As most commonly used in legal settings, an audit is an examination of financial records and documents and other evidence by a trained accountant. Audits are conducted of records of a business or governmental entity, with the aim of ensuring proper accounting practices, recommendations for improvements, and a balancing of the books. An audit performed by employees is called "internal audit," and one done by an independent (outside) accountant is an "independent audit." Auditors may refuse to sign the audit to guarantee its accuracy if only limited records are produced.

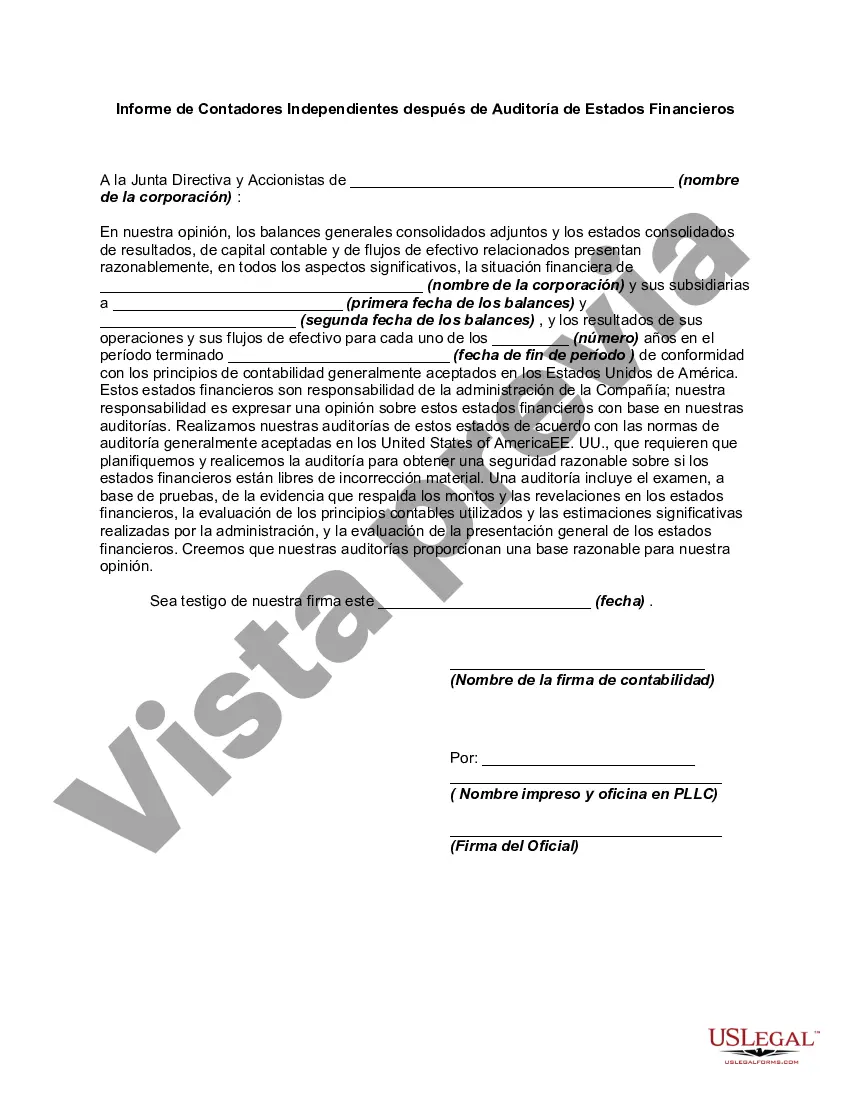

Mecklenburg County, North Carolina Report of Independent Accountants after Audit of Financial Statements is a comprehensive review conducted by independent accounting firms to assess the financial health and transparency of Mecklenburg County's financial statements. The purpose of the Mecklenburg County Report of Independent Accountants after Audit of Financial Statements is to provide an unbiased evaluation of the financial position, operational efficiency, and the accuracy of financial information presented by Mecklenburg County. This report helps stakeholders, including county residents, government officials, investors, and creditors, make informed decisions based on reliable financial data. The independent accountants conduct a detailed examination of Mecklenburg County's financial statements, including balance sheets, income statements, cash flow statements, and notes to the financial statements. They examine transactions, records, internal controls, and accounting practices ensuring compliance with Generally Accepted Accounting Principles (GAAP) and other applicable legal requirements. The Mecklenburg County Report of Independent Accountants after Audit of Financial Statements provides an opinion on whether the financial statements accurately present the financial position of the county based on the audit findings. The opinion is typically presented in one of the following formats: 1. Unqualified Opinion: This is the most desirable opinion as it indicates that the financial statements are fairly presented without any material misstatements. It provides the highest level of assurance to users of the financial statements. 2. Qualified Opinion: A qualified opinion is issued when the independent accountants identify specific departures from GAAP or other legal requirements that have a significant impact on the financial statements. While the overall financial statements may be reliable, the specific qualified areas require attention. 3. Adverse Opinion: An adverse opinion is conveyed when the independent accountants find that the financial statements are materially misstated, resulting in an overall lack of reliability. This opinion indicates serious issues and raises concerns regarding the accuracy and validity of the financial statements. 4. Disclaimer of Opinion: A disclaimer of opinion may occur if the independent accountants are unable to form an opinion due to pervasive limitations on the scope of the audit or an inability to obtain sufficient appropriate evidence. This opinion signifies a lack of reliability due to significant constraints during the audit process. The Mecklenburg County Report of Independent Accountants after Audit of Financial Statements adds credibility to the financial information provided by the county and promotes transparency in public financial management. It enhances trust among stakeholders and facilitates informed decision-making regarding governmental budgets, investments, bond offerings, and other financial matters. In conclusion, Mecklenburg County, North Carolina, undergoes an annual audit of its financial statements conducted by independent accounting firms. The resulting Mecklenburg County Report of Independent Accountants after Audit of Financial Statements provides an objective evaluation of the county's financial health, assists stakeholders in making informed decisions, and ensures transparency and accountability in public financial management.Mecklenburg County, North Carolina Report of Independent Accountants after Audit of Financial Statements is a comprehensive review conducted by independent accounting firms to assess the financial health and transparency of Mecklenburg County's financial statements. The purpose of the Mecklenburg County Report of Independent Accountants after Audit of Financial Statements is to provide an unbiased evaluation of the financial position, operational efficiency, and the accuracy of financial information presented by Mecklenburg County. This report helps stakeholders, including county residents, government officials, investors, and creditors, make informed decisions based on reliable financial data. The independent accountants conduct a detailed examination of Mecklenburg County's financial statements, including balance sheets, income statements, cash flow statements, and notes to the financial statements. They examine transactions, records, internal controls, and accounting practices ensuring compliance with Generally Accepted Accounting Principles (GAAP) and other applicable legal requirements. The Mecklenburg County Report of Independent Accountants after Audit of Financial Statements provides an opinion on whether the financial statements accurately present the financial position of the county based on the audit findings. The opinion is typically presented in one of the following formats: 1. Unqualified Opinion: This is the most desirable opinion as it indicates that the financial statements are fairly presented without any material misstatements. It provides the highest level of assurance to users of the financial statements. 2. Qualified Opinion: A qualified opinion is issued when the independent accountants identify specific departures from GAAP or other legal requirements that have a significant impact on the financial statements. While the overall financial statements may be reliable, the specific qualified areas require attention. 3. Adverse Opinion: An adverse opinion is conveyed when the independent accountants find that the financial statements are materially misstated, resulting in an overall lack of reliability. This opinion indicates serious issues and raises concerns regarding the accuracy and validity of the financial statements. 4. Disclaimer of Opinion: A disclaimer of opinion may occur if the independent accountants are unable to form an opinion due to pervasive limitations on the scope of the audit or an inability to obtain sufficient appropriate evidence. This opinion signifies a lack of reliability due to significant constraints during the audit process. The Mecklenburg County Report of Independent Accountants after Audit of Financial Statements adds credibility to the financial information provided by the county and promotes transparency in public financial management. It enhances trust among stakeholders and facilitates informed decision-making regarding governmental budgets, investments, bond offerings, and other financial matters. In conclusion, Mecklenburg County, North Carolina, undergoes an annual audit of its financial statements conducted by independent accounting firms. The resulting Mecklenburg County Report of Independent Accountants after Audit of Financial Statements provides an objective evaluation of the county's financial health, assists stakeholders in making informed decisions, and ensures transparency and accountability in public financial management.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.