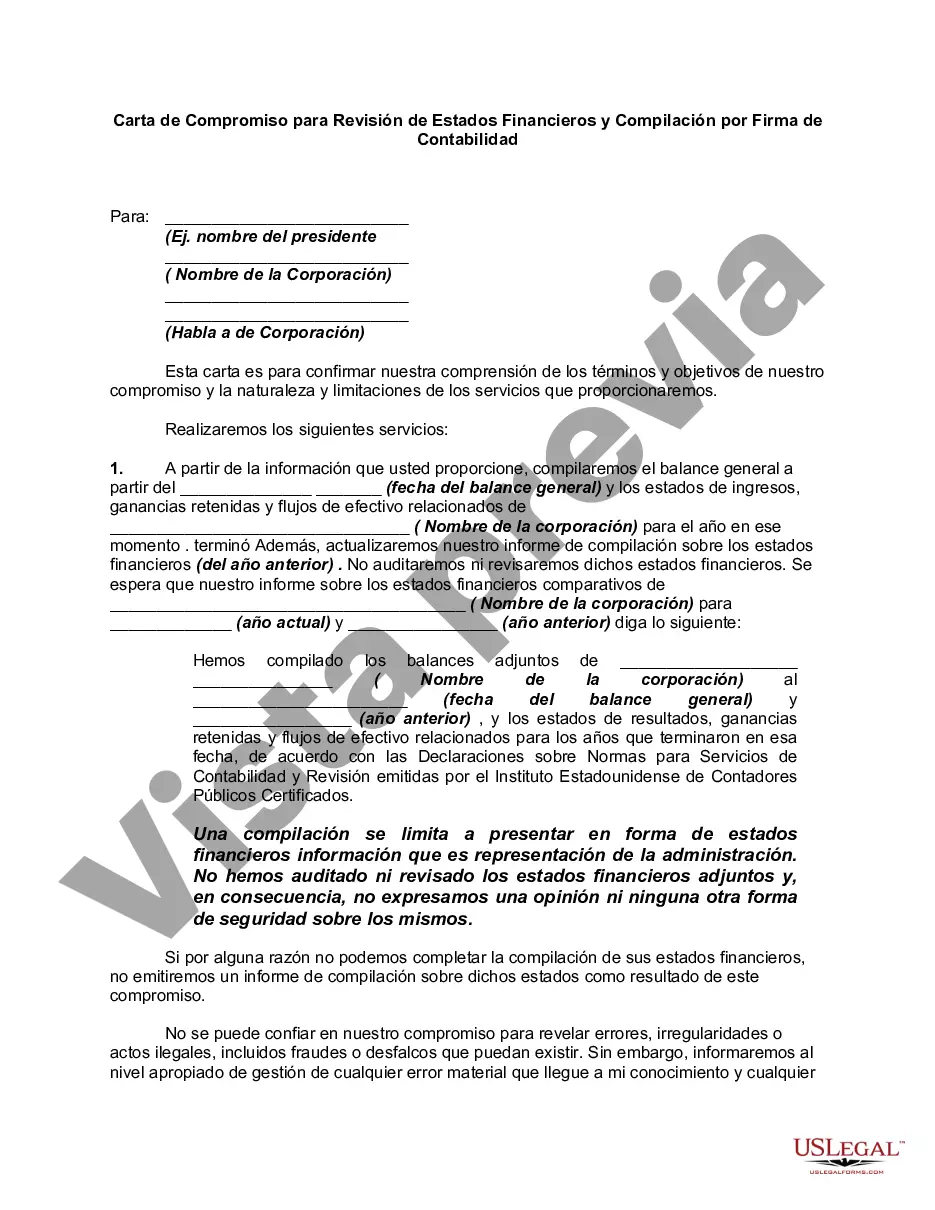

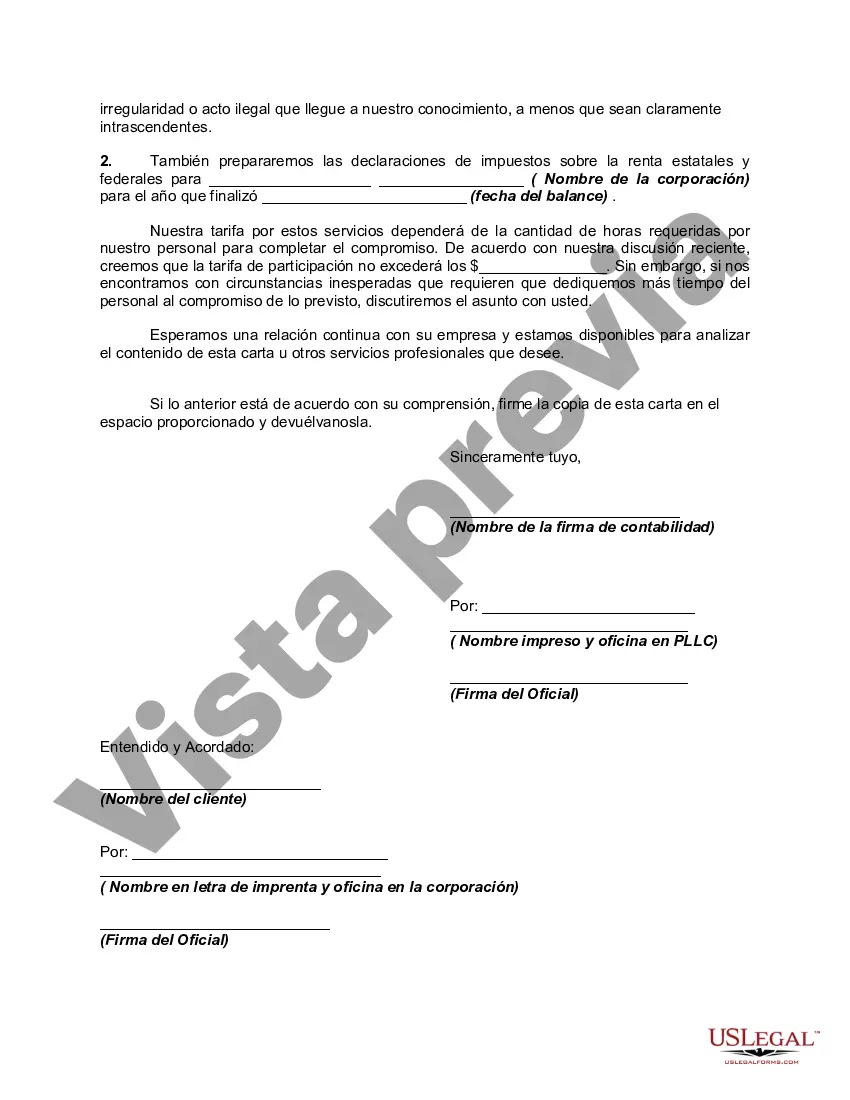

Compiled financial statements represent the most basic level of service that certified public accountants provide with respect to financial statements. In a compilation, the CPA must comply with certain basic requirements of professional standards, such as having a knowledge of the client's industry and applicable accounting principles, having a clear understanding with the client as to the services to be provided, and reading the financial statements to determine whether there are any obvious departures from generally accepted accounting principles (or, in some cases, another comprehensive basis of accounting used by the entity). It may be necessary for the CPA to perform "other accounting services" (such as creating a general ledger for the client, or assisting the client with adjusting entries for the books of the client (before the financial statements can be prepared). Upon completion, a report on the financial statements is issued that states a compilation was performed in accordance with AICPA professional standards, but no assurance is expressed that the statements are in conformity with generally accepted accounting principles. This is known as the expression of "no assurance." Compiled financial statements are often prepared for privately-held entities that do not need a higher level of assurance expressed by the CPA.

Mecklenburg North Carolina Engagement Letter for Review of Financial Statements and Compilation by Accounting Firm: An engagement letter is a vital document that outlines the terms and conditions of an agreement between a client and an accounting firm in Mecklenburg, North Carolina, for the review of financial statements and compilation services. The engagement letter serves as a crucial communication tool that defines the scope of work, responsibilities, and obligations of both parties involved in the engagement process. The Mecklenburg North Carolina Engagement Letter for Review of Financial Statements and Compilation by an Accounting Firm typically includes the following key components: 1. Introduction: The engagement letter begins with an introduction that establishes the professional relationship between the accounting firm and the client. It includes the names and addresses of both parties involved, ensuring clarity and identification. 2. Objective and Scope: This section outlines the specific purpose of the engagement, whether it is a review of financial statements or compilation services. The engagement letter should clearly state the extent of the review, including the period covered and the level of assurance provided. 3. Responsibilities of the Client: The engagement letter outlines the obligations and responsibilities of the client, such as providing accurate and complete financial records, access to necessary documentation, and timely responses to queries. It also emphasizes the client's ultimate responsibility for the financial statements' accuracy and fairness. 4. Responsibilities of the Accounting Firm: This section outlines the responsibilities of the accounting firm, including conducting the review or compilation in accordance with relevant professional standards and regulations. It may also highlight the credentials and expertise of the firm's staff members assigned to the engagement. 5. Limitations and Restrictions: The engagement letter identifies any inherent limitations associated with the review or compilation process. This may include the fact that a review does not provide absolute assurance, or that compilation services do not entail verification or validation of the financial information. 6. Timeline and Deliverables: The engagement letter includes a timeline or estimated completion date for the engagement process. It also outlines the expected deliverables, such as the review report or compiled financial statements, and any other agreed-upon deliverables. 7. Fees and Payment Terms: This section specifies the accounting firm's fees for the engagement and outlines the payment terms, including the frequency and method of payment. It is essential to be clear and transparent about the financial arrangements to avoid any misunderstandings later on. 8. Termination Clause: The engagement letter may include a termination clause that outlines the conditions under which either party can terminate the engagement. This clause provides clarity and protection for both parties involved. Different types of Mecklenburg North Carolina Engagement Letters for Review of Financial Statements and Compilation by an Accounting Firm may include engagements for: 1. Reviews of Historical Financial Statements: This type of engagement letter primarily focuses on conducting a thorough review of historical financial statements to provide limited assurance regarding their accuracy and conformity with the applicable financial reporting framework. 2. Compilation of Financial Statements: This type of engagement letter is formulated when an accounting firm is engaged to take information provided by the client and present it in the form of financial statements without providing any form of assurance on the information's accuracy. In conclusion, the Mecklenburg North Carolina Engagement Letter for Review of Financial Statements and Compilation by an Accounting Firm is a foundational document that outlines the terms, objectives, responsibilities, and limitations of an engagement. It ensures clear communication and mutual understanding between the accounting firm and the client, promoting a successful and efficient engagement process.Mecklenburg North Carolina Engagement Letter for Review of Financial Statements and Compilation by Accounting Firm: An engagement letter is a vital document that outlines the terms and conditions of an agreement between a client and an accounting firm in Mecklenburg, North Carolina, for the review of financial statements and compilation services. The engagement letter serves as a crucial communication tool that defines the scope of work, responsibilities, and obligations of both parties involved in the engagement process. The Mecklenburg North Carolina Engagement Letter for Review of Financial Statements and Compilation by an Accounting Firm typically includes the following key components: 1. Introduction: The engagement letter begins with an introduction that establishes the professional relationship between the accounting firm and the client. It includes the names and addresses of both parties involved, ensuring clarity and identification. 2. Objective and Scope: This section outlines the specific purpose of the engagement, whether it is a review of financial statements or compilation services. The engagement letter should clearly state the extent of the review, including the period covered and the level of assurance provided. 3. Responsibilities of the Client: The engagement letter outlines the obligations and responsibilities of the client, such as providing accurate and complete financial records, access to necessary documentation, and timely responses to queries. It also emphasizes the client's ultimate responsibility for the financial statements' accuracy and fairness. 4. Responsibilities of the Accounting Firm: This section outlines the responsibilities of the accounting firm, including conducting the review or compilation in accordance with relevant professional standards and regulations. It may also highlight the credentials and expertise of the firm's staff members assigned to the engagement. 5. Limitations and Restrictions: The engagement letter identifies any inherent limitations associated with the review or compilation process. This may include the fact that a review does not provide absolute assurance, or that compilation services do not entail verification or validation of the financial information. 6. Timeline and Deliverables: The engagement letter includes a timeline or estimated completion date for the engagement process. It also outlines the expected deliverables, such as the review report or compiled financial statements, and any other agreed-upon deliverables. 7. Fees and Payment Terms: This section specifies the accounting firm's fees for the engagement and outlines the payment terms, including the frequency and method of payment. It is essential to be clear and transparent about the financial arrangements to avoid any misunderstandings later on. 8. Termination Clause: The engagement letter may include a termination clause that outlines the conditions under which either party can terminate the engagement. This clause provides clarity and protection for both parties involved. Different types of Mecklenburg North Carolina Engagement Letters for Review of Financial Statements and Compilation by an Accounting Firm may include engagements for: 1. Reviews of Historical Financial Statements: This type of engagement letter primarily focuses on conducting a thorough review of historical financial statements to provide limited assurance regarding their accuracy and conformity with the applicable financial reporting framework. 2. Compilation of Financial Statements: This type of engagement letter is formulated when an accounting firm is engaged to take information provided by the client and present it in the form of financial statements without providing any form of assurance on the information's accuracy. In conclusion, the Mecklenburg North Carolina Engagement Letter for Review of Financial Statements and Compilation by an Accounting Firm is a foundational document that outlines the terms, objectives, responsibilities, and limitations of an engagement. It ensures clear communication and mutual understanding between the accounting firm and the client, promoting a successful and efficient engagement process.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.