A guaranty is a contract under which one person agrees to pay a debt or perform a duty if the other person who is bound to pay the debt or perform the duty fails to do so. A guaranty of the payment of a debt is different from a guaranty of the collection of the debt. A guaranty of payment is absolute while a guaranty of collection is conditional.

Fairfax Virginia Guaranty of Collection of Promissory Note is a legal document used to ensure collection of outstanding debts owed by a borrower. It provides a guarantee to the lender that the guarantor will undertake collection efforts in the event that the borrower defaults on their payment obligations. The purpose of the Fairfax Virginia Guaranty of Collection of Promissory Note is to provide additional security to the lender by creating a secondary source for debt recovery. By signing this guaranty, the guarantor becomes legally responsible for the collection of any unpaid amounts under the promissory note. There are different types of Fairfax Virginia Guaranty of Collection of Promissory Note that can be used depending on the specific situation: 1. Individual Guaranty of Collection of Promissory Note: This type of guaranty is executed by an individual who agrees to be personally liable for the collection of a promissory note. 2. Corporate Guaranty of Collection of Promissory Note: In this case, a corporation assumes the responsibility of collecting the debt on behalf of the lender. The corporation guarantees repayment of the outstanding amounts under the promissory note. 3. Limited Guaranty of Collection of Promissory Note: This type of guaranty limits the liability of the guarantor to a specific amount or for a specified period. Key elements included in the Fairfax Virginia Guaranty of Collection of Promissory Note are: — Comprehensive identification of the parties involved, including the lender, borrower, and guarantor. — The specific terms and conditions under which the guaranty becomes effective, such as the amount of debt, interest rate, and repayment terms. — The guarantor's responsibilities, outlining their obligation to pursue collection efforts in case of borrower default. — The consequences of borrower default, stating the possible remedies available to the lender and outlining the guarantor's liability. — Indemnification provisions that protect the lender from losses incurred in pursuing collection efforts. — Governing laws and jurisdiction, specifying that the Fairfax Virginia laws apply and any disputes will be resolved in the appropriate state court. In summary, the Fairfax Virginia Guaranty of Collection of Promissory Note is an important legal document that provides additional security to lenders for the collection of outstanding debts. Different types of guaranty exist, such as individual, corporate, and limited guaranties, allowing flexibility to suit various circumstances. It is crucial to consult with a legal professional when creating or executing this document to ensure its compliance with applicable laws and to safeguard the interests of all parties involved.Fairfax Virginia Guaranty of Collection of Promissory Note is a legal document used to ensure collection of outstanding debts owed by a borrower. It provides a guarantee to the lender that the guarantor will undertake collection efforts in the event that the borrower defaults on their payment obligations. The purpose of the Fairfax Virginia Guaranty of Collection of Promissory Note is to provide additional security to the lender by creating a secondary source for debt recovery. By signing this guaranty, the guarantor becomes legally responsible for the collection of any unpaid amounts under the promissory note. There are different types of Fairfax Virginia Guaranty of Collection of Promissory Note that can be used depending on the specific situation: 1. Individual Guaranty of Collection of Promissory Note: This type of guaranty is executed by an individual who agrees to be personally liable for the collection of a promissory note. 2. Corporate Guaranty of Collection of Promissory Note: In this case, a corporation assumes the responsibility of collecting the debt on behalf of the lender. The corporation guarantees repayment of the outstanding amounts under the promissory note. 3. Limited Guaranty of Collection of Promissory Note: This type of guaranty limits the liability of the guarantor to a specific amount or for a specified period. Key elements included in the Fairfax Virginia Guaranty of Collection of Promissory Note are: — Comprehensive identification of the parties involved, including the lender, borrower, and guarantor. — The specific terms and conditions under which the guaranty becomes effective, such as the amount of debt, interest rate, and repayment terms. — The guarantor's responsibilities, outlining their obligation to pursue collection efforts in case of borrower default. — The consequences of borrower default, stating the possible remedies available to the lender and outlining the guarantor's liability. — Indemnification provisions that protect the lender from losses incurred in pursuing collection efforts. — Governing laws and jurisdiction, specifying that the Fairfax Virginia laws apply and any disputes will be resolved in the appropriate state court. In summary, the Fairfax Virginia Guaranty of Collection of Promissory Note is an important legal document that provides additional security to lenders for the collection of outstanding debts. Different types of guaranty exist, such as individual, corporate, and limited guaranties, allowing flexibility to suit various circumstances. It is crucial to consult with a legal professional when creating or executing this document to ensure its compliance with applicable laws and to safeguard the interests of all parties involved.

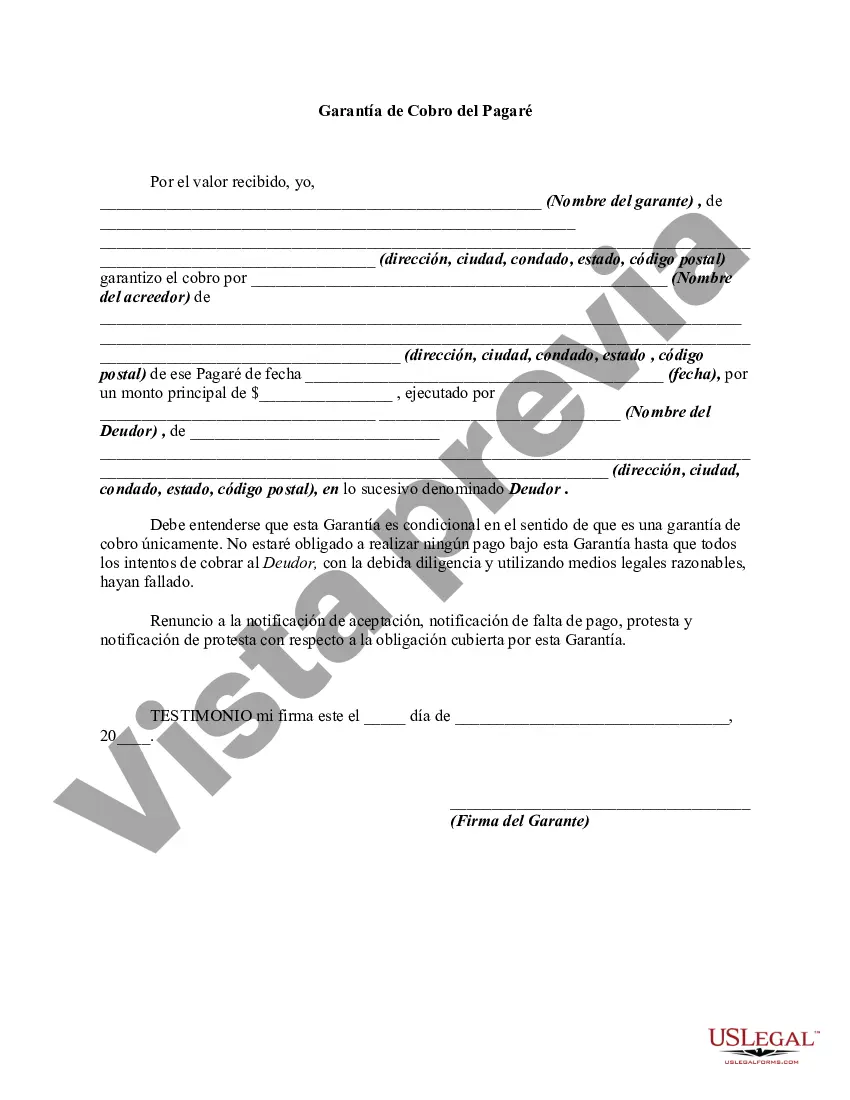

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.