Generally, a contract to employ a certified public accountant need not be in writing. However, such contracts often call for services of a highly complex and technical nature, and hence they should be explicit in their terms, and they should be in writing. In particular, a written employment contract is necessary in order to avoid misunderstanding with the employer regarding the amount of the accountant's fee or compensation and the nature of its computation. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

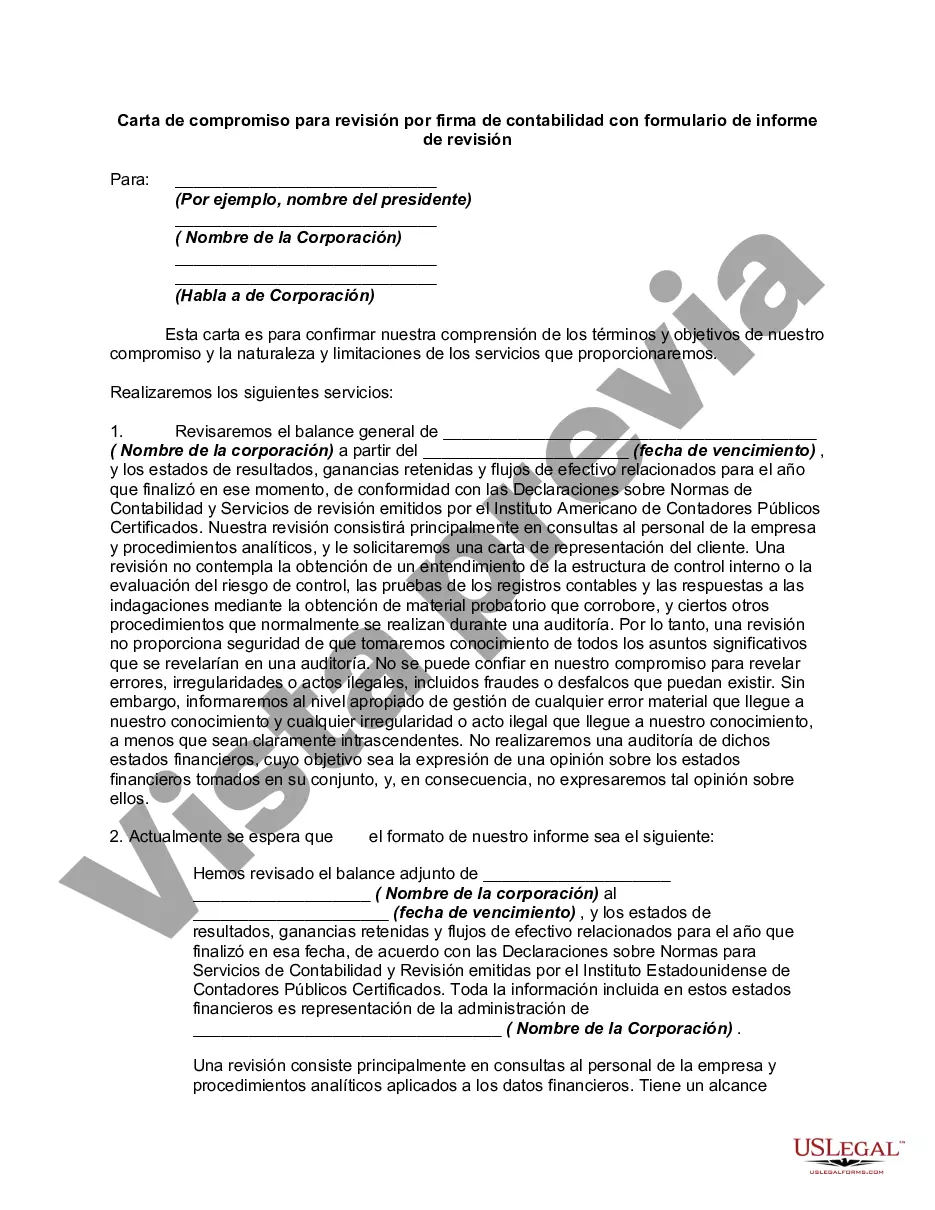

A Contra Costa California Engagement Letter for Review by an Accounting Firm with Form of Review Report is a crucial document that outlines the terms and conditions of the engagement between an accounting firm and its client for the purpose of review services. This letter is specifically designed to comply with the requirements of Contra Costa California and the applicable professional standards. The Contra Costa California Engagement Letter for Review serves as a formal agreement between the accounting firm and the client, ensuring a clear understanding of the scope, objectives, and responsibilities of both parties involved in the review process. By utilizing this letter, the accounting firm can establish a strong foundation for effective communication, minimize misunderstandings, and mitigate potential disputes. Typically, a Contra Costa California Engagement Letter for Review by Accounting Firm with Form of Review Report includes various sections to address multiple aspects of the engagement, such as: 1. Engagement Objectives: This section clarifies the intended purpose of the review engagement, whether it is to express limited assurance or no assurance regarding the financial statements. 2. Scope of the Engagement: This section outlines the specific areas to be addressed in the review, such as statements, schedules, or specific accounts. It also emphasizes the reliance on management's representations and confirms that the accounting firm will not perform an audit or express an opinion on the financial statements. 3. Responsibilities of the Accounting Firm: This section details the duties and responsibilities of the accounting firm while conducting the review, including the need to comply with professional standards and obtain sufficient appropriate review evidence. 4. Responsibilities of the Client: This section highlights the client's obligations, such as providing complete and accurate financial records, ensuring internal controls, and making management representations to the accounting firm. 5. Internal Control Considerations: This section may address the accounting firm's responsibilities for assessing and documenting the client's internal control over financial reporting in the context of the review engagement. 6. Timeline and Deliverables: This section specifies the expected completion date of the review engagement and the anticipated date for issuing the final review report. Forms of Review Reports: 1. Unmodified Review Report: This type of review report is issued when the accounting firm concludes that they have obtained sufficient appropriate review evidence and nothing has come to their attention that would indicate the financial statements need modification. It provides limited assurance that no material modifications are necessary for the financial statements to be in accordance with the applicable financial reporting framework. 2. Modified Review Report: This type of review report is issued when the accounting firm identifies material modifications that need to be made to the financial statements due to concerns or limitations encountered during the review. The report describes the nature and extent of the modifications required. 3. Adverse Review Report: In rare cases, an adverse review report may be issued if the accounting firm determines that the financial statements do not conform to the applicable financial reporting framework. This report conveys a lack of assurance on the financial statements' reliability. 4. Disclaimer of Opinion: In exceptional circumstances, the accounting firm may be unable to obtain sufficient appropriate review evidence, and therefore, is unable to express any opinion on the financial statements. This situation might arise due to severe limitations, such as the lack of necessary records or significant uncertainties. In summary, a Contra Costa California Engagement Letter for Review by an Accounting Firm with Form of Review Report is a vital document that establishes the terms of engagement and sets expectations for the review process. The different types of review reports reflect the outcome of the review and the accounting firm's level of assurance provided to the client regarding the financial statements.A Contra Costa California Engagement Letter for Review by an Accounting Firm with Form of Review Report is a crucial document that outlines the terms and conditions of the engagement between an accounting firm and its client for the purpose of review services. This letter is specifically designed to comply with the requirements of Contra Costa California and the applicable professional standards. The Contra Costa California Engagement Letter for Review serves as a formal agreement between the accounting firm and the client, ensuring a clear understanding of the scope, objectives, and responsibilities of both parties involved in the review process. By utilizing this letter, the accounting firm can establish a strong foundation for effective communication, minimize misunderstandings, and mitigate potential disputes. Typically, a Contra Costa California Engagement Letter for Review by Accounting Firm with Form of Review Report includes various sections to address multiple aspects of the engagement, such as: 1. Engagement Objectives: This section clarifies the intended purpose of the review engagement, whether it is to express limited assurance or no assurance regarding the financial statements. 2. Scope of the Engagement: This section outlines the specific areas to be addressed in the review, such as statements, schedules, or specific accounts. It also emphasizes the reliance on management's representations and confirms that the accounting firm will not perform an audit or express an opinion on the financial statements. 3. Responsibilities of the Accounting Firm: This section details the duties and responsibilities of the accounting firm while conducting the review, including the need to comply with professional standards and obtain sufficient appropriate review evidence. 4. Responsibilities of the Client: This section highlights the client's obligations, such as providing complete and accurate financial records, ensuring internal controls, and making management representations to the accounting firm. 5. Internal Control Considerations: This section may address the accounting firm's responsibilities for assessing and documenting the client's internal control over financial reporting in the context of the review engagement. 6. Timeline and Deliverables: This section specifies the expected completion date of the review engagement and the anticipated date for issuing the final review report. Forms of Review Reports: 1. Unmodified Review Report: This type of review report is issued when the accounting firm concludes that they have obtained sufficient appropriate review evidence and nothing has come to their attention that would indicate the financial statements need modification. It provides limited assurance that no material modifications are necessary for the financial statements to be in accordance with the applicable financial reporting framework. 2. Modified Review Report: This type of review report is issued when the accounting firm identifies material modifications that need to be made to the financial statements due to concerns or limitations encountered during the review. The report describes the nature and extent of the modifications required. 3. Adverse Review Report: In rare cases, an adverse review report may be issued if the accounting firm determines that the financial statements do not conform to the applicable financial reporting framework. This report conveys a lack of assurance on the financial statements' reliability. 4. Disclaimer of Opinion: In exceptional circumstances, the accounting firm may be unable to obtain sufficient appropriate review evidence, and therefore, is unable to express any opinion on the financial statements. This situation might arise due to severe limitations, such as the lack of necessary records or significant uncertainties. In summary, a Contra Costa California Engagement Letter for Review by an Accounting Firm with Form of Review Report is a vital document that establishes the terms of engagement and sets expectations for the review process. The different types of review reports reflect the outcome of the review and the accounting firm's level of assurance provided to the client regarding the financial statements.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.