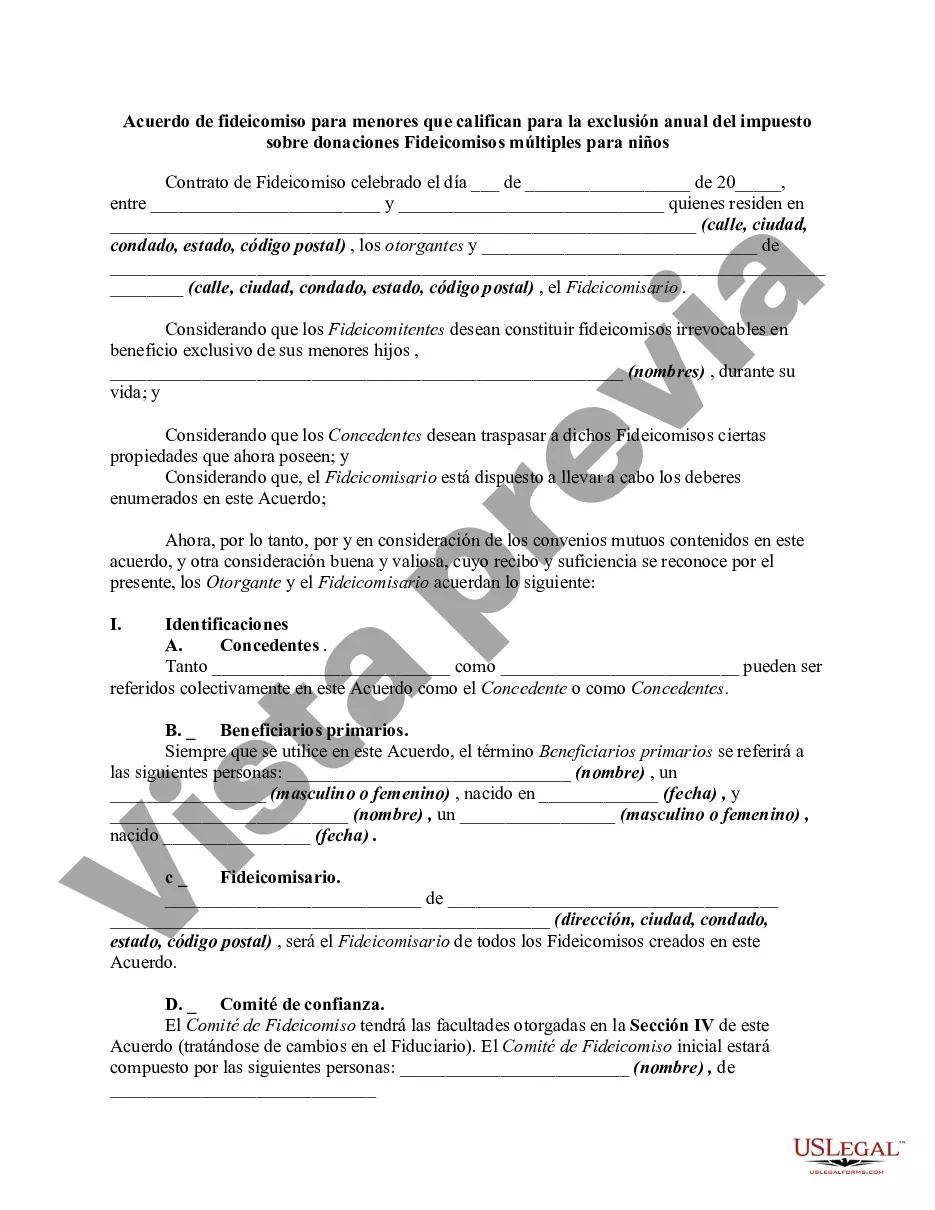

This form set up what is known as present interest trusts, with the intention of meeting the requirements of Section 2503(c) of the Internal Revenue Code.

The San Diego California Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children is a legal document designed to establish a trust for minors in order to take advantage of the annual gift tax exclusion. This type of trust provides a way for individuals to transfer assets to their children while minimizing gift tax liabilities. Keywords: San Diego California, trust agreement, minors, qualifying, annual gift tax exclusion, multiple trusts, children. There are several types of San Diego California Trust Agreements for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children. Some of these include: 1. Unified Credit Trust: This trust is established with the purpose of utilizing the annual gift tax exclusion for each child. By creating separate trusts for each child, parents or grandparents can contribute up to the annual exclusion amount without incurring gift taxes. 2. Crummy Trust: Named after the Crummy v. Commissioner case, this trust allows for the creation of multiple gift trusts for each child. It utilizes the "Crummy" withdrawal power, which provides the beneficiaries with the ability to withdraw the gifted amounts for a certain period of time, usually 30 days. This withdrawal power makes the gifts qualify for the annual gift tax exclusion. 3. Section 2503© Trust: This trust is established under the provisions of Section 2503(c) of the Internal Revenue Code. It allows for the creation of multiple trusts for each child, maintaining the gift tax exclusion. This type of trust is often used to transfer assets to children while avoiding the generation-skipping transfer tax. 4. 2503(b) Trust: Similar to the Section 2503© Trust, this trust is established under Section 2503(b) of the Internal Revenue Code. It enables the annual exclusion for gifts to minors, while also ensuring that the gifted assets are included in the taxable estate of the granter. 5. Life Insurance Trust: This type of trust is funded with life insurance policies and is often used to provide for the financial needs of the beneficiaries upon the granter's death. By creating multiple life insurance trusts for each child, the gift tax exclusion can be maximized. Overall, the San Diego California Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children provides individuals with various options for transferring assets to their children while minimizing gift tax implications. These trusts allow for the creation of separate accounts for each child, ensuring that the annual gift tax exclusion can be maximized.The San Diego California Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children is a legal document designed to establish a trust for minors in order to take advantage of the annual gift tax exclusion. This type of trust provides a way for individuals to transfer assets to their children while minimizing gift tax liabilities. Keywords: San Diego California, trust agreement, minors, qualifying, annual gift tax exclusion, multiple trusts, children. There are several types of San Diego California Trust Agreements for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children. Some of these include: 1. Unified Credit Trust: This trust is established with the purpose of utilizing the annual gift tax exclusion for each child. By creating separate trusts for each child, parents or grandparents can contribute up to the annual exclusion amount without incurring gift taxes. 2. Crummy Trust: Named after the Crummy v. Commissioner case, this trust allows for the creation of multiple gift trusts for each child. It utilizes the "Crummy" withdrawal power, which provides the beneficiaries with the ability to withdraw the gifted amounts for a certain period of time, usually 30 days. This withdrawal power makes the gifts qualify for the annual gift tax exclusion. 3. Section 2503© Trust: This trust is established under the provisions of Section 2503(c) of the Internal Revenue Code. It allows for the creation of multiple trusts for each child, maintaining the gift tax exclusion. This type of trust is often used to transfer assets to children while avoiding the generation-skipping transfer tax. 4. 2503(b) Trust: Similar to the Section 2503© Trust, this trust is established under Section 2503(b) of the Internal Revenue Code. It enables the annual exclusion for gifts to minors, while also ensuring that the gifted assets are included in the taxable estate of the granter. 5. Life Insurance Trust: This type of trust is funded with life insurance policies and is often used to provide for the financial needs of the beneficiaries upon the granter's death. By creating multiple life insurance trusts for each child, the gift tax exclusion can be maximized. Overall, the San Diego California Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion — Multiple Trusts for Children provides individuals with various options for transferring assets to their children while minimizing gift tax implications. These trusts allow for the creation of separate accounts for each child, ensuring that the annual gift tax exclusion can be maximized.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.