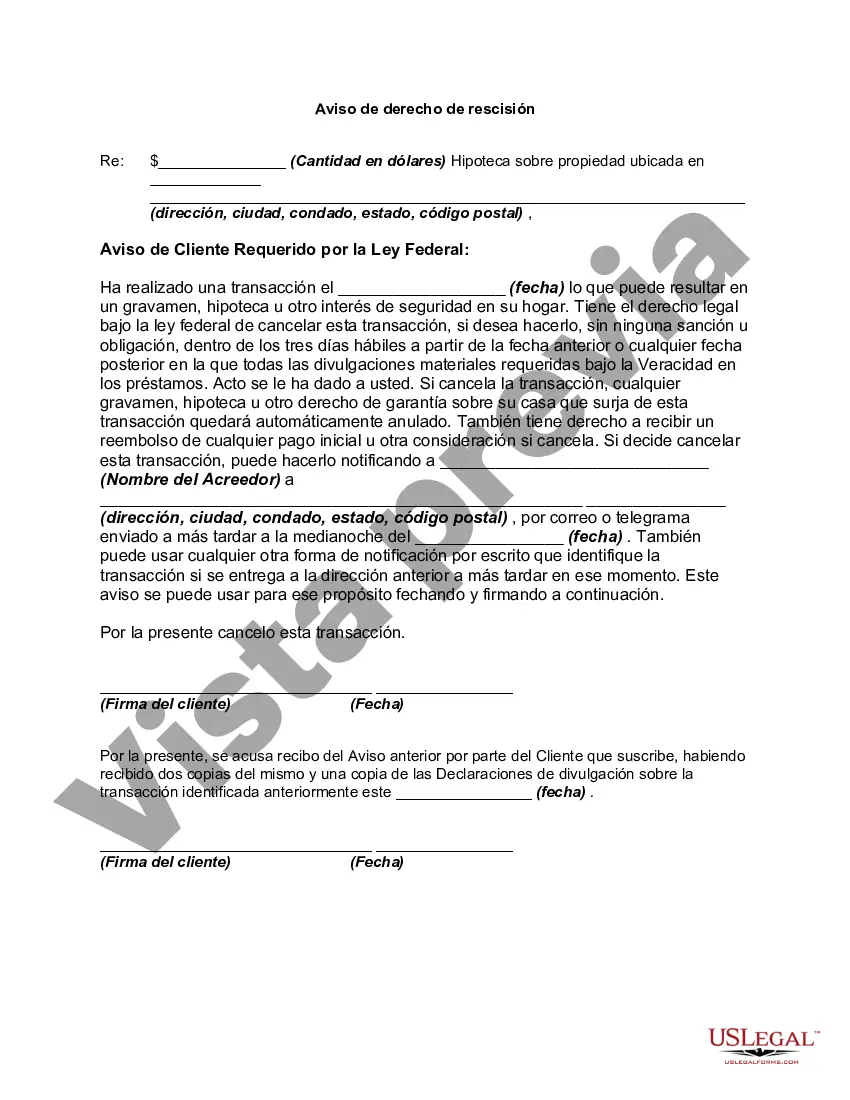

In a credit transaction in which a security interest is or will be retained or acquired in a consumer's principal dwelling, each consumer whose ownership is or will be subject to the security interest has the right to rescind the transaction. Lenders are required to deliver two copies of the notice of the right to rescind and one copy of the disclosure statement to each consumer entitled to rescind. The notice must be on a separate document that identifies the rescission period on the transaction and must clearly and conspicuously:

" disclose the retention or acquisition of a security interest in the consumer's principal dwelling;

" the consumer's right to rescind the transaction; and

" how the consumer may exercise the right to rescind with a form for that purpose.

Mecklenburg North Carolina Right to Rescind When Security Interest in Consumer's Principal Dwelling is Involved — Rescission In Mecklenburg County, North Carolina, the right to rescind comes into play when a security interest in a consumer's principal dwelling is involved. Rescission is a legal remedy that allows the borrower to cancel or annul a mortgage loan, home equity loan, or refinance transaction that uses their principal dwelling as collateral. It is designed to protect consumers from potentially unfair lending practices and provide them with an opportunity to reconsider their financial decisions. The Right to Rescind is governed by the Truth in Lending Act (TILL) and its regulations, which applies to various types of consumer credit transactions. When a consumer enters into a loan agreement where their primary residence is pledged as security, they typically have three business days to exercise their right to rescind. This period allows them to carefully review the terms and conditions of the loan and seek professional advice if needed. During the rescission period, the consumer can simply communicate their intent to cancel the loan in writing or by any other means permissible by law. Upon such rescission, the lender is legally obligated to unwind the transaction, release the security interest in the consumer's dwelling, and return any money or property that the consumer has paid or given as part of the loan agreement. It is important to note that the right to rescind does not apply in all situations. Certain types of transactions are exempt, such as loans used to purchase or build the consumer's principal dwelling. Additionally, if the borrower's principal dwelling is not involved or used as collateral, the right to rescind may not be applicable. Different types of Mecklenburg North Carolina Right to Rescind when security interest in consumer's principal dwelling is involved — rescission: 1. Mortgage Loan Rescission: If a borrower secures their mortgage loan with their principal dwelling as collateral in Mecklenburg County, they have the right to rescind within three business days of signing the loan agreement. 2. Home Equity Loan Rescission: Similar to a mortgage loan, consumers have the right to rescind a home equity loan if their principal dwelling is used as collateral. They have three business days to exercise this right in Mecklenburg County. 3. Refinance Transaction Rescission: When consumers opt to refinance their existing loan while pledging their principal dwelling as security, the right to rescind is applicable. They have three business days to reconsider and cancel the refinancing transaction, ensuring the protection of their rights in Mecklenburg County. In summary, Mecklenburg North Carolina provides consumers with a vital right to rescind when a security interest in their principal dwelling is involved. This legal safeguard allows borrowers to review loan terms, seek advice, and cancel certain types of transactions within a specific time frame. By exercising the right to rescind, consumers can protect themselves from potential unfair lending practices and make informed financial decisions.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.