The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. TILA applies only to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use. This form was designed to cover an situation where the Seller is not a creditor as defined by the TILA.

Lima, Arizona, Installment Sale not covered by the Federal Consumer Credit Protection Act with Security Agreement refers to a specific type of financial transaction that falls outside the purview of federal consumer credit protection regulations. In such cases, there are several types of installment sales that are not covered by these regulations and can vary based on specific circumstances. Some common examples include: 1. Non-commercial Installment Sales: When an individual or a private party engages in an installment sale, such as selling a personal vehicle or property to another individual, it generally falls outside the scope of the federal consumer credit protection laws. These sales are usually conducted directly between the buyer and seller, without involving a commercial lending institution. 2. Private Loans: If an individual borrows money from another individual, friend, or family member, and they agree to an installment payment plan with a security agreement, it is typically not covered by the federal consumer credit protection laws. These private loans are often made on an informal basis and may not involve complex legal documentation. 3. Interfamily Transactions: When family members engage in financial transactions among themselves, such as parents lending money to their children or siblings conducting installment sales between each other, it generally falls outside the federal consumer credit protection regulations. These transactions are usually based on trust and personal relationships rather than commercial relationships. 4. Seller Financing: In certain cases, when property owners or businesses provide financing to buyers directly, bypassing traditional lending institutions, and agree on an installment sale with a security agreement, it may not be protected by the federal consumer credit protection laws. This arrangement can be common in real estate transactions, where the seller acts as the lender to facilitate the sale. It is important to note that while these installment sales may not be covered by federal consumer credit protection laws, other state-specific laws or regulations might apply. Therefore, it is advisable for both buyers and sellers to seek legal advice and ensure compliance with any relevant state laws pertaining to installment sales and security agreements in Lima, Arizona, or any other jurisdiction.

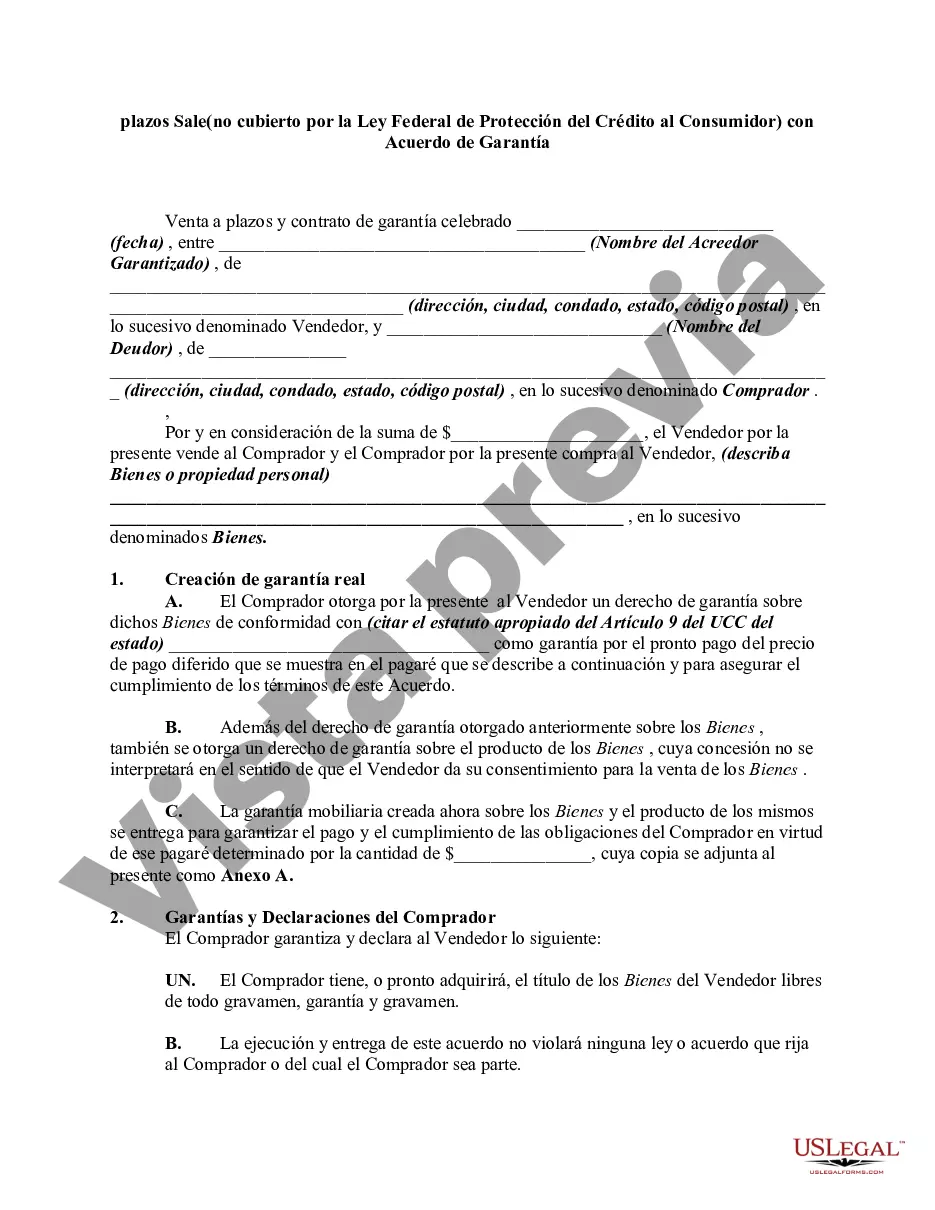

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.