A number of states have enacted measures to facilitate greater communication between borrowers and lenders by requiring mortgage servicers to provide certain notices to defaulted borrowers prior to commencing a foreclosure action. The measures serve a dual purpose, providing more meaningful notice to borrowers of the status of their loans and slowing down the rate of foreclosures within these states. For instance, one state now requires a mortgagee to mail a homeowner a notice of intent to foreclose at least 45 days before initiating a foreclosure action on a loan. The notice must be in writing, and must detail all amounts that are past due and any itemized charges that must be paid to bring the loan current, inform the homeowner that he or she may have options as an alternative to foreclosure, and provide contact information of the servicer, HUD-approved foreclosure counseling agencies, and the state Office of Commissioner of Banks.

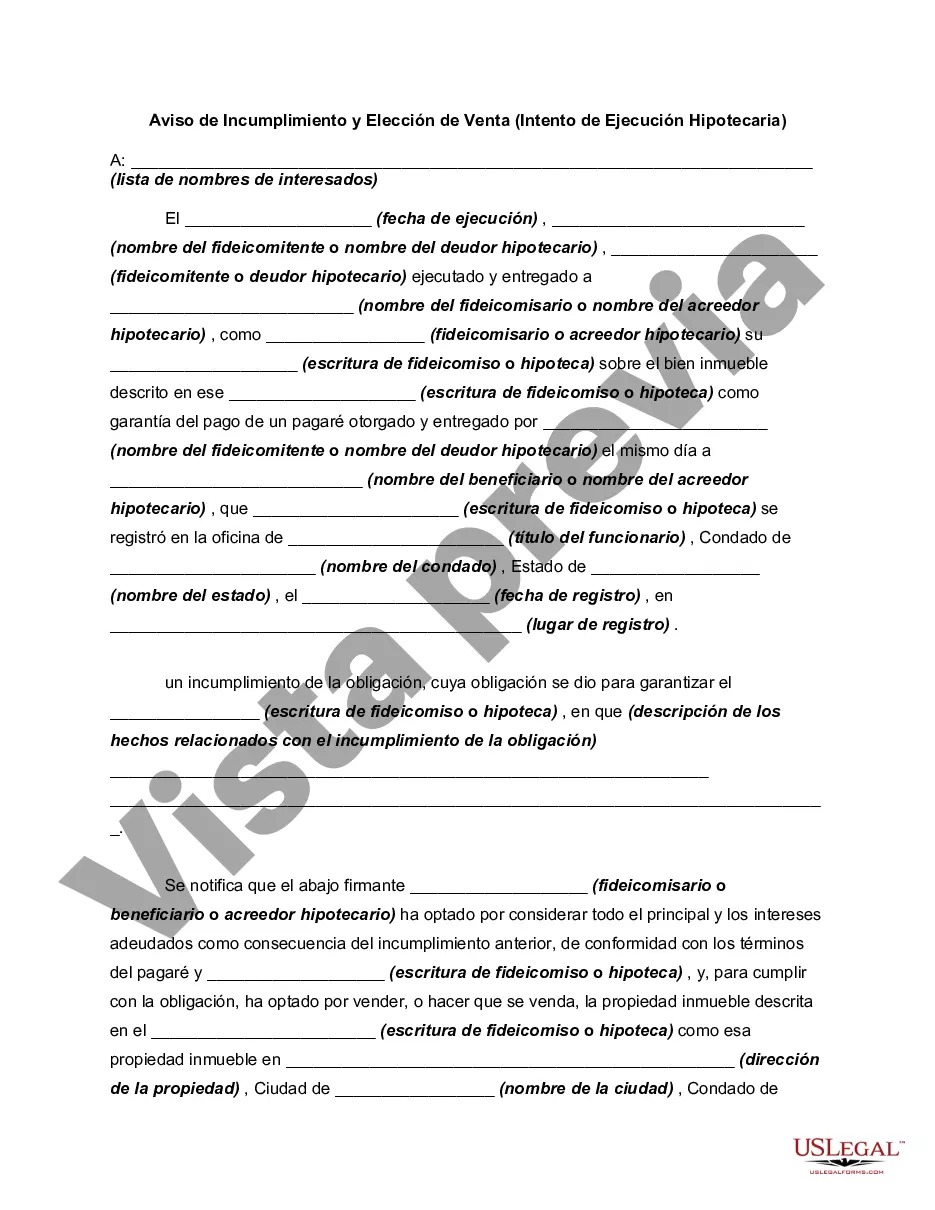

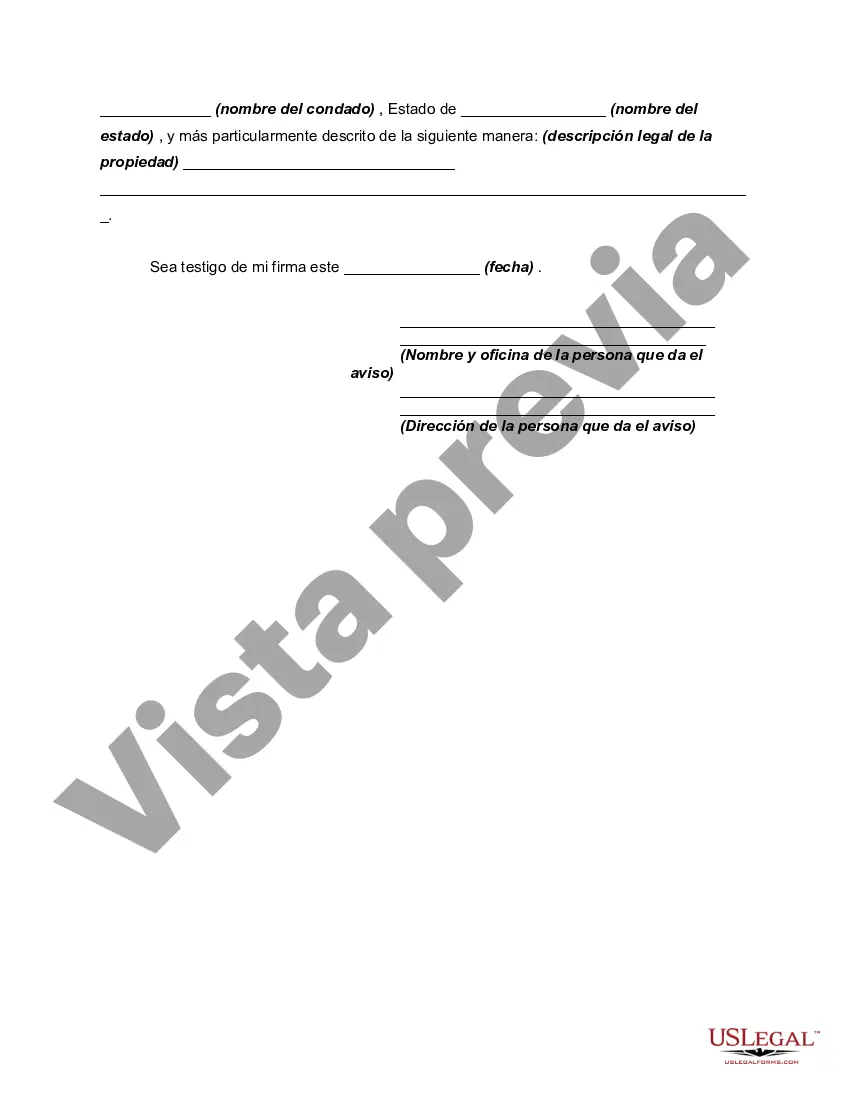

Hennepin County, Minnesota Notice of Default and Election to Sell — Intent To Foreclose is a legal document issued when a homeowner fails to make timely mortgage payments, indicating the initiation of foreclosure proceedings. This notice serves as a formal notification to the homeowner that they are in default of their mortgage agreement and that the lender intends to proceed with the foreclosure process. When a borrower defaults on their mortgage payments, the lender may file a Notice of Default with the Hennepin County Recorder's Office. This document includes key information, such as the borrower's name, property address, loan details, and the amount of unpaid mortgage payments. Additionally, it outlines the lender's intent to sell the property through a public auction to recover the outstanding debt. There are several types of Hennepin County Notice of Default and Election to Sell — Intent To Foreclose forms, each serving different purposes during the foreclosure process. These may include: 1. Pre-Foreclosure Notice of Default: This initial notice is sent to the borrower after they miss a certain number of mortgage payments, usually around three. It informs them of the delinquency and advises them to take immediate action to resolve the situation, often by catching up with the missed payments or seeking loan modification options. 2. Foreclosure Sale Notice: If the borrower fails to address the delinquency or find a suitable resolution, the lender may proceed with a foreclosure sale. This notice includes the date, time, and location of the public auction where the property will be sold to the highest bidder. 3. Notice of Postponement: In some cases, a foreclosure sale may be postponed due to various reasons, such as borrower request, legal complications, or negotiations for a loan modification. The Notice of Postponement informs interested parties about the updated date and time of the postponed sale. 4. Notice of Rescission: If the borrower successfully resolves the default, either by catching up on missed payments or negotiating a loan modification with the lender, a Notice of Rescission is filed. This document cancels the foreclosure proceedings, giving the homeowner a chance to maintain ownership of the property. It is important for borrowers who receive a Hennepin County Notice of Default and Election to Sell — Intent To Foreclose to take swift action to prevent the foreclosure process from proceeding. Seeking legal counsel, exploring loan modification options, or addressing the delinquency by catching up on missed payments may offer solutions to avoid losing their property.Hennepin County, Minnesota Notice of Default and Election to Sell — Intent To Foreclose is a legal document issued when a homeowner fails to make timely mortgage payments, indicating the initiation of foreclosure proceedings. This notice serves as a formal notification to the homeowner that they are in default of their mortgage agreement and that the lender intends to proceed with the foreclosure process. When a borrower defaults on their mortgage payments, the lender may file a Notice of Default with the Hennepin County Recorder's Office. This document includes key information, such as the borrower's name, property address, loan details, and the amount of unpaid mortgage payments. Additionally, it outlines the lender's intent to sell the property through a public auction to recover the outstanding debt. There are several types of Hennepin County Notice of Default and Election to Sell — Intent To Foreclose forms, each serving different purposes during the foreclosure process. These may include: 1. Pre-Foreclosure Notice of Default: This initial notice is sent to the borrower after they miss a certain number of mortgage payments, usually around three. It informs them of the delinquency and advises them to take immediate action to resolve the situation, often by catching up with the missed payments or seeking loan modification options. 2. Foreclosure Sale Notice: If the borrower fails to address the delinquency or find a suitable resolution, the lender may proceed with a foreclosure sale. This notice includes the date, time, and location of the public auction where the property will be sold to the highest bidder. 3. Notice of Postponement: In some cases, a foreclosure sale may be postponed due to various reasons, such as borrower request, legal complications, or negotiations for a loan modification. The Notice of Postponement informs interested parties about the updated date and time of the postponed sale. 4. Notice of Rescission: If the borrower successfully resolves the default, either by catching up on missed payments or negotiating a loan modification with the lender, a Notice of Rescission is filed. This document cancels the foreclosure proceedings, giving the homeowner a chance to maintain ownership of the property. It is important for borrowers who receive a Hennepin County Notice of Default and Election to Sell — Intent To Foreclose to take swift action to prevent the foreclosure process from proceeding. Seeking legal counsel, exploring loan modification options, or addressing the delinquency by catching up on missed payments may offer solutions to avoid losing their property.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.