The admission of a new partner results in the legal dissolution of the existing partnership and the beginning of a new one. From an economic standpoint, however, the admission of a new partner (or partners) may be of minor significance in the continuity of the business. For example, in large public accounting or law firms, partners are admitted annually without any change in operating policies. To recognize the economic effects, it is necessary only to open a capital account for each new partner. In the entries illustrated in this appendix, we assume that the accounting records of the predecessor firm will continue to be used by the new partnership. A new partner may be admitted either by (1) purchasing the interest of one or more existing partners or (2) investing assets in the partnership, as shown in Illustration 12A-1. The former affects only the capital accounts of the partners who are parties to the transaction. The latter increases both net assets and total capital of the partnership.

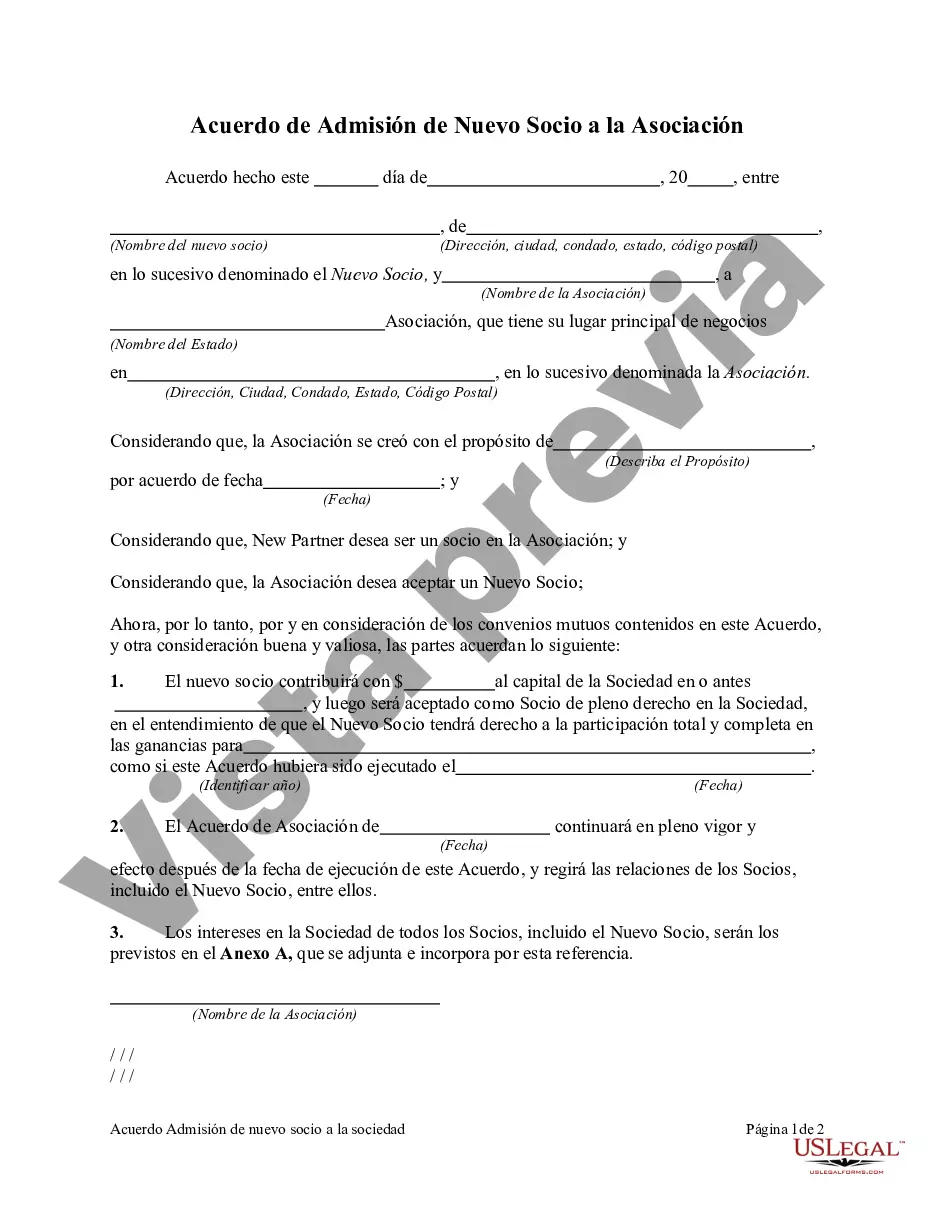

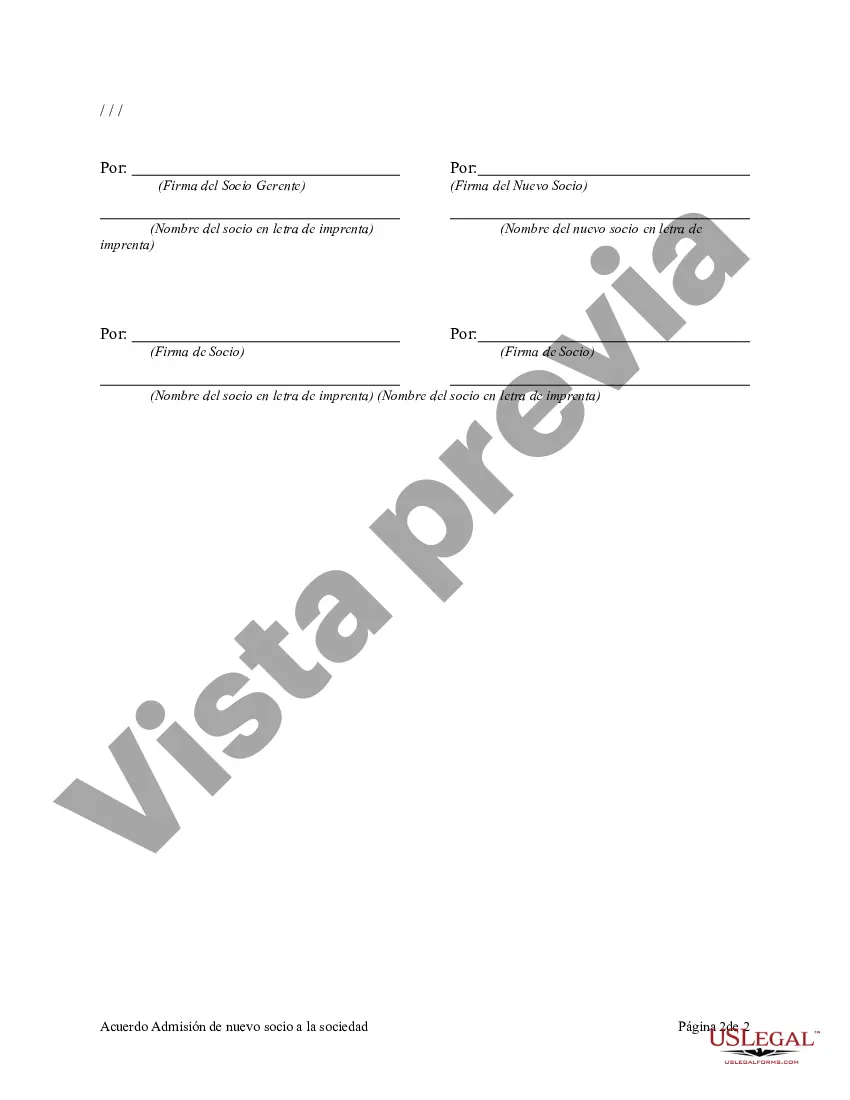

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Orange California Acuerdo de Admisión de Nuevo Socio a la Asociación - Agreement Admitting New Partner to Partnership

Description

How to fill out Orange California Acuerdo De Admisión De Nuevo Socio A La Asociación?

Do you need to quickly create a legally-binding Orange Agreement Admitting New Partner to Partnership or maybe any other document to manage your own or business affairs? You can select one of the two options: hire a legal advisor to write a legal paper for you or create it entirely on your own. Luckily, there's another solution - US Legal Forms. It will help you receive professionally written legal papers without having to pay unreasonable fees for legal services.

US Legal Forms offers a huge catalog of over 85,000 state-specific document templates, including Orange Agreement Admitting New Partner to Partnership and form packages. We offer templates for an array of life circumstances: from divorce paperwork to real estate documents. We've been out there for more than 25 years and gained a rock-solid reputation among our customers. Here's how you can become one of them and obtain the necessary template without extra troubles.

- To start with, carefully verify if the Orange Agreement Admitting New Partner to Partnership is adapted to your state's or county's laws.

- If the form includes a desciption, make sure to check what it's suitable for.

- Start the searching process again if the form isn’t what you were looking for by using the search bar in the header.

- Select the plan that is best suited for your needs and proceed to the payment.

- Select the format you would like to get your form in and download it.

- Print it out, complete it, and sign on the dotted line.

If you've already set up an account, you can easily log in to it, locate the Orange Agreement Admitting New Partner to Partnership template, and download it. To re-download the form, simply head to the My Forms tab.

It's easy to find and download legal forms if you use our catalog. In addition, the paperwork we provide are updated by law professionals, which gives you greater confidence when dealing with legal affairs. Try US Legal Forms now and see for yourself!