The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. TILA applies only to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use. This form was designed to cover an situation where the Seller is not a creditor as defined by the TILA.

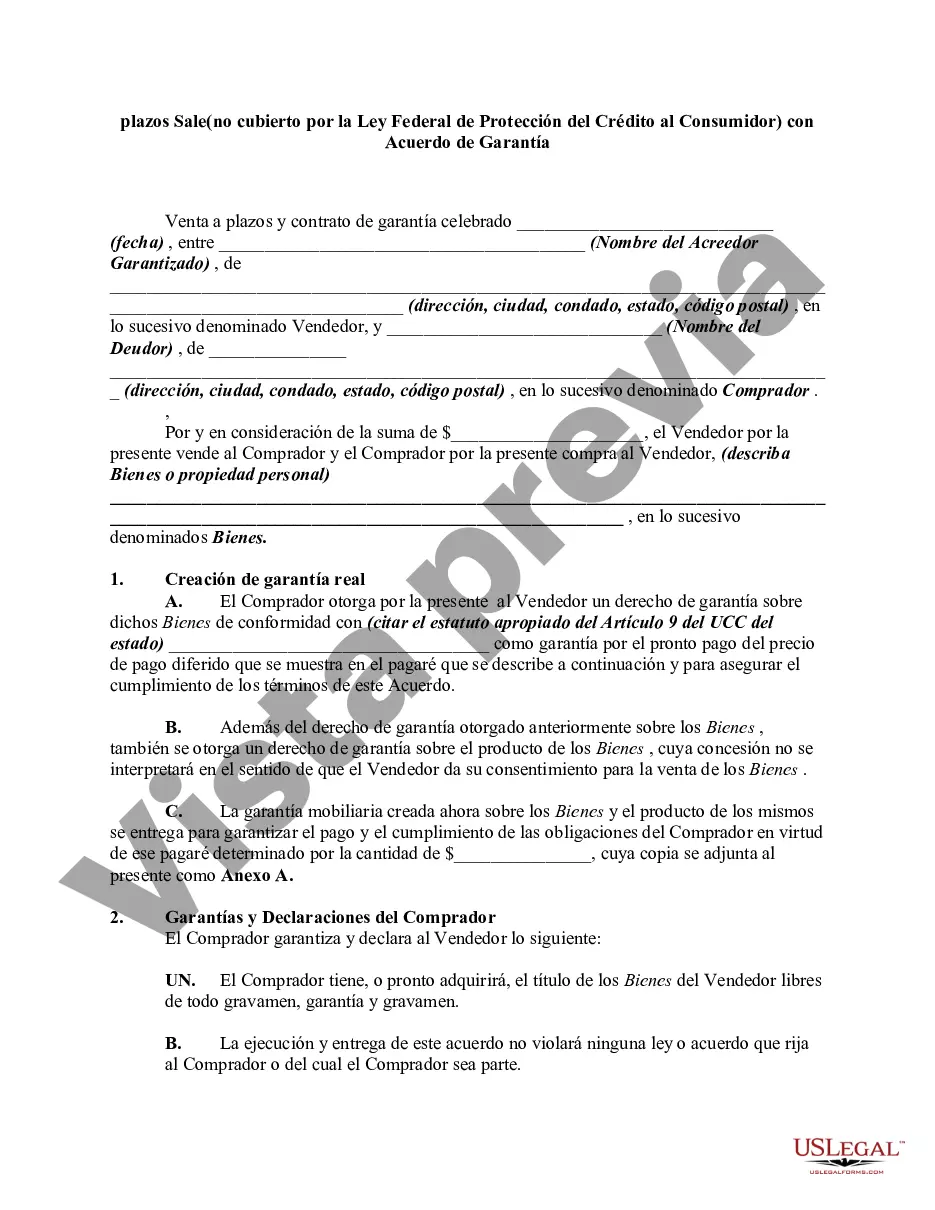

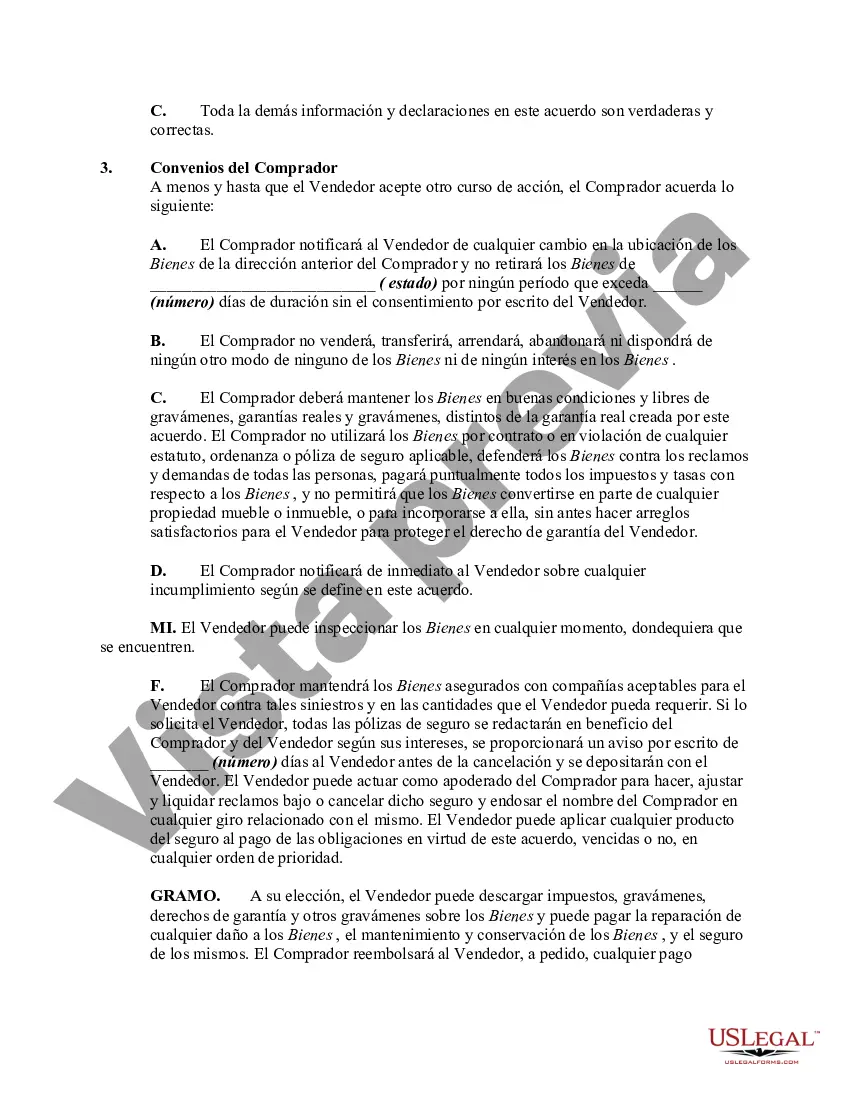

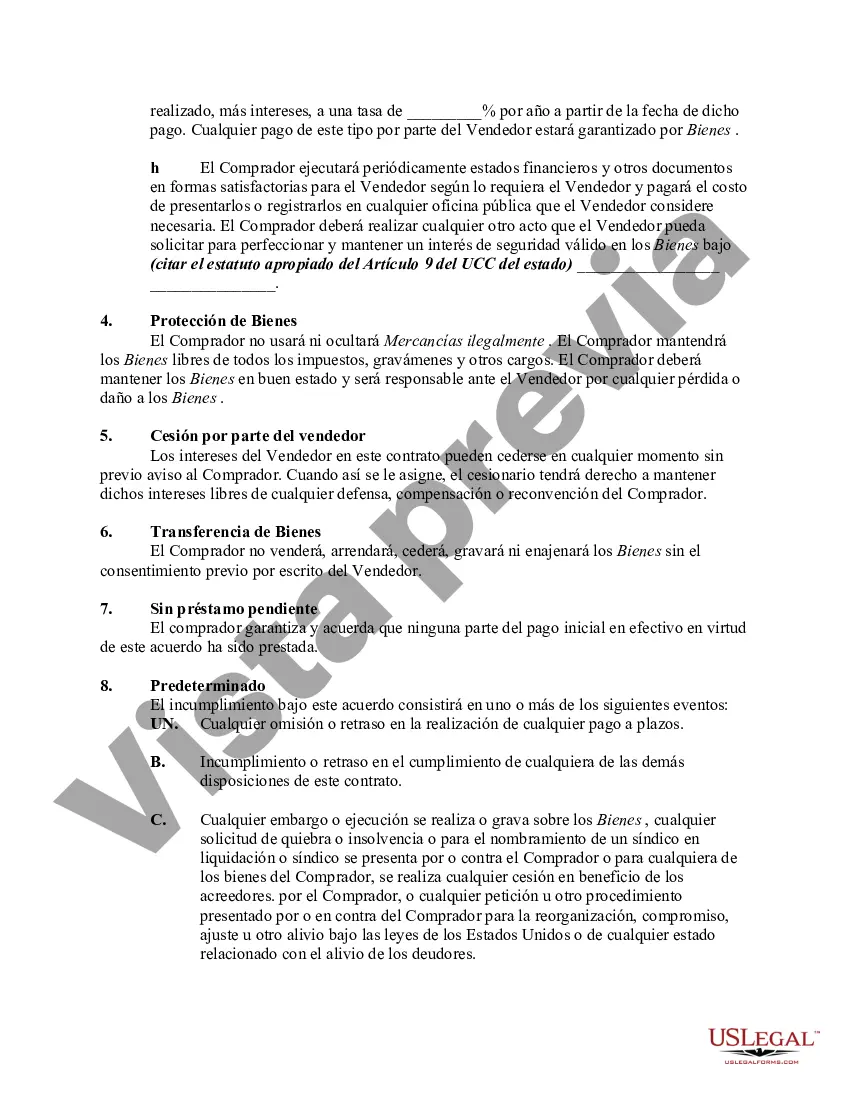

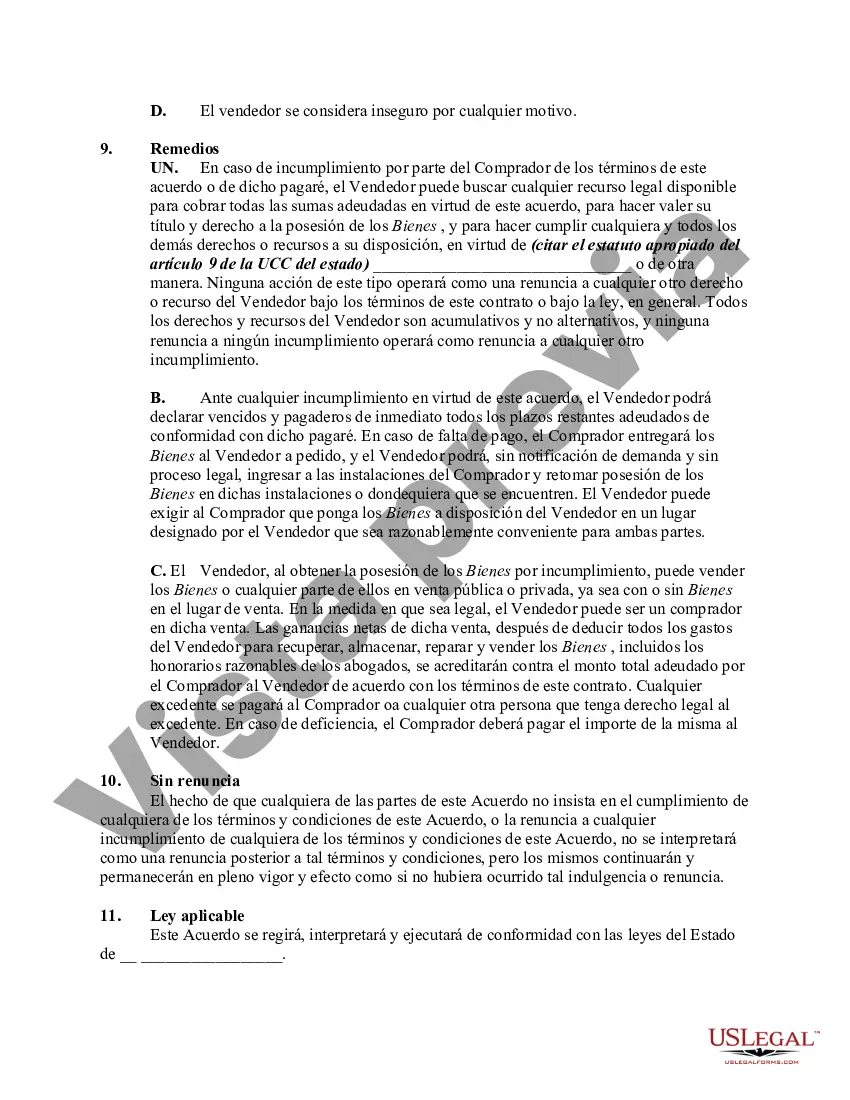

Oakland, Michigan, Installment Sale not covered by Federal Consumer Credit Protection Act with Security Agreement is a type of financing arrangement that falls outside the scope of the Federal Consumer Credit Protection Act (FC CPA). This means that certain protections and regulations provided by the FC CPA may not apply to these specific types of installment sale agreements in Oakland, Michigan. The essential characteristic of an Oakland, Michigan, Installment Sale not covered by the FC CPA with Security Agreement is the absence of federal consumer credit protection laws. While the FC CPA aims to safeguard consumers from unfair lending practices, prevent discrimination in credit transactions, and promote transparency in lending, these particular installment sale agreements in Oakland, Michigan, do not adhere to those federally mandated regulations. It is important to note that the exact types of Oakland, Michigan, Installment Sale not covered by the FC CPA with Security Agreement can vary. Some common examples include: 1. Seller Financing Contracts: These are agreements between the seller and the buyer, where the seller essentially acts as the lender, providing financing for the purchase of a property or an item. In such cases, the buyer makes installment payments directly to the seller, often with predetermined interest rates and payment schedules. 2. Buy Here Pay (BHP) Financing: This type of installment sale is popular in the automotive industry. Typically, car dealerships provide financing directly to buyers who may have poor credit or limited options to secure loans from traditional sources. BHP financing allows the buyer to make installment payments directly to the dealership, which often sells used vehicles. 3. In-house Financing: This refers to installment sale agreements where the seller or service provider offers financing for their products or services directly to the consumer. In these cases, the seller sets the terms, interest rates, and payment schedules. 4. Personal Loans from Family or Friends: In some instances, individuals may enter into an installment sale agreement with a family member or friend without involving traditional financial institutions. These agreements are often based on mutual trust and understanding, typically resulting in customized terms and conditions. 5. Peer-to-peer (P2P) Lending: Although P2P lending operates within an online marketplace, it can also fall under the Oakland, Michigan, installment sale category not covered by the FC CPA. P2P lending platforms connect borrowers directly with individual lenders or investors who fund the loan. It is crucial for both consumers and sellers engaged in Oakland, Michigan Installment Sale agreements not covered by the FC CPA with a Security Agreement to exercise caution and ensure complete transparency throughout the transaction. As the absence of FC CPA protections exposes consumers to potential risks, it is recommended that parties involved seek legal advice and thoroughly review all terms and conditions of the specific installment sale agreement before entering into such arrangements.Oakland, Michigan, Installment Sale not covered by Federal Consumer Credit Protection Act with Security Agreement is a type of financing arrangement that falls outside the scope of the Federal Consumer Credit Protection Act (FC CPA). This means that certain protections and regulations provided by the FC CPA may not apply to these specific types of installment sale agreements in Oakland, Michigan. The essential characteristic of an Oakland, Michigan, Installment Sale not covered by the FC CPA with Security Agreement is the absence of federal consumer credit protection laws. While the FC CPA aims to safeguard consumers from unfair lending practices, prevent discrimination in credit transactions, and promote transparency in lending, these particular installment sale agreements in Oakland, Michigan, do not adhere to those federally mandated regulations. It is important to note that the exact types of Oakland, Michigan, Installment Sale not covered by the FC CPA with Security Agreement can vary. Some common examples include: 1. Seller Financing Contracts: These are agreements between the seller and the buyer, where the seller essentially acts as the lender, providing financing for the purchase of a property or an item. In such cases, the buyer makes installment payments directly to the seller, often with predetermined interest rates and payment schedules. 2. Buy Here Pay (BHP) Financing: This type of installment sale is popular in the automotive industry. Typically, car dealerships provide financing directly to buyers who may have poor credit or limited options to secure loans from traditional sources. BHP financing allows the buyer to make installment payments directly to the dealership, which often sells used vehicles. 3. In-house Financing: This refers to installment sale agreements where the seller or service provider offers financing for their products or services directly to the consumer. In these cases, the seller sets the terms, interest rates, and payment schedules. 4. Personal Loans from Family or Friends: In some instances, individuals may enter into an installment sale agreement with a family member or friend without involving traditional financial institutions. These agreements are often based on mutual trust and understanding, typically resulting in customized terms and conditions. 5. Peer-to-peer (P2P) Lending: Although P2P lending operates within an online marketplace, it can also fall under the Oakland, Michigan, installment sale category not covered by the FC CPA. P2P lending platforms connect borrowers directly with individual lenders or investors who fund the loan. It is crucial for both consumers and sellers engaged in Oakland, Michigan Installment Sale agreements not covered by the FC CPA with a Security Agreement to exercise caution and ensure complete transparency throughout the transaction. As the absence of FC CPA protections exposes consumers to potential risks, it is recommended that parties involved seek legal advice and thoroughly review all terms and conditions of the specific installment sale agreement before entering into such arrangements.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.