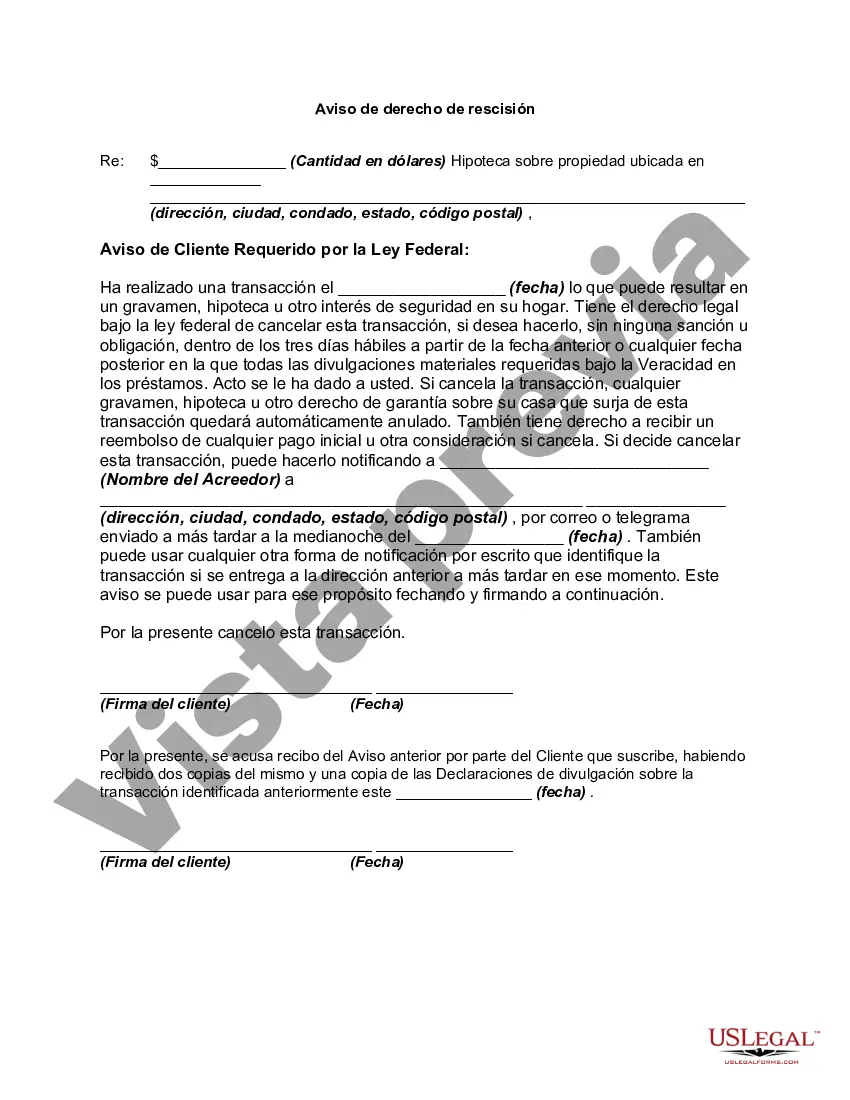

In a credit transaction in which a security interest is or will be retained or acquired in a consumer's principal dwelling, each consumer whose ownership is or will be subject to the security interest has the right to rescind the transaction. Lenders are required to deliver two copies of the notice of the right to rescind and one copy of the disclosure statement to each consumer entitled to rescind. The notice must be on a separate document that identifies the rescission period on the transaction and must clearly and conspicuously:

" disclose the retention or acquisition of a security interest in the consumer's principal dwelling;

" the consumer's right to rescind the transaction; and

" how the consumer may exercise the right to rescind with a form for that purpose.

King Washington right to rescind when security interest in consumer's principal dwelling is involved — Rescission refers to a legal provision that grants consumers the right to cancel a mortgage or home equity loan when it is secured by their primary residence. This right acts as a safeguard for homeowners, protecting their interests against unfair lending practices. When a consumer has a security interest in their principal dwelling, they have the right to rescind or cancel the loan within a specific timeframe, typically three business days, after the loan documents are signed. This means that if the consumer feels coerced, deceived, or finds the loan terms unsatisfactory, they can legally void the contract and walk away from the loan agreement without penalty. The King Washington act recognizes various types of situations where the right to rescind becomes applicable: 1. Predatory lending practices: Consumers are protected against predatory lending, which includes fraudulent schemes, high-pressure tactics, or improper disclosures intended to deceive or take advantage of vulnerable homeowners. 2. Incorrect or incomplete disclosures: If the lender fails to provide the required disclosures regarding loan terms, costs, or risks involved, the consumer retains the right to rescind the loan. 3. Violations of Truth in Lending Act (TILL): TILL mandates lenders to accurately disclose loan terms, including interest rates, fees, and repayment schedules. Any violation of TILL provisions can trigger the right to rescission. 4. Material changes in loan terms: Should the lender make any material changes to the loan terms after the initial agreement, the consumer can exercise their right to rescind the loan. 5. Failure to provide the notice of the right to rescind: If the lender fails to provide the consumer with the mandatory notice outlining their right to rescind, the consumer's rescission period can be extended up to three years from the transaction's completion. It is essential for consumers to be aware of the King Washington right to rescind when a security interest in their principal dwelling is involved. This provision aims to promote fair lending practices, protecting homeowners from abusive or misleading loan agreements. By understanding their rights, consumers can make informed decisions regarding their loans, ensuring they receive fair treatment and avoid potential financial risks.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.