The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. TILA applies only to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use. This form was designed to cover an situation where the Seller is not a creditor as defined by the TILA.

A Philadelphia Pennsylvania installment sale not covered by the Federal Consumer Credit Protection Act with a Security Agreement refers to a type of sales transaction where a buyer purchases goods or services from a seller in Philadelphia, Pennsylvania, on an installment basis, but outside the scope of the federal regulations imposed by the Consumer Credit Protection Act of the United States. This type of installment sale involves a security agreement that legally secures the seller's interest in the goods being sold until the buyer fulfills their financial obligations. The Federal Consumer Credit Protection Act was enacted to protect consumers by regulating the terms and conditions of credit transactions. However, certain types of installment sales in Philadelphia, Pennsylvania, may fall outside the scope of this act due to specific criteria or exemptions. Understanding the details and variations of installment sales is crucial for both sellers and buyers involved in Philadelphia's business landscape. Types of Philadelphia Pennsylvania Installment Sale not covered by Federal Consumer Credit Protection Act with Security Agreement: 1. Sales to Business Entities: The Federal Consumer Credit Protection Act primarily focuses on providing protection to individual consumers. Therefore, installment sales involving business entities or transactions made primarily for business purposes may not be subject to its regulations. This exemption encourages commercial transactions and allows businesses in Philadelphia to have more flexibility in structuring installment sales with security agreements. 2. Transactions with Cash Price above the Threshold: The Federal Consumer Credit Protection Act sets a threshold for the definition of a "consumer credit transaction." Installment sales in Philadelphia, Pennsylvania, with a cash price exceeding this threshold may not fall within the scope of the act. This exemption from federal regulations allows sellers to negotiate terms and interest rates more freely, accommodating higher-value transactions. 3. Sales with a Specific Repayment Period: Installment sales in Philadelphia may not be covered by federal regulations if they have a pre-determined repayment period that falls outside the parameters set by the Consumer Credit Protection Act. An agreement with terms deviating from the act's requirements provides more flexibility for sellers and buyers in Philadelphia to structure installment payments according to their specific needs. 4. Seller-Financed Sales: Installment sales where the seller directly extends credit to the buyer without involving any third-party financial institution or lender may be exempt from the Consumer Credit Protection Act. In such cases, the seller assumes greater responsibility for managing the risks associated with the credit extension, including drafting a comprehensive security agreement to protect their interests. In summary, a Philadelphia Pennsylvania installment sale not covered by the Federal Consumer Credit Protection Act with a Security Agreement refers to sales transactions that meet certain criteria or fall under particular exemptions specified by the act. Understanding the details of these exemptions allows sellers and buyers in Philadelphia to navigate installment sales with more freedom and flexibility while still adhering to state and local laws and regulations.A Philadelphia Pennsylvania installment sale not covered by the Federal Consumer Credit Protection Act with a Security Agreement refers to a type of sales transaction where a buyer purchases goods or services from a seller in Philadelphia, Pennsylvania, on an installment basis, but outside the scope of the federal regulations imposed by the Consumer Credit Protection Act of the United States. This type of installment sale involves a security agreement that legally secures the seller's interest in the goods being sold until the buyer fulfills their financial obligations. The Federal Consumer Credit Protection Act was enacted to protect consumers by regulating the terms and conditions of credit transactions. However, certain types of installment sales in Philadelphia, Pennsylvania, may fall outside the scope of this act due to specific criteria or exemptions. Understanding the details and variations of installment sales is crucial for both sellers and buyers involved in Philadelphia's business landscape. Types of Philadelphia Pennsylvania Installment Sale not covered by Federal Consumer Credit Protection Act with Security Agreement: 1. Sales to Business Entities: The Federal Consumer Credit Protection Act primarily focuses on providing protection to individual consumers. Therefore, installment sales involving business entities or transactions made primarily for business purposes may not be subject to its regulations. This exemption encourages commercial transactions and allows businesses in Philadelphia to have more flexibility in structuring installment sales with security agreements. 2. Transactions with Cash Price above the Threshold: The Federal Consumer Credit Protection Act sets a threshold for the definition of a "consumer credit transaction." Installment sales in Philadelphia, Pennsylvania, with a cash price exceeding this threshold may not fall within the scope of the act. This exemption from federal regulations allows sellers to negotiate terms and interest rates more freely, accommodating higher-value transactions. 3. Sales with a Specific Repayment Period: Installment sales in Philadelphia may not be covered by federal regulations if they have a pre-determined repayment period that falls outside the parameters set by the Consumer Credit Protection Act. An agreement with terms deviating from the act's requirements provides more flexibility for sellers and buyers in Philadelphia to structure installment payments according to their specific needs. 4. Seller-Financed Sales: Installment sales where the seller directly extends credit to the buyer without involving any third-party financial institution or lender may be exempt from the Consumer Credit Protection Act. In such cases, the seller assumes greater responsibility for managing the risks associated with the credit extension, including drafting a comprehensive security agreement to protect their interests. In summary, a Philadelphia Pennsylvania installment sale not covered by the Federal Consumer Credit Protection Act with a Security Agreement refers to sales transactions that meet certain criteria or fall under particular exemptions specified by the act. Understanding the details of these exemptions allows sellers and buyers in Philadelphia to navigate installment sales with more freedom and flexibility while still adhering to state and local laws and regulations.

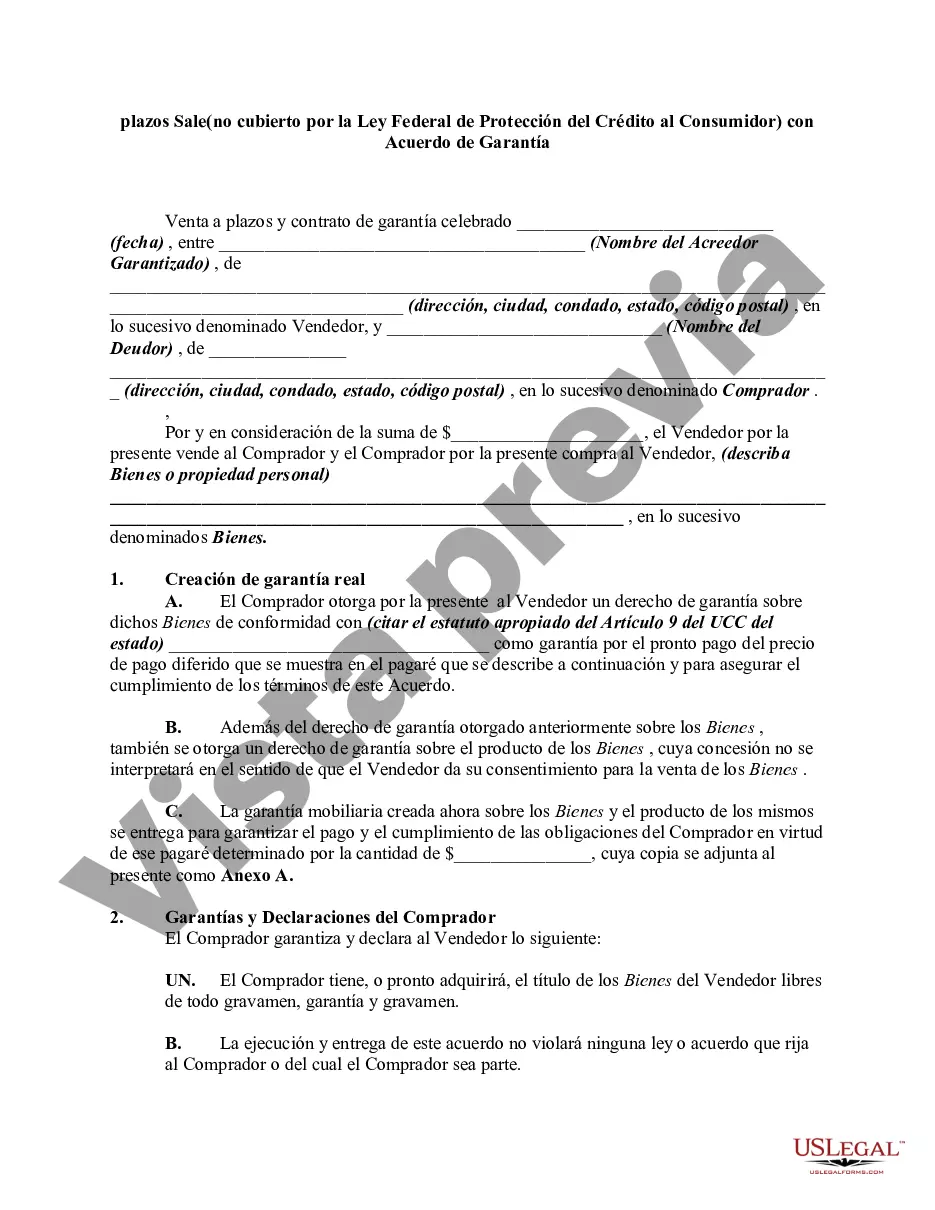

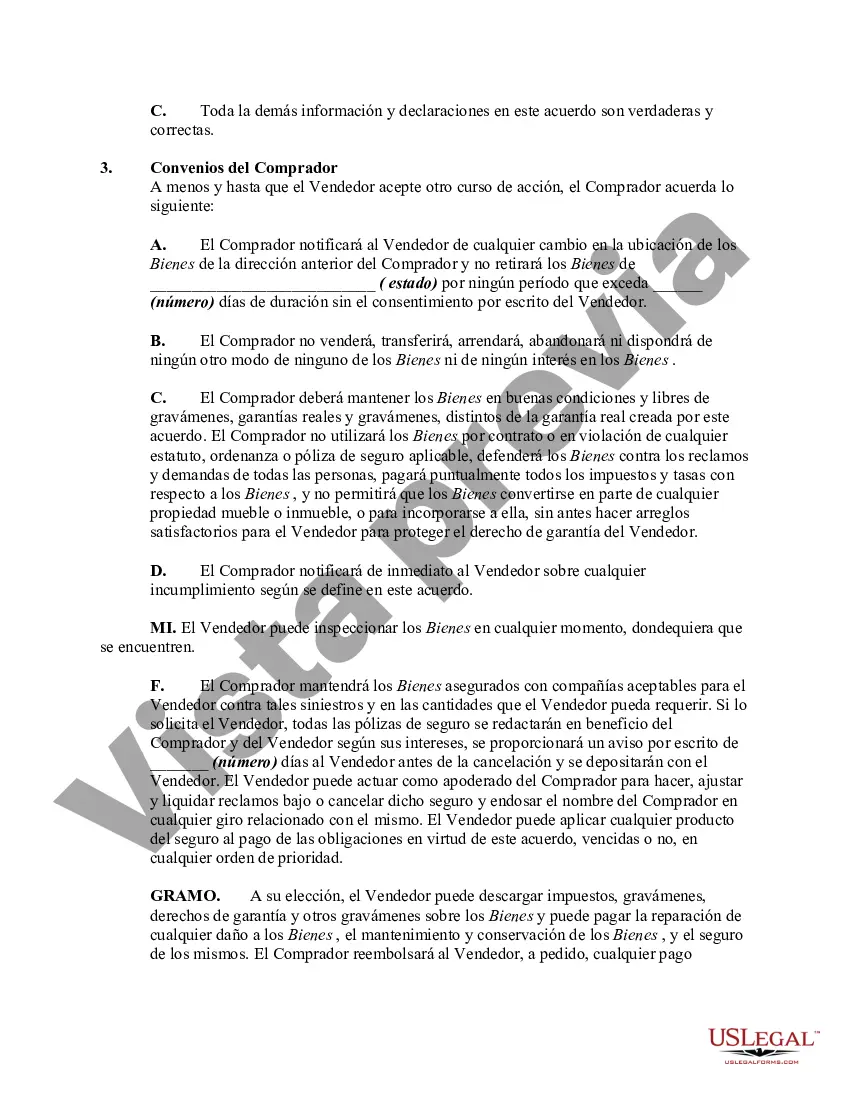

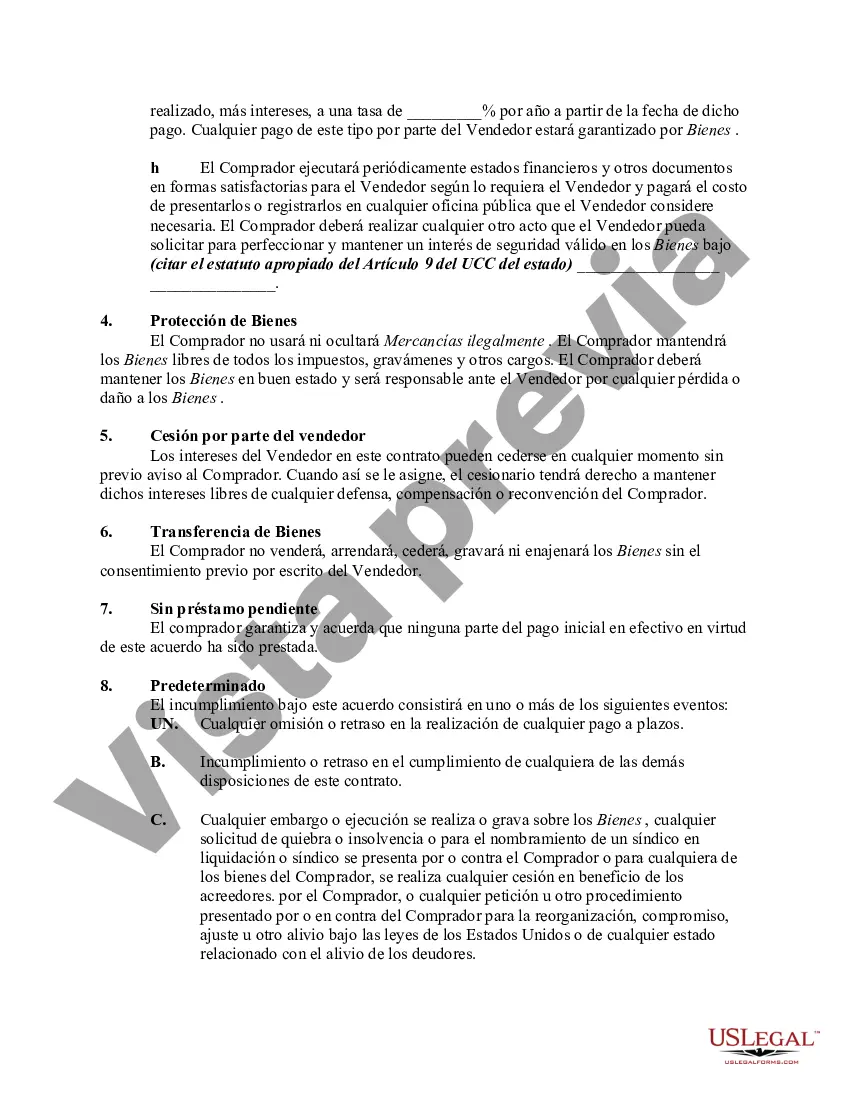

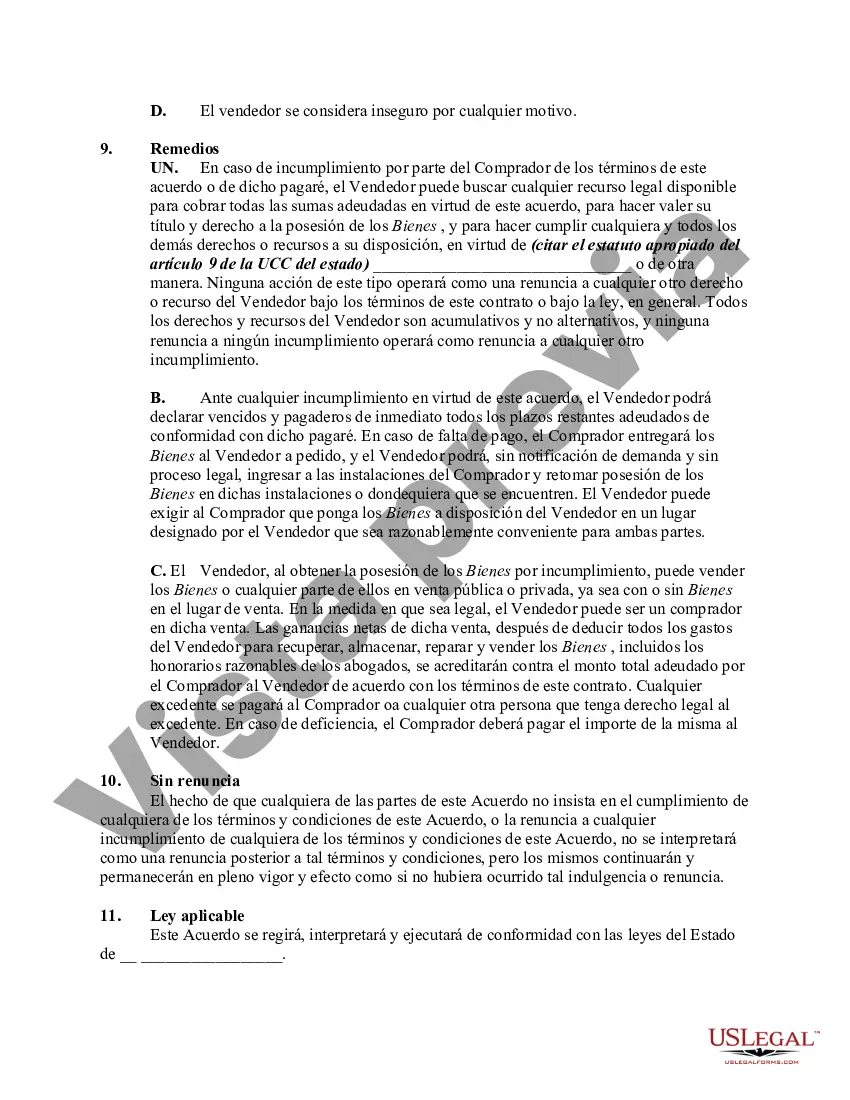

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.