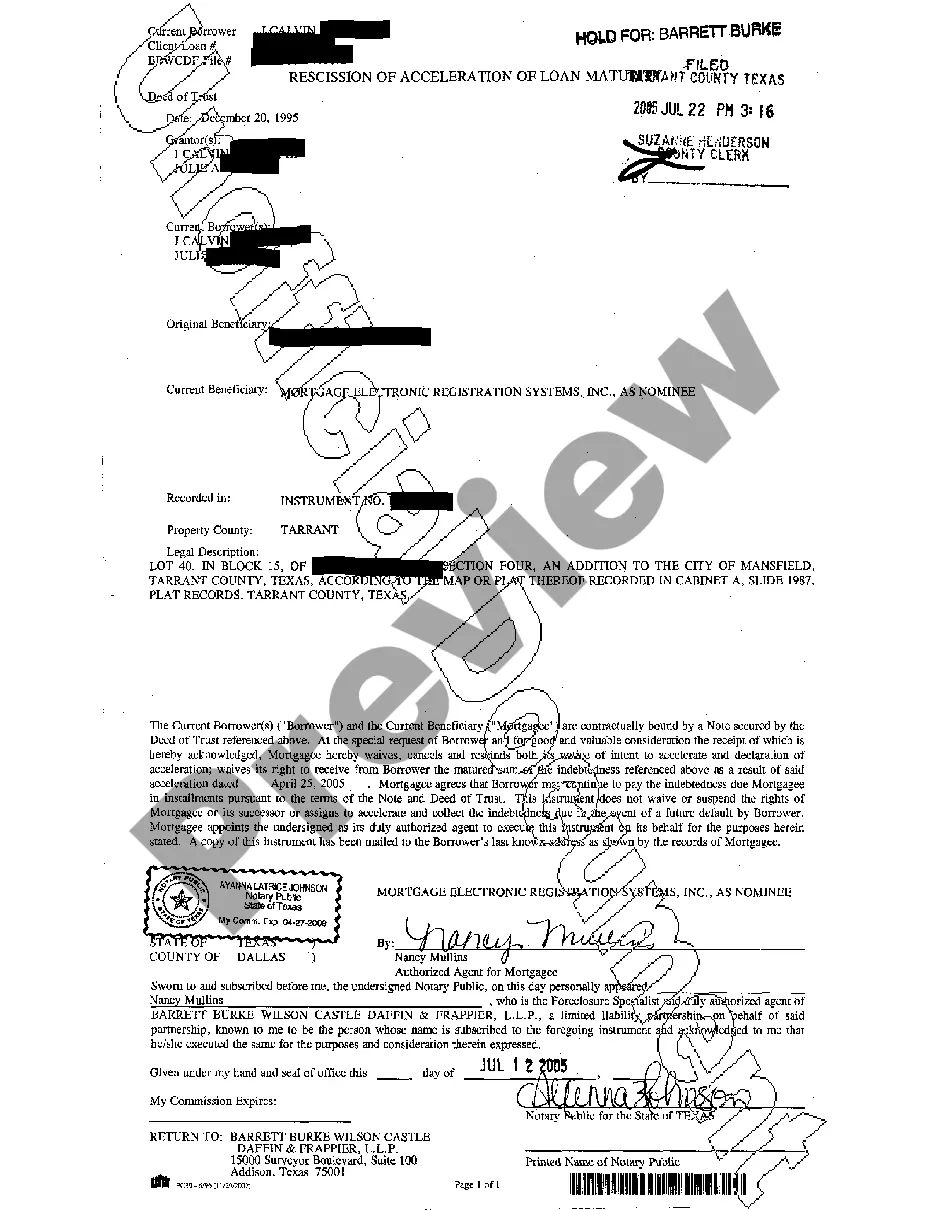

Title: Understanding Brownsville Texas Rescission of Acceleration of Loan: Types and Detailed Description Introduction: In the realm of loan agreements, Brownsville Texas Rescission of Acceleration of Loan refers to a specific legal process where the acceleration clause invoked by the lender is cancelled, thereby restoring the original payment terms and preventing foreclosure. This article aims to provide a comprehensive overview of Brownsville Texas Rescission of Acceleration of Loan, including its types and a detailed description. Types of Brownsville Texas Rescission of Acceleration of Loan: 1. Voluntary Rescission: In some cases, the lender may voluntarily decide to rescind the acceleration clause, allowing the debtor to return to the original payment structure. This type of rescission is typically done due to negotiations, payment arrangements, or the debtor's demonstration of financial stability. 2. Judicial Rescission: If the debtor contests the acceleration of the loan in court, the judge may order a judicial rescission, invalidating the acceleration clause and reverting the loan to its original terms. This type of rescission can occur as a result of a legal dispute or disagreement between the lender and debtor. 3. Non-Judicial Rescission: Rescission of acceleration can also occur outside the court through a non-judicial process. This type involves mediation, arbitration, or negotiations between the lender and debtor, resulting in the reversal of the acceleration clause and the return to the original payment structure. Detailed Description of Brownsville Texas Rescission of Acceleration of Loan: The process of Brownsville Texas Rescission of Acceleration of Loan begins when a borrower fails to meet the mortgage payment obligations, which triggers the acceleration clause. The acceleration clause is a contractual provision often found in loan agreements that allows the lender to accelerate the entire debt, making it due immediately if certain conditions are not met. Upon the invocation of the acceleration clause, the lender usually issues an Acceleration Notice to the borrower, demanding the immediate full payment of the outstanding loan balance. However, in Brownsville, Texas, the debtor maintains the right to rescind the acceleration and revert to the original payment terms if certain conditions are satisfied. To initiate the rescission process, the debtor must communicate their intent to rescind in writing to the lender within a specific timeframe, which is typically outlined in the loan agreement or state laws. The written notice must detail the reasons for the rescission request and provide supporting evidence, such as proof of financial hardship or changed circumstances. Upon receiving the rescission notice, the lender will evaluate the borrower's request and choose to either voluntarily rescind the acceleration clause or proceed with legal action. If both parties mutually agree to rescind, negotiations may occur to establish new payment terms or modify the existing loan agreement. In cases where the lender does not voluntarily rescind, the debtor may choose to contest the acceleration in court through a legal proceeding. Judicial rescission involves presenting evidence and arguments to convince a judge to invalidate the acceleration clause and restore the original payment arrangement. A favorable court ruling would lead to the rescission of acceleration and the reinstatement of the original loan terms. Alternatively, the borrower can pursue a non-judicial rescission by engaging in mediation, arbitration, or negotiation with the lender. These alternative dispute resolution methods aim to facilitate a mutually satisfactory agreement where the acceleration is rescinded, and both parties reach a revised payment plan. Conclusion: In Brownsville, Texas, the process of rescinding the acceleration of a loan provides debtors an opportunity to revert to the original payment terms, avoiding the immediate full repayment demanded by the lender. Whether through voluntary, judicial, or non-judicial means, Brownsville Texas Rescission of Acceleration of Loan protects borrowers from foreclosure and provides opportunities for negotiation and finding suitable alternatives.

Brownsville Texas Rescission of Acceleration of Loan

Description

How to fill out Brownsville Texas Rescission Of Acceleration Of Loan?

Finding verified templates specific to your local laws can be difficult unless you use the US Legal Forms library. It’s an online pool of more than 85,000 legal forms for both personal and professional needs and any real-life situations. All the documents are properly grouped by area of usage and jurisdiction areas, so locating the Brownsville Texas Rescission of Acceleration of Loan gets as quick and easy as ABC.

For everyone already acquainted with our service and has used it before, obtaining the Brownsville Texas Rescission of Acceleration of Loan takes just a couple of clicks. All you need to do is log in to your account, opt for the document, and click Download to save it on your device. The process will take just a couple of additional steps to complete for new users.

Follow the guidelines below to get started with the most extensive online form library:

- Look at the Preview mode and form description. Make certain you’ve picked the right one that meets your requirements and fully corresponds to your local jurisdiction requirements.

- Search for another template, if needed. Once you find any inconsistency, use the Search tab above to get the right one. If it suits you, move to the next step.

- Purchase the document. Click on the Buy Now button and choose the subscription plan you prefer. You should register an account to get access to the library’s resources.

- Make your purchase. Provide your credit card details or use your PayPal account to pay for the service.

- Download the Brownsville Texas Rescission of Acceleration of Loan. Save the template on your device to proceed with its completion and get access to it in the My Forms menu of your profile whenever you need it again.

Keeping paperwork neat and compliant with the law requirements has significant importance. Benefit from the US Legal Forms library to always have essential document templates for any needs just at your hand!