A trustor is the person who creates a trust. A trustor is also called a grantor, donor or settlor. A trust is a separate legal entity that holds property or assets of some kind for the benefit of a specific person, group of people or organization known as the beneficiary/beneficiaries. When a trust is established, an individual or corporate entity is named to oversee or manage the assets in the trust. This individual or entity is called a trustee. A trustee can be a professional with financial knowledge, a relative or loyal friend or a corporation. More than one trustee can be named by the trustor.

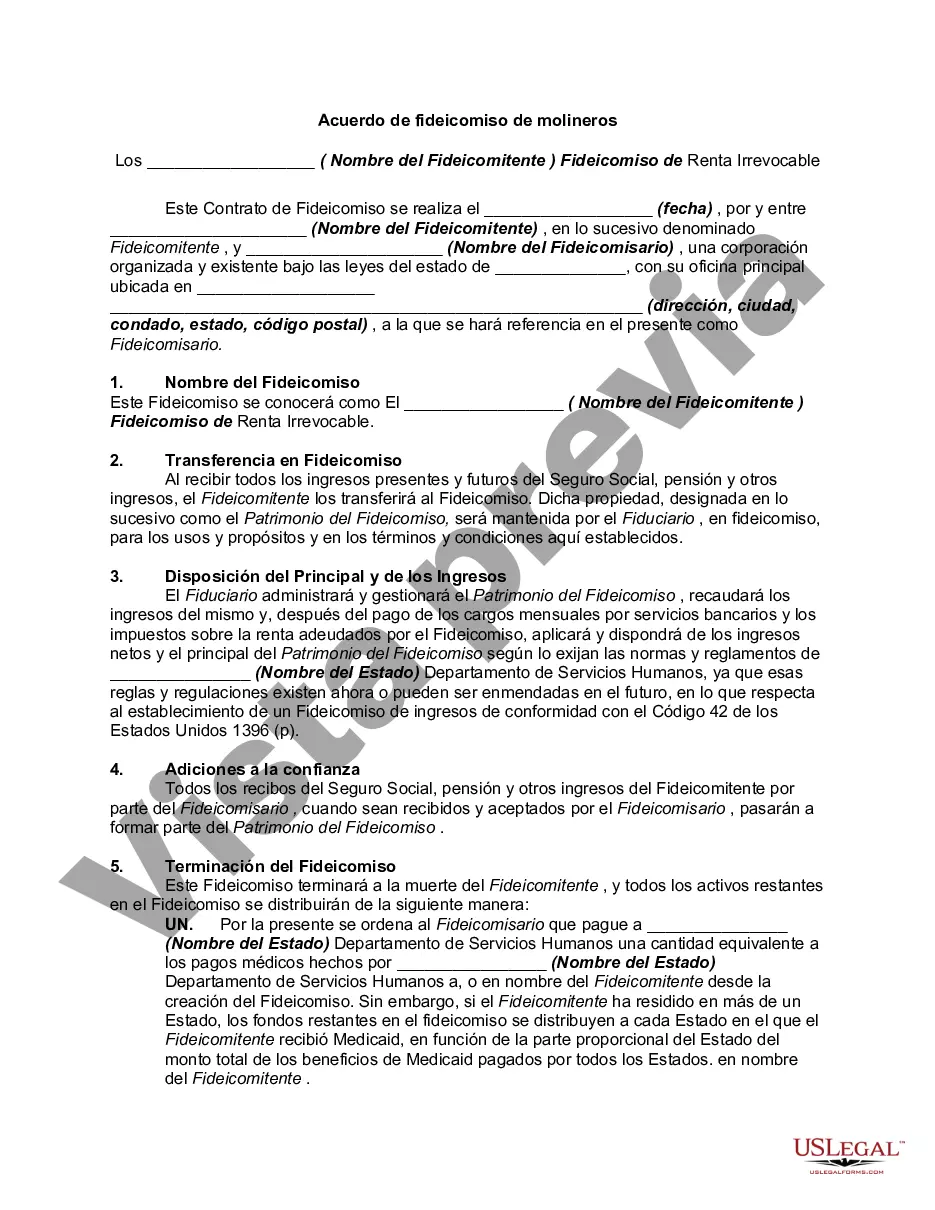

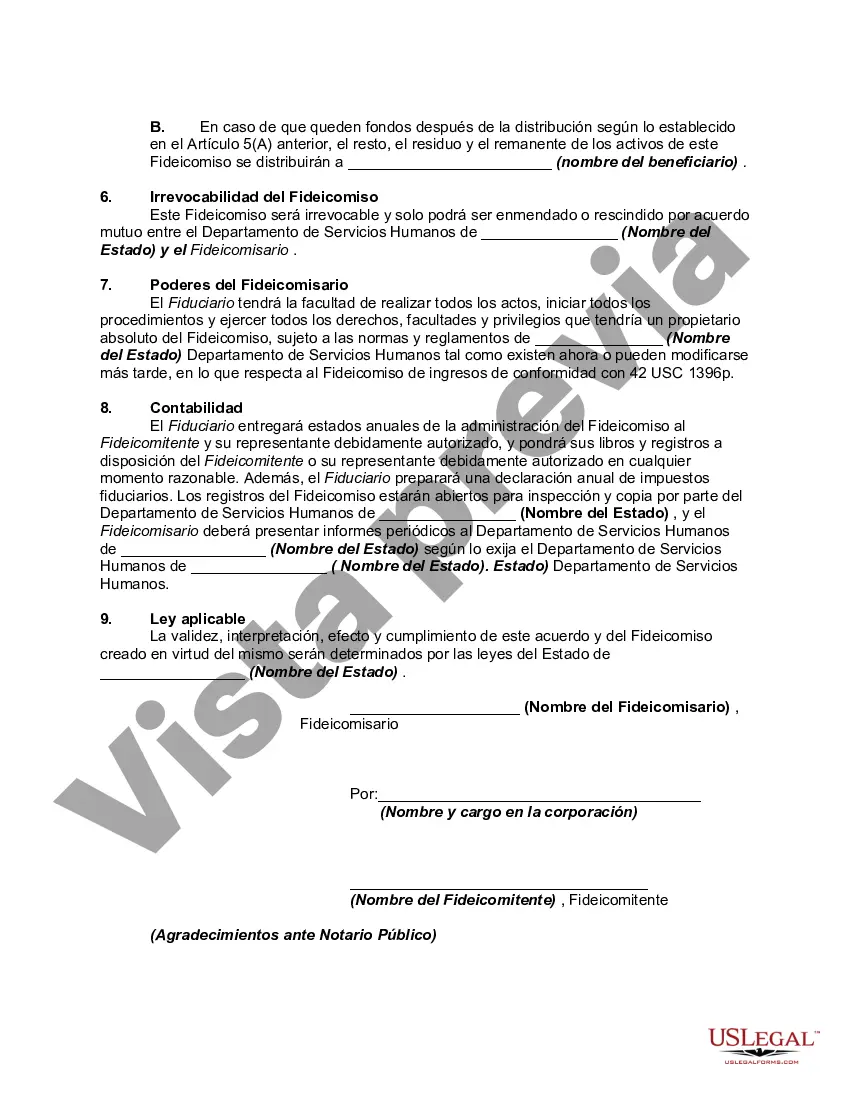

The qualified Medicaid income trust is a legal instrument which meets criteria in 42 United States Code 1396(p) and which allows individuals with income over the institutional care program limits to qualify for institutional care services or for home and community based services assistance.

A Medicaid trust may take various forms and laws vary by state. There are differing requirements under state laws regarding what assets may be counted or reached for recovery upon death. To comply with applicable requirements, professional financial advice should be sought. The term "Miller Trust" is an informal name. A more accurate name for this trust is an "Income Cap Trust". It has also been called an Income Assignment Trust. This is because, after the trust is created, the patient assigns his or her right to receive social security and pension to the trust.

The Franklin Ohio Qualified Income Miller Trust is a legal tool designed to help individuals meet the income requirements for Medicaid eligibility while protecting their assets. It is specifically aimed at individuals who have income that exceeds the threshold set by Medicaid. This type of trust is known as a Miller Trust or an income-only trust. It allows individuals to "spend down" their excess income by redirecting it into the trust, thereby reducing their overall income and helping them qualify for Medicaid benefits. The trust is named after the Miller v. Ibarra court case in which the concept was established. The Franklin Ohio Qualified Income Miller Trust is subject to specific rules and regulations set by the state of Ohio. It must be irrevocable, meaning it cannot be changed or revoked once it is established. The trust must be managed by a trustee, who can be either an individual or a professional entity authorized to act as a trustee. The trust's income is used solely for the benefit of the beneficiary and is typically directed towards paying for the beneficiary's medical expenses and personal needs. Medicaid eligibility is based on both income and asset limits, and by diverting excess income into the trust, individuals can meet the income requirements while protecting their assets. The Franklin Ohio Qualified Income Miller Trust can greatly benefit individuals who require long-term care but do not meet the income requirements for Medicaid. By strategically utilizing this trust, individuals can ensure that their healthcare needs are taken care of while preserving their hard-earned assets. Keywords: Franklin Ohio Qualified Income Miller Trust, Medicaid eligibility, asset protection, Miller trust, income-only trust, spend down excess income, irrevocable trust, trustee, Medicaid benefits, medical expenses, long-term care, healthcare needs.The Franklin Ohio Qualified Income Miller Trust is a legal tool designed to help individuals meet the income requirements for Medicaid eligibility while protecting their assets. It is specifically aimed at individuals who have income that exceeds the threshold set by Medicaid. This type of trust is known as a Miller Trust or an income-only trust. It allows individuals to "spend down" their excess income by redirecting it into the trust, thereby reducing their overall income and helping them qualify for Medicaid benefits. The trust is named after the Miller v. Ibarra court case in which the concept was established. The Franklin Ohio Qualified Income Miller Trust is subject to specific rules and regulations set by the state of Ohio. It must be irrevocable, meaning it cannot be changed or revoked once it is established. The trust must be managed by a trustee, who can be either an individual or a professional entity authorized to act as a trustee. The trust's income is used solely for the benefit of the beneficiary and is typically directed towards paying for the beneficiary's medical expenses and personal needs. Medicaid eligibility is based on both income and asset limits, and by diverting excess income into the trust, individuals can meet the income requirements while protecting their assets. The Franklin Ohio Qualified Income Miller Trust can greatly benefit individuals who require long-term care but do not meet the income requirements for Medicaid. By strategically utilizing this trust, individuals can ensure that their healthcare needs are taken care of while preserving their hard-earned assets. Keywords: Franklin Ohio Qualified Income Miller Trust, Medicaid eligibility, asset protection, Miller trust, income-only trust, spend down excess income, irrevocable trust, trustee, Medicaid benefits, medical expenses, long-term care, healthcare needs.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.