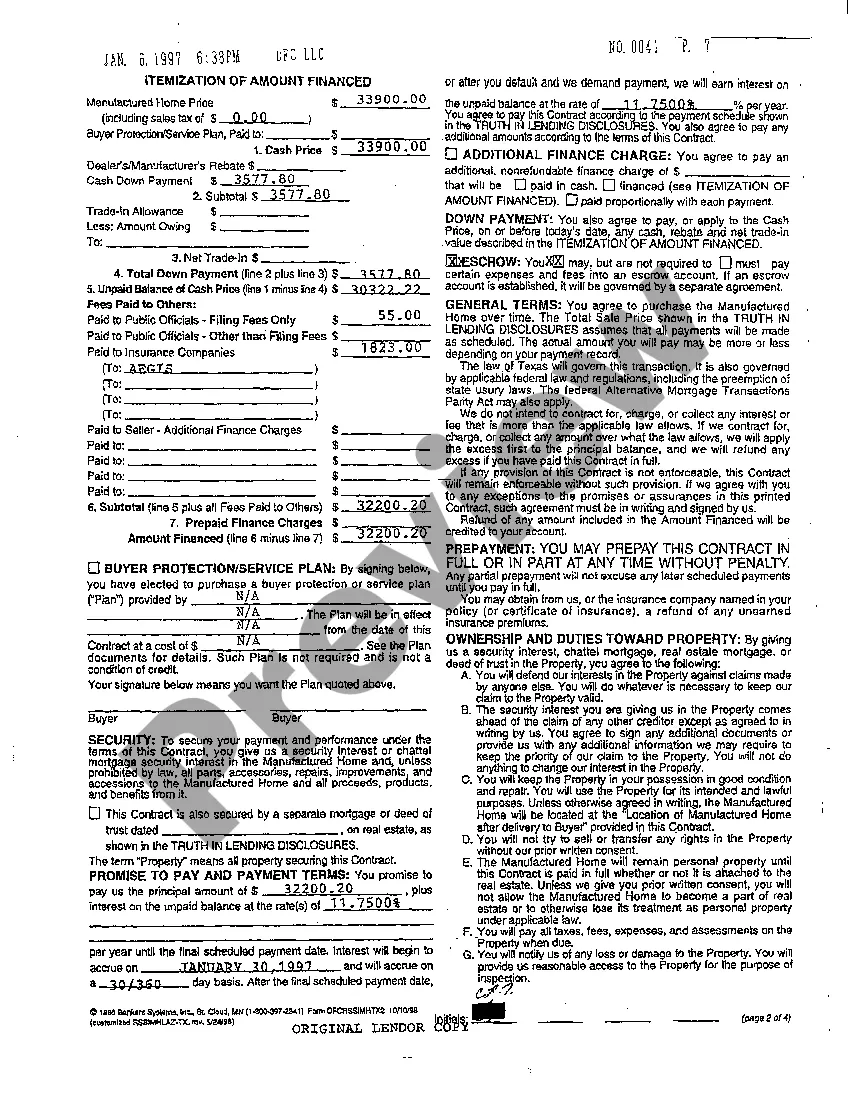

Travis Texas Truth In Lending Disclosures play a crucial role in ensuring transparency and fairness in consumer lending practices. These disclosures are a set of regulations under the Truth in Lending Act (TILL), designed to protect borrowers by providing them with important information about the terms and costs of their loans. The primary purpose of Travis Texas Truth In Lending Disclosures is to enable borrowers to make informed decisions and compare loan offers from different lenders. By providing standardized information, these disclosures empower borrowers to assess the affordability and suitability of the loan they are considering. The main components included in Travis Texas Truth In Lending Disclosures are: 1. Annual Percentage Rate (APR): This percentage reflects the total cost of the loan, including both interest and any additional fees or charges. The APR allows borrowers to compare the overall cost of different loan options accurately. 2. Finance Charge: The finance charge represents the total cost of credit, including interest, fees, and any other charges imposed by the lender. 3. Amount Financed: This refers to the actual amount of money the borrower will receive from the loan after deducting any fees or charges paid directly to the lender. 4. Total Payments: The total payment amount shows the sum of all the payments the borrower will make over the life of the loan, including both principal and interest. 5. Payment Schedule: This section outlines the number and frequency of payments, as well as their due dates. It enables borrowers to plan their finances and understand the repayment structure. 6. Prepayment Penalty: If applicable, this disclosure informs borrowers if there are any penalties associated with paying off their loan early. It is essential for borrowers who may consider refinancing or paying off their loan ahead of schedule. Different types of Travis Texas Truth In Lending Disclosures may include variations specific to certain loan types or circumstances. For example: 1. Mortgage Loan Disclosures: In addition to the standard TILL disclosure requirements, mortgage loans have additional disclosures, such as the Loan Estimate and Closing Disclosure forms, which provide detailed information about the loan terms, closing costs, and other key aspects of the mortgage transaction. 2. Credit Card Disclosures: Credit card issuers are required to provide specific disclosures, including the Annual Percentage Rate, annual fees, grace period (if any), and any other fees or charges associated with the credit card. 3. Student Loan Disclosures: Lenders providing student loans must comply with specific disclosure requirements under the Truth-in-Lending Act provisions for private student loans. These include the APR, finance charges, repayment terms, and any provisions related to deferment or forbearance. In conclusion, Travis Texas Truth In Lending Disclosures are an essential aspect of consumer protection, ensuring borrowers have access to comprehensive information about their loans. By understanding the terms, costs, and repayment structure, borrowers are better equipped to make informed financial decisions.

Travis Texas Truth In Lending Disclosures

State:

Texas

County:

Travis

Control #:

TX-CC-24-03

Format:

PDF

Instant download

This form is available by subscription

Description

A03 Truth In Lending Disclosures

Travis Texas Truth In Lending Disclosures play a crucial role in ensuring transparency and fairness in consumer lending practices. These disclosures are a set of regulations under the Truth in Lending Act (TILL), designed to protect borrowers by providing them with important information about the terms and costs of their loans. The primary purpose of Travis Texas Truth In Lending Disclosures is to enable borrowers to make informed decisions and compare loan offers from different lenders. By providing standardized information, these disclosures empower borrowers to assess the affordability and suitability of the loan they are considering. The main components included in Travis Texas Truth In Lending Disclosures are: 1. Annual Percentage Rate (APR): This percentage reflects the total cost of the loan, including both interest and any additional fees or charges. The APR allows borrowers to compare the overall cost of different loan options accurately. 2. Finance Charge: The finance charge represents the total cost of credit, including interest, fees, and any other charges imposed by the lender. 3. Amount Financed: This refers to the actual amount of money the borrower will receive from the loan after deducting any fees or charges paid directly to the lender. 4. Total Payments: The total payment amount shows the sum of all the payments the borrower will make over the life of the loan, including both principal and interest. 5. Payment Schedule: This section outlines the number and frequency of payments, as well as their due dates. It enables borrowers to plan their finances and understand the repayment structure. 6. Prepayment Penalty: If applicable, this disclosure informs borrowers if there are any penalties associated with paying off their loan early. It is essential for borrowers who may consider refinancing or paying off their loan ahead of schedule. Different types of Travis Texas Truth In Lending Disclosures may include variations specific to certain loan types or circumstances. For example: 1. Mortgage Loan Disclosures: In addition to the standard TILL disclosure requirements, mortgage loans have additional disclosures, such as the Loan Estimate and Closing Disclosure forms, which provide detailed information about the loan terms, closing costs, and other key aspects of the mortgage transaction. 2. Credit Card Disclosures: Credit card issuers are required to provide specific disclosures, including the Annual Percentage Rate, annual fees, grace period (if any), and any other fees or charges associated with the credit card. 3. Student Loan Disclosures: Lenders providing student loans must comply with specific disclosure requirements under the Truth-in-Lending Act provisions for private student loans. These include the APR, finance charges, repayment terms, and any provisions related to deferment or forbearance. In conclusion, Travis Texas Truth In Lending Disclosures are an essential aspect of consumer protection, ensuring borrowers have access to comprehensive information about their loans. By understanding the terms, costs, and repayment structure, borrowers are better equipped to make informed financial decisions.

Free preview

How to fill out Travis Texas Truth In Lending Disclosures?

If you’ve already used our service before, log in to your account and save the Travis Texas Truth In Lending Disclosures on your device by clicking the Download button. Make sure your subscription is valid. If not, renew it in accordance with your payment plan.

If this is your first experience with our service, adhere to these simple steps to obtain your document:

- Ensure you’ve located an appropriate document. Read the description and use the Preview option, if any, to check if it meets your requirements. If it doesn’t fit you, use the Search tab above to find the appropriate one.

- Buy the template. Click the Buy Now button and pick a monthly or annual subscription plan.

- Register an account and make a payment. Utilize your credit card details or the PayPal option to complete the purchase.

- Get your Travis Texas Truth In Lending Disclosures. Pick the file format for your document and save it to your device.

- Fill out your sample. Print it out or take advantage of professional online editors to fill it out and sign it electronically.

You have regular access to each piece of paperwork you have bought: you can find it in your profile within the My Forms menu anytime you need to reuse it again. Take advantage of the US Legal Forms service to easily find and save any template for your personal or professional needs!