As most commonly used in legal settings, an audit is an examination of financial records and documents and other evidence by a trained accountant. Audits are conducted of records of a business or governmental entity, with the aim of ensuring proper accounting practices, recommendations for improvements, and a balancing of the books. An audit performed by employees is called "internal audit," and one done by an independent (outside) accountant is an "independent audit." Auditors may refuse to sign the audit to guarantee its accuracy if only limited records are produced.

Montgomery, Maryland is a county located in the state of Maryland, United States. It is a thriving and diverse community with a population of over 1 million residents. The county is known for its rich history, cultural attractions, and strong economy. The Montgomery Maryland Report of Independent Accountants after Audit of Financial Statements is a document that provides an assessment of the financial health and performance of the county government. This report is conducted by independent accountants who review the financial statements, records, and internal controls of the county's financial operations. The objective of the Montgomery Maryland Report of Independent Accountants after Audit of Financial Statements is to provide assurance to the stakeholders, including the county government, taxpayers, investors, and creditors, about the accuracy, reliability, and transparency of the financial information provided by the county. The report examines various aspects of the financial statements, including the balance sheet, income statement, cash flow statement, and footnotes. The independent accountants assess the compliance with accounting principles, government regulations, and internal policies. They also test the effectiveness of internal controls and the reliability of the financial reporting process. The Montgomery Maryland Report of Independent Accountants after Audit of Financial Statements is a crucial tool for decision-making and accountability purposes. It helps the county government to evaluate its financial performance, identify areas of improvement, and make sound financial decisions. It also provides transparency to taxpayers and other stakeholders, ensuring that the county's financial information is accurate, reliable, and compliant with applicable standards. Different types of Montgomery Maryland Reports of Independent Accountants after Audit of Financial Statements may include the following: 1. Unqualified Opinion: This type of report is issued when the independent accountants express an opinion that the financial statements are presented fairly in all material aspects and comply with generally accepted accounting principles. 2. Qualified Opinion: A qualified opinion is issued when the accountants encounter certain limitation of scope or exceptions that have materially affected the financial statements. This means that while most of the financial statements are accurate, there are specific areas that may require further examination or corrections. 3. Adverse Opinion: An adverse opinion is the most critical type of report. It is issued when the accountants find significant departures from generally accepted accounting principles, which materially impact the financial statements. This opinion indicates that the financial statements are not presented fairly and should not be relied upon. 4. Disclaimer of Opinion: In rare cases, the independent accountants may issue a disclaimer of opinion when they are unable to express an opinion due to significant limitations on the scope of their audit or the lack of sufficient evidence to support their opinion. In conclusion, the Montgomery Maryland Report of Independent Accountants after Audit of Financial Statements is a crucial assessment of the county government's financial health and performance. It provides assurance to stakeholders and ensures transparency and accountability. The report may vary in opinion types, including unqualified, qualified, adverse, or a disclaimer of opinion, depending on the findings of the independent auditors.Montgomery, Maryland is a county located in the state of Maryland, United States. It is a thriving and diverse community with a population of over 1 million residents. The county is known for its rich history, cultural attractions, and strong economy. The Montgomery Maryland Report of Independent Accountants after Audit of Financial Statements is a document that provides an assessment of the financial health and performance of the county government. This report is conducted by independent accountants who review the financial statements, records, and internal controls of the county's financial operations. The objective of the Montgomery Maryland Report of Independent Accountants after Audit of Financial Statements is to provide assurance to the stakeholders, including the county government, taxpayers, investors, and creditors, about the accuracy, reliability, and transparency of the financial information provided by the county. The report examines various aspects of the financial statements, including the balance sheet, income statement, cash flow statement, and footnotes. The independent accountants assess the compliance with accounting principles, government regulations, and internal policies. They also test the effectiveness of internal controls and the reliability of the financial reporting process. The Montgomery Maryland Report of Independent Accountants after Audit of Financial Statements is a crucial tool for decision-making and accountability purposes. It helps the county government to evaluate its financial performance, identify areas of improvement, and make sound financial decisions. It also provides transparency to taxpayers and other stakeholders, ensuring that the county's financial information is accurate, reliable, and compliant with applicable standards. Different types of Montgomery Maryland Reports of Independent Accountants after Audit of Financial Statements may include the following: 1. Unqualified Opinion: This type of report is issued when the independent accountants express an opinion that the financial statements are presented fairly in all material aspects and comply with generally accepted accounting principles. 2. Qualified Opinion: A qualified opinion is issued when the accountants encounter certain limitation of scope or exceptions that have materially affected the financial statements. This means that while most of the financial statements are accurate, there are specific areas that may require further examination or corrections. 3. Adverse Opinion: An adverse opinion is the most critical type of report. It is issued when the accountants find significant departures from generally accepted accounting principles, which materially impact the financial statements. This opinion indicates that the financial statements are not presented fairly and should not be relied upon. 4. Disclaimer of Opinion: In rare cases, the independent accountants may issue a disclaimer of opinion when they are unable to express an opinion due to significant limitations on the scope of their audit or the lack of sufficient evidence to support their opinion. In conclusion, the Montgomery Maryland Report of Independent Accountants after Audit of Financial Statements is a crucial assessment of the county government's financial health and performance. It provides assurance to stakeholders and ensures transparency and accountability. The report may vary in opinion types, including unqualified, qualified, adverse, or a disclaimer of opinion, depending on the findings of the independent auditors.

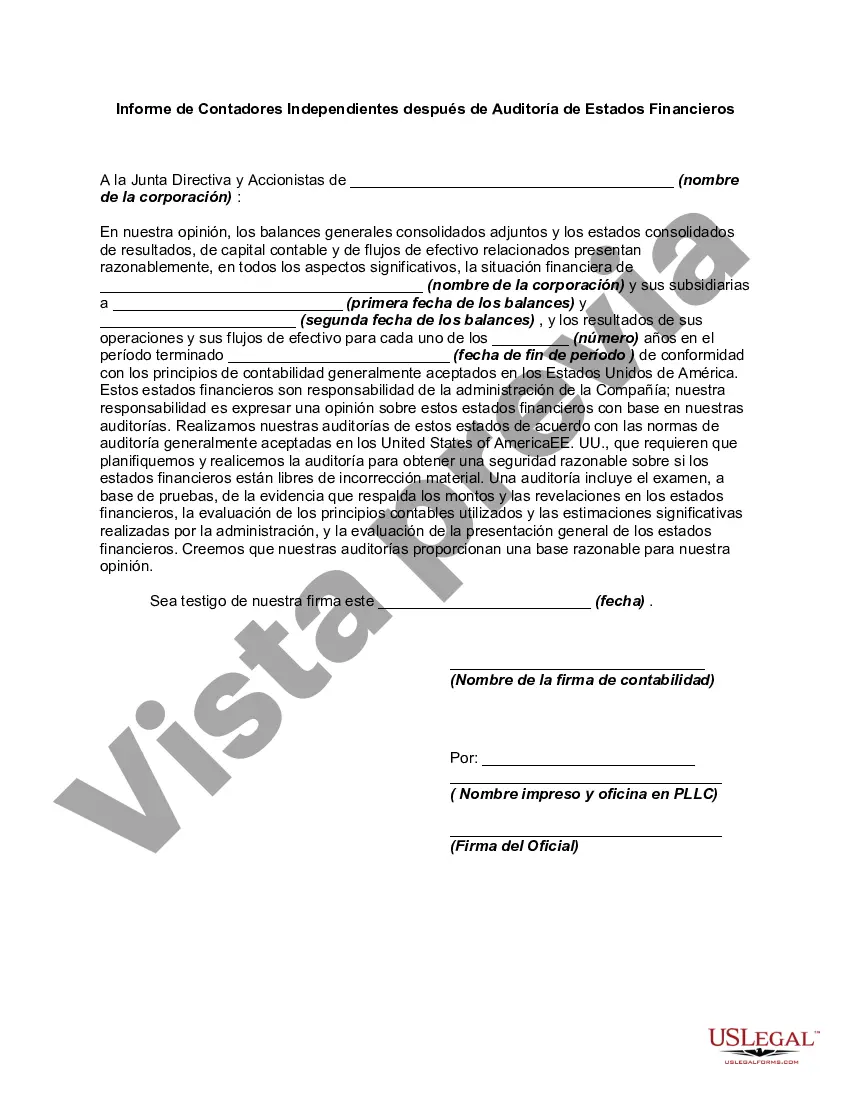

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.