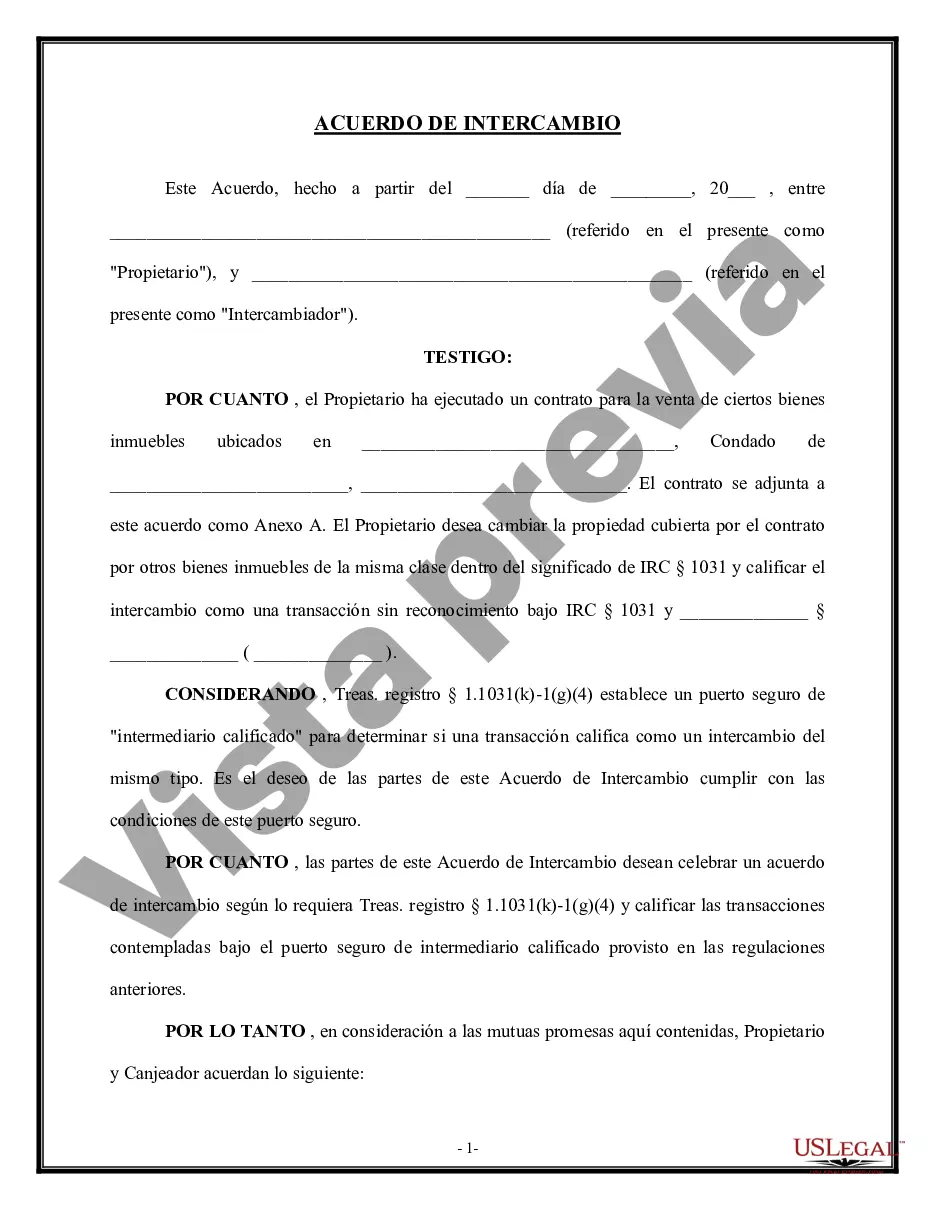

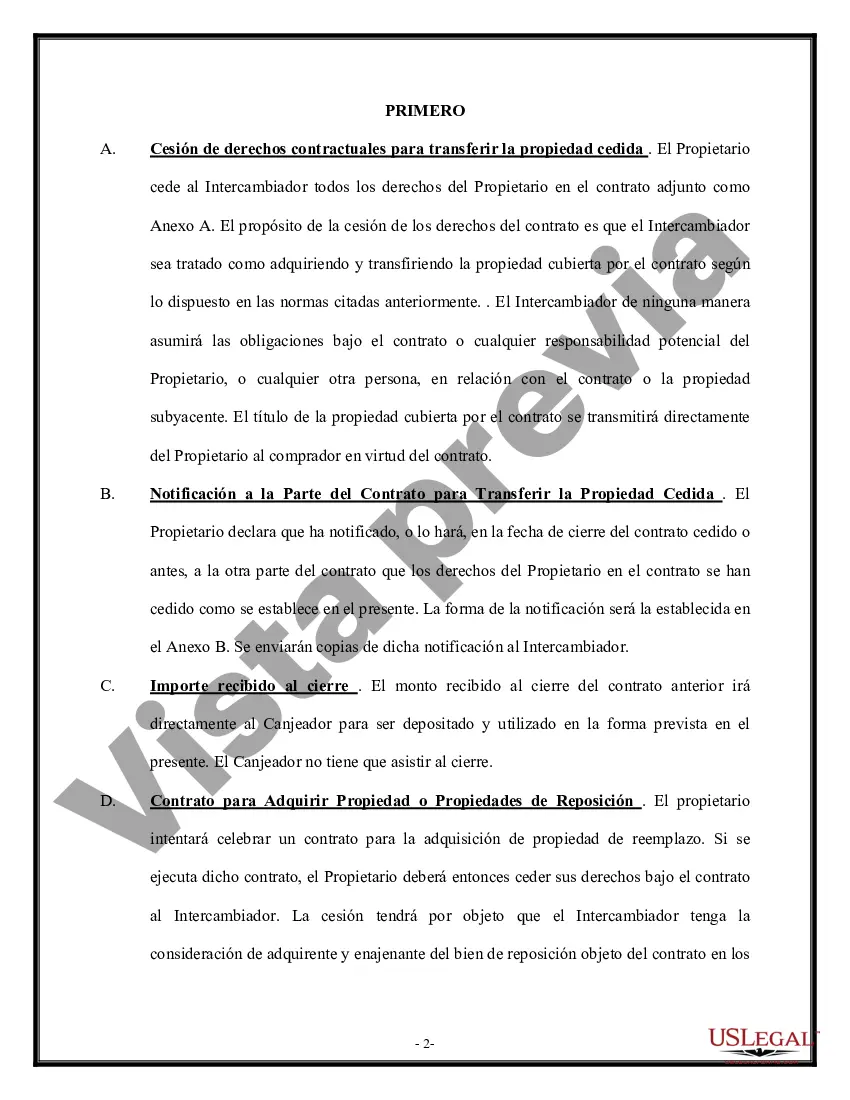

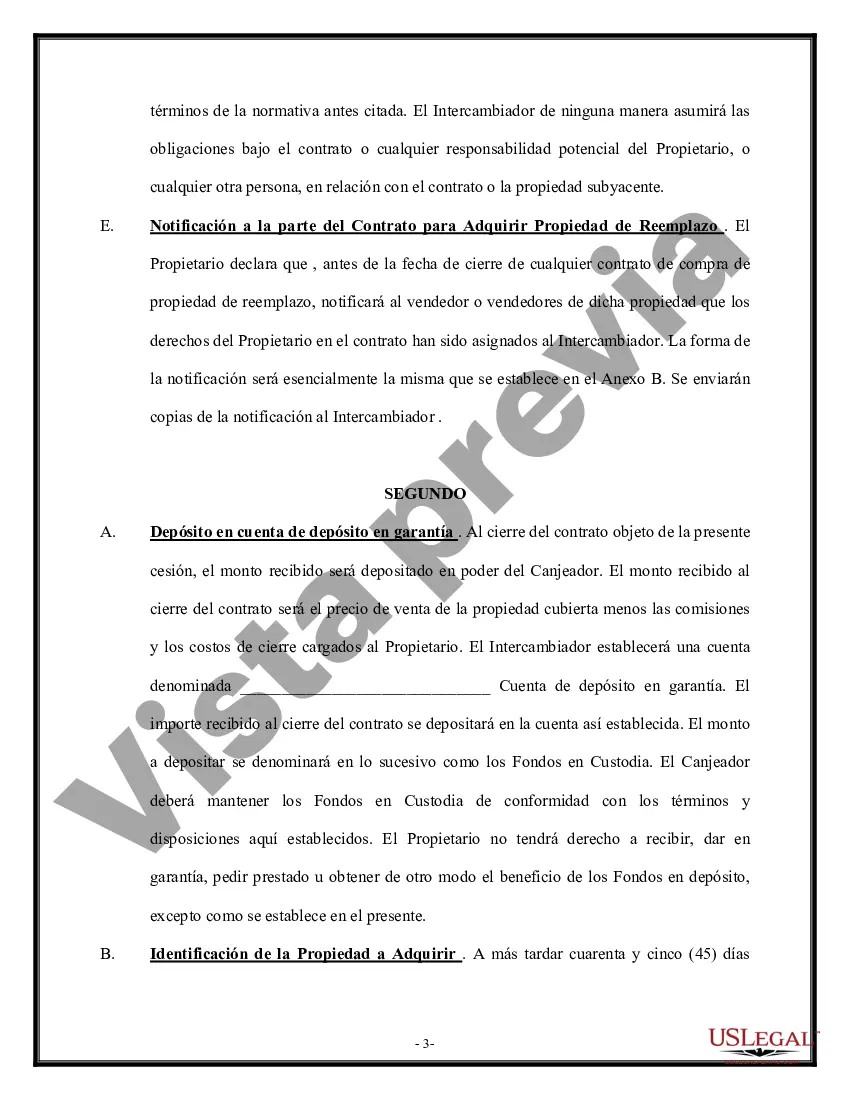

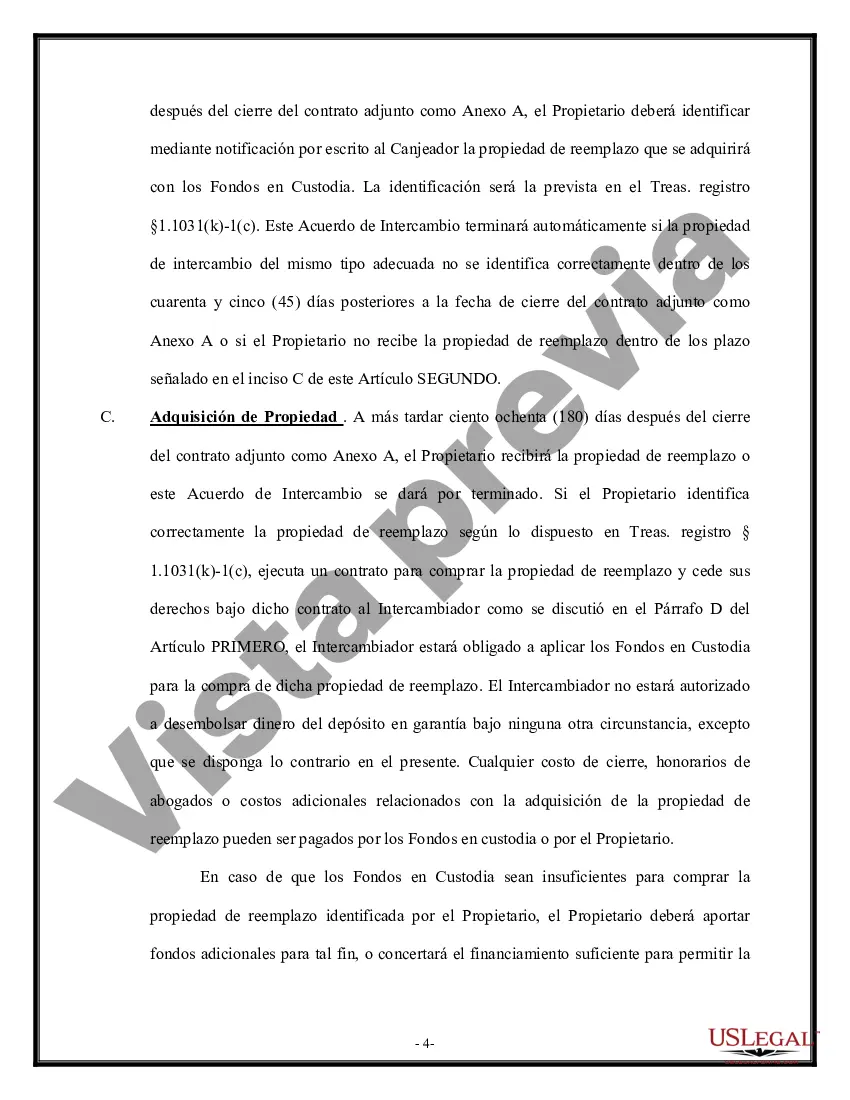

King Washington Tax Free Exchange Agreement Section 1031 is an important provision in the tax code that provides individuals and businesses with a tax-deferred exchange opportunity for certain types of properties. By taking advantage of this provision, taxpayers can defer their capital gains taxes on the sale of investment or business properties, as long as the proceeds are reinvested in a similar property within certain timeframes. This exchange agreement, commonly known as a 1031 exchange, allows taxpayers to sell a property, known as the "relinquished property," and acquire a different property, known as the "replacement property," while deferring the payment of capital gains taxes on the sale. The ultimate goal is to allow taxpayers to reinvest their capital gains into other investment or business properties, thus stimulating economic growth and encouraging investment. The King Washington Tax Free Exchange Agreement Section 1031 applies to a broad range of properties, including real estate, both residential and commercial, as well as certain types of personal property used for investment or business purposes. However, this provision does not cover properties held for personal use, such as primary residences or vacation homes. It's important to note that there are specific criteria and regulations that need to be followed to qualify for a tax-free exchange under Section 1031. The relinquished property and the replacement property must be of a "like-kind" nature, meaning they must be of the same nature or character, such as exchanging one commercial building for another or swapping one rental property for another. Additionally, there are strict timelines that must be adhered to during the exchange process. There are different types of 1031 exchanges within the King Washington Tax Free Exchange Agreement Section 1031. These include: 1. Simultaneous Exchange: This is the most straightforward type of exchange in which the sale of the relinquished property and the acquisition of the replacement property occur simultaneously. 2. Delayed Exchange: This is the most common type of 1031 exchange, where the taxpayer sells the relinquished property first and then has a specific timeframe to identify and acquire the replacement property. This exchange allows for a more flexible timeline but requires careful planning and adherence to IRS rules. 3. Reverse Exchange: In a reverse exchange, the taxpayer acquires the replacement property first and later sells the relinquished property. This type of exchange is more complex and requires an exchange facilitator to work within the IRS guidelines. 4. Construction or Improvement Exchange: Also known as a build-to-suit exchange, this type allows taxpayers to use exchange funds to improve or construct a replacement property. This exchange requires meticulous planning and adherence to IRS regulations. In conclusion, the King Washington Tax Free Exchange Agreement Section 1031 offers taxpayers a valuable tax deferral opportunity when exchanging investment or business properties. It encourages investment, fosters economic growth, and provides a mechanism for individuals and businesses to optimize their real estate portfolios. Proper guidance from tax professionals is essential to ensure compliance with IRS rules and maximize the benefits of a 1031 exchange.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.King Washington Acuerdo de Intercambio Libre de Impuestos Sección 1031 - Tax Free Exchange Agreement Section 1031

Description

How to fill out King Washington Acuerdo De Intercambio Libre De Impuestos Sección 1031?

Whether you intend to start your company, enter into an agreement, apply for your ID update, or resolve family-related legal concerns, you must prepare certain documentation corresponding to your local laws and regulations. Finding the correct papers may take a lot of time and effort unless you use the US Legal Forms library.

The service provides users with more than 85,000 expertly drafted and checked legal documents for any personal or business occurrence. All files are collected by state and area of use, so opting for a copy like King Tax Free Exchange Agreement Section 1031 is fast and straightforward.

The US Legal Forms website users only need to log in to their account and click the Download key next to the required form. If you are new to the service, it will take you a couple of additional steps to obtain the King Tax Free Exchange Agreement Section 1031. Adhere to the instructions below:

- Make sure the sample meets your individual needs and state law requirements.

- Read the form description and check the Preview if there’s one on the page.

- Make use of the search tab providing your state above to find another template.

- Click Buy Now to get the sample once you find the proper one.

- Choose the subscription plan that suits you most to continue.

- Log in to your account and pay the service with a credit card or PayPal.

- Download the King Tax Free Exchange Agreement Section 1031 in the file format you prefer.

- Print the copy or fill it out and sign it electronically via an online editor to save time.

Documents provided by our website are reusable. Having an active subscription, you can access all of your earlier purchased paperwork at any time in the My Forms tab of your profile. Stop wasting time on a endless search for up-to-date official documentation. Join the US Legal Forms platform and keep your paperwork in order with the most comprehensive online form library!