The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. TILA applies only to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use. This form was designed to cover an situation where the Seller is not a creditor as defined by the TILA.

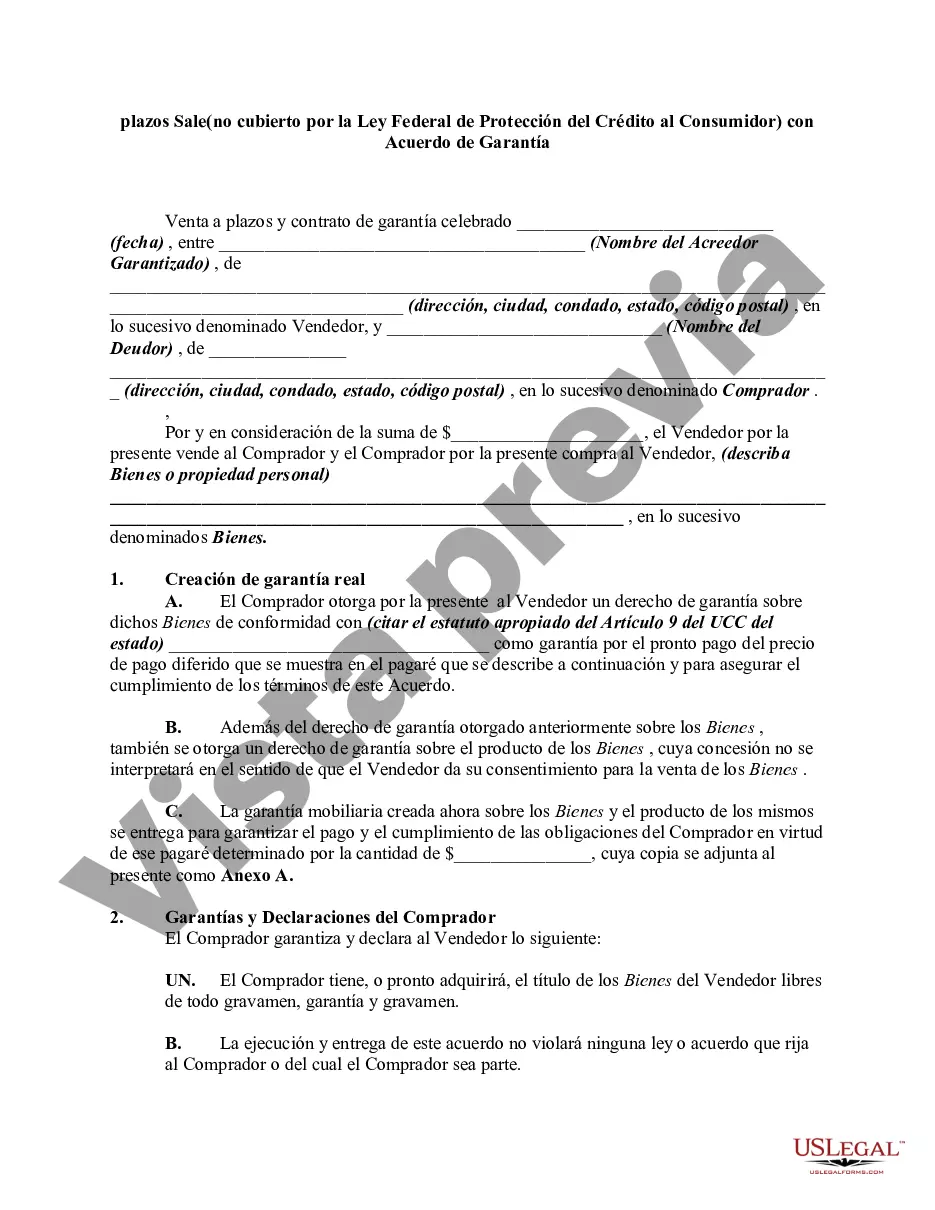

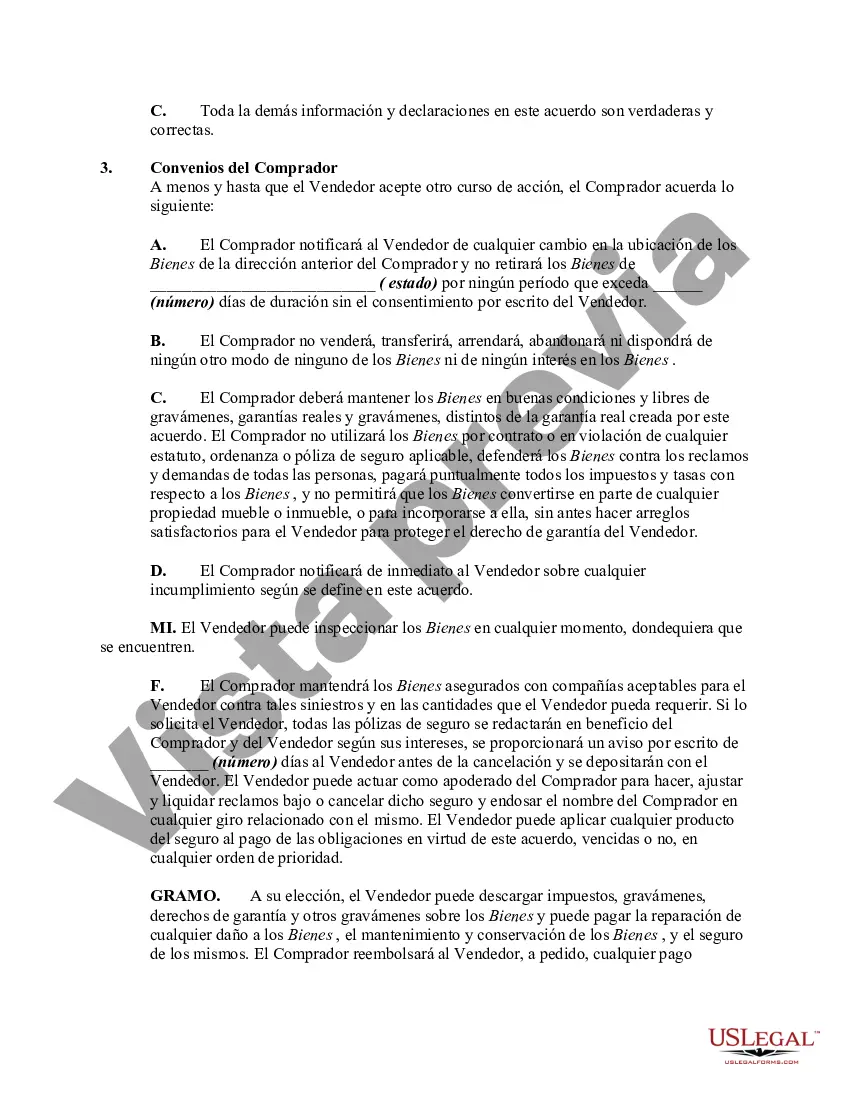

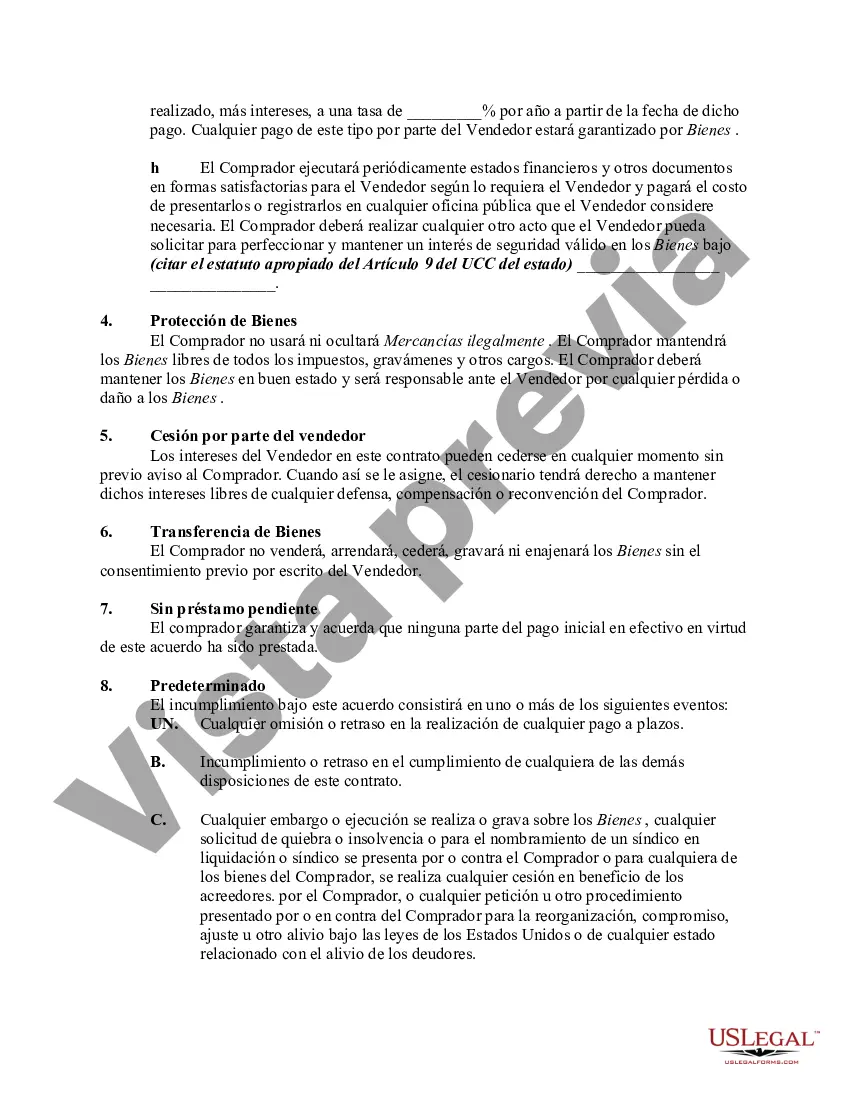

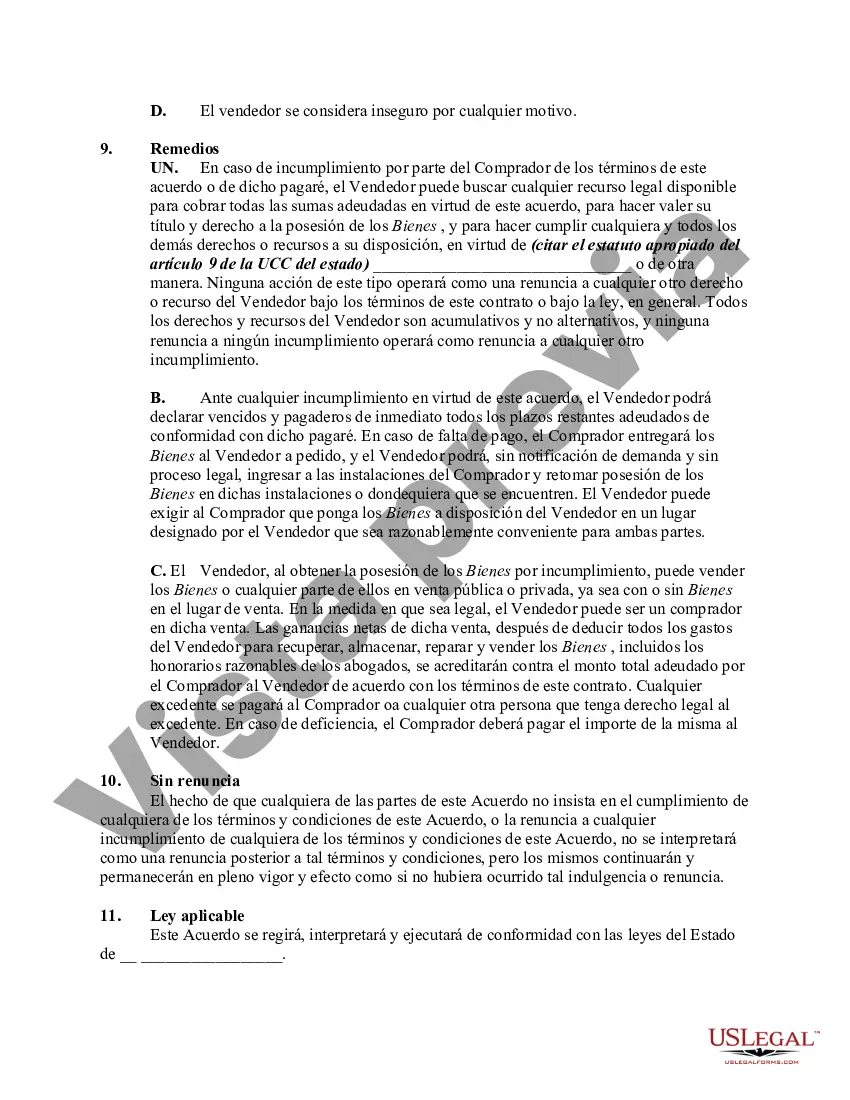

An installment sale refers to a sales transaction wherein a buyer agrees to make regular payments over a specified period to the seller. In Alameda, California, there are various types of installment sales that are not covered by the Federal Consumer Credit Protection Act (FC CPA) with a Security Agreement. Let's explore these different types and understand them in more detail. 1. Private Party Installment Sale: In private party installment sales, individuals or non-commercial entities sell goods or services to a buyer, with the payment structure divided into installments. These transactions are not subject to the FC CPA and are commonly used for selling used cars, appliances, furniture, or other personal items. 2. Real Estate Installment Sale: Real estate installment sales occur when a property owner sells their property to a buyer on an installment basis. This type of installment sale is not covered by the FC CPA, and buyers and sellers negotiate the terms, including the down payment, interest rate, and repayment period, through a security agreement. 3. Business-to-Business Installment Sale: Businesses often engage in installment sales with other businesses for goods or services. These sales fall outside the scope of the FC CPA since they do not involve consumers. Enterprises negotiate the terms and conditions, such as payment schedule, interest rates, and security agreements, to facilitate the sale of commercial or industrial goods. 4. Non-Regulated Lenders: Certain lenders or financing institutions may offer installment sales that do not fall under the FC CPA's coverage. These non-regulated lenders can provide installment loans or financing to individuals or businesses with specific terms and interest rates defined in the security agreement. It's important to note that while these types of installment sales are not covered by the FC CPA, other consumer protection laws, such as state-specific regulations and laws, may still apply to ensure fair and ethical practices. In Alameda, California, individuals and businesses engaging in installment sales that are not covered by the FC CPA should exercise caution and understanding when entering into these agreements. Proper legal advice and due diligence are recommended to ensure compliance with applicable laws and protect the rights and interests of all parties involved.An installment sale refers to a sales transaction wherein a buyer agrees to make regular payments over a specified period to the seller. In Alameda, California, there are various types of installment sales that are not covered by the Federal Consumer Credit Protection Act (FC CPA) with a Security Agreement. Let's explore these different types and understand them in more detail. 1. Private Party Installment Sale: In private party installment sales, individuals or non-commercial entities sell goods or services to a buyer, with the payment structure divided into installments. These transactions are not subject to the FC CPA and are commonly used for selling used cars, appliances, furniture, or other personal items. 2. Real Estate Installment Sale: Real estate installment sales occur when a property owner sells their property to a buyer on an installment basis. This type of installment sale is not covered by the FC CPA, and buyers and sellers negotiate the terms, including the down payment, interest rate, and repayment period, through a security agreement. 3. Business-to-Business Installment Sale: Businesses often engage in installment sales with other businesses for goods or services. These sales fall outside the scope of the FC CPA since they do not involve consumers. Enterprises negotiate the terms and conditions, such as payment schedule, interest rates, and security agreements, to facilitate the sale of commercial or industrial goods. 4. Non-Regulated Lenders: Certain lenders or financing institutions may offer installment sales that do not fall under the FC CPA's coverage. These non-regulated lenders can provide installment loans or financing to individuals or businesses with specific terms and interest rates defined in the security agreement. It's important to note that while these types of installment sales are not covered by the FC CPA, other consumer protection laws, such as state-specific regulations and laws, may still apply to ensure fair and ethical practices. In Alameda, California, individuals and businesses engaging in installment sales that are not covered by the FC CPA should exercise caution and understanding when entering into these agreements. Proper legal advice and due diligence are recommended to ensure compliance with applicable laws and protect the rights and interests of all parties involved.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.