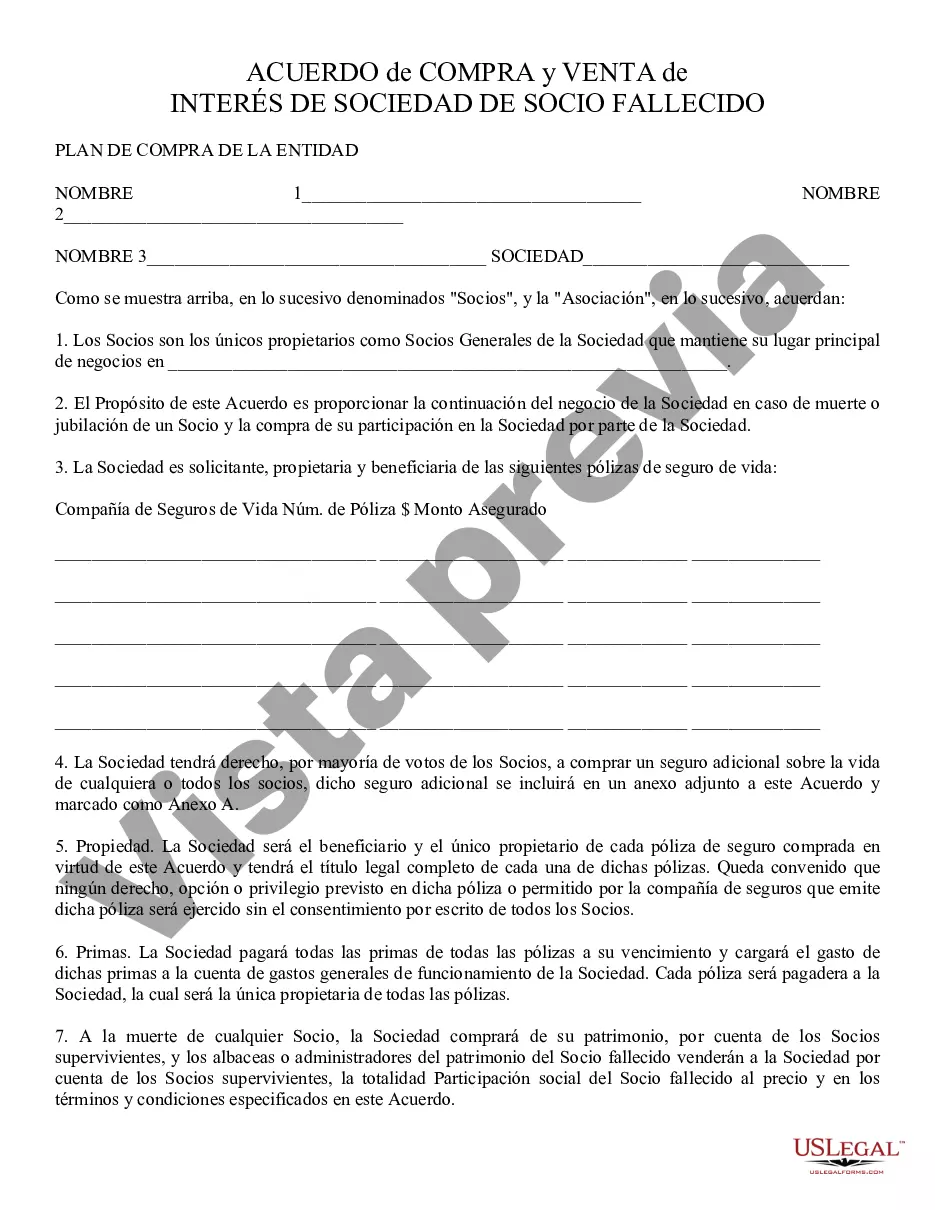

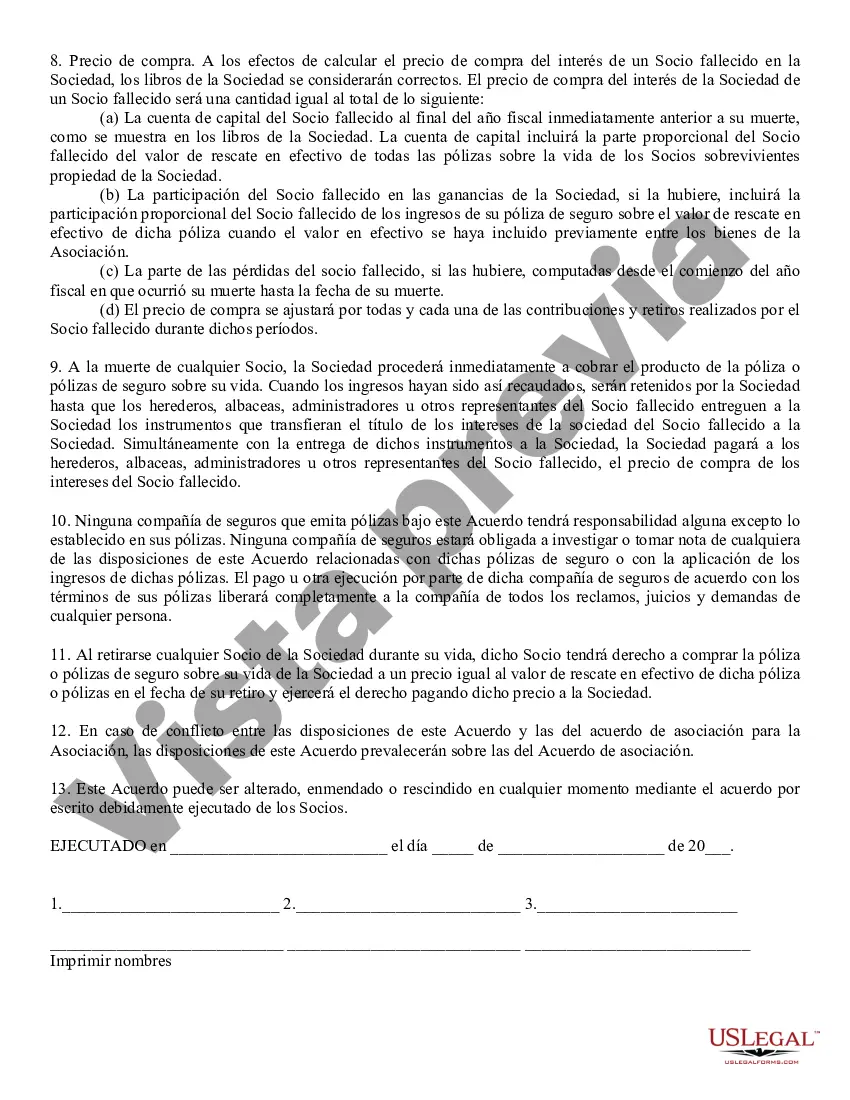

Fairfax Virginia Sale of Deceased Partner's Interest refers to the legal process involved in selling the ownership stake or share of a deceased individual in a business or partnership located in Fairfax, Virginia. This process is typically initiated to settle the affairs of the deceased partner and ensure a smooth transition of ownership within the business. When a partner in a business based in Fairfax, Virginia passes away, their interest in the company becomes part of their estate. Selling the deceased partner's interest is often necessary to provide necessary funds for the estate, distribute assets to beneficiaries, or facilitate the continuation of the business. There are several types of Fairfax Virginia Sale of Deceased Partner's Interest, including: 1. Outright Sale: In this scenario, the deceased partner's interest is sold to an external buyer or an existing partner in the business. The proceeds generated from the sale are then distributed among the estate or beneficiaries as per the deceased partner's will or applicable laws of inheritance in Virginia. 2. Buy-Sell Agreement: If the business has an existing buy-sell agreement in place, it may specify how the deceased partner's interest should be sold. Typically, buy-sell agreements outline the procedure for valuing the interest and provide an option for the remaining partners or the business itself to purchase the deceased partner's interest. 3. Auction or Public Sale: In some cases, when there is no buyer readily available within the business or the deceased partner's network, the interest may be sold through a public auction. This process involves advertising the sale publicly and accepting bids from interested parties, ultimately selecting the highest bidder. 4. Offer to Other Partners: If the business has multiple partners, they may have the right of first refusal to purchase the deceased partner's interest. If any of the remaining partners are interested, they can offer to buy the interest at a fair market value determined by professional appraisers. 5. Liquidation: If other alternatives fail, the business may resort to liquidating its assets and winding up operations. In this case, the business's assets, including the deceased partner's interest, will be sold off, and the proceeds will be distributed to creditors and any entitled beneficiaries. Navigating the Fairfax Virginia Sale of Deceased Partner's Interest can be a complex process involving legal consultations, business valuation, negotiations, and compliance with Virginia laws and regulations. It is advisable to seek assistance from an experienced attorney or business advisor knowledgeable in estate planning and business law to ensure a smooth and fair transfer of the deceased partner's interest in accordance with the partner's wishes and legal requirements in Fairfax, Virginia.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Fairfax Virginia Venta de Interés de Socio Fallecido - Sale of Deceased Partner's Interest

Description

How to fill out Fairfax Virginia Venta De Interés De Socio Fallecido?

How much time does it normally take you to draft a legal document? Considering that every state has its laws and regulations for every life scenario, finding a Fairfax Sale of Deceased Partner's Interest suiting all local requirements can be stressful, and ordering it from a professional lawyer is often costly. Numerous web services offer the most popular state-specific documents for download, but using the US Legal Forms library is most beneficial.

US Legal Forms is the most comprehensive web collection of templates, gathered by states and areas of use. Aside from the Fairfax Sale of Deceased Partner's Interest, here you can get any specific form to run your business or personal deeds, complying with your regional requirements. Professionals check all samples for their actuality, so you can be sure to prepare your documentation correctly.

Using the service is fairly easy. If you already have an account on the platform and your subscription is valid, you only need to log in, opt for the required form, and download it. You can retain the file in your profile anytime in the future. Otherwise, if you are new to the website, there will be a few more actions to complete before you obtain your Fairfax Sale of Deceased Partner's Interest:

- Examine the content of the page you’re on.

- Read the description of the sample or Preview it (if available).

- Search for another form using the corresponding option in the header.

- Click Buy Now when you’re certain in the selected file.

- Select the subscription plan that suits you most.

- Create an account on the platform or log in to proceed to payment options.

- Pay via PalPal or with your credit card.

- Switch the file format if necessary.

- Click Download to save the Fairfax Sale of Deceased Partner's Interest.

- Print the sample or use any preferred online editor to fill it out electronically.

No matter how many times you need to use the acquired document, you can locate all the samples you’ve ever saved in your profile by opening the My Forms tab. Try it out!