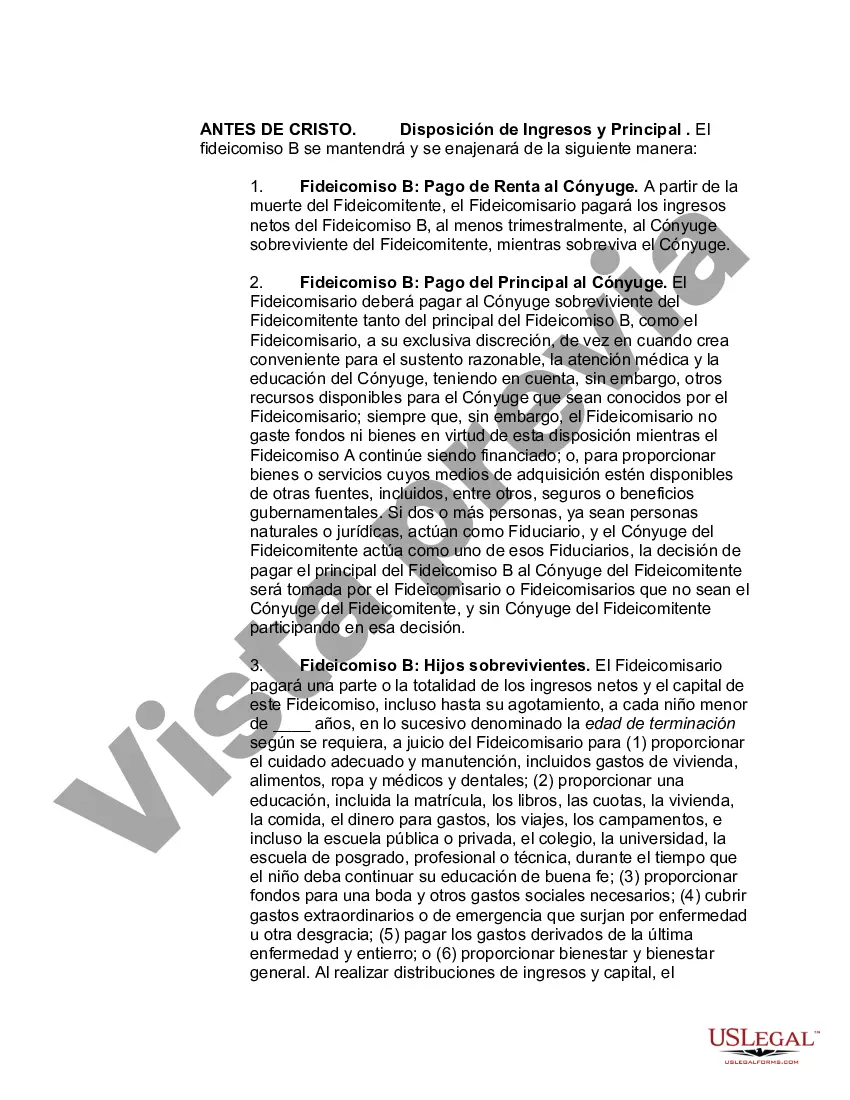

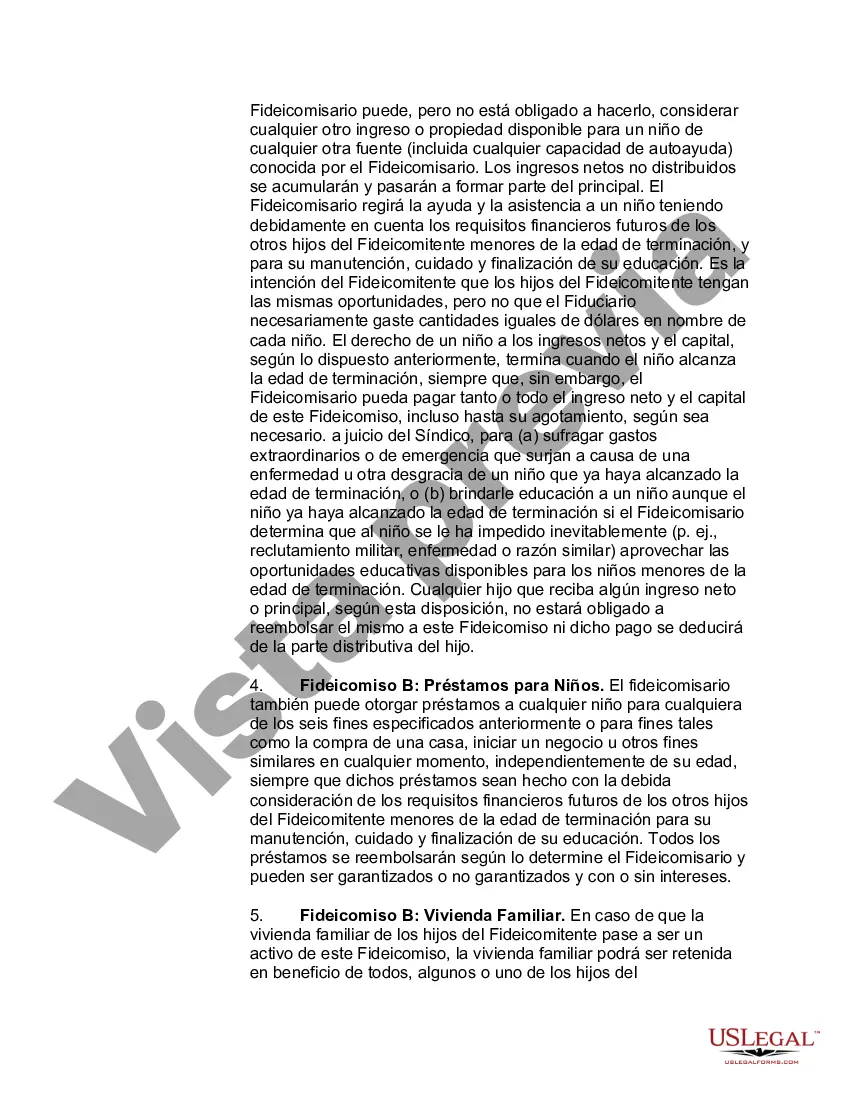

An A-B trust is a revocable living trust which divides into two trusts upon the death of the first spouse. This type of trust makes use of both the estate tax exemption ($3.5 million per person in 2009) and the marital deduction to make it so that no estate taxes are due upon the death of the first spouse. The B Trust is also known as the Bypass trust and it contains the amount of that years applicable exclusion amount. The A trust is the marital deduction trust which will typically contain both the surviving spouse's separate property and one half community property interests but also the residue of the deceased spouse's estate after the estate tax exemption has been utilized by the B trust. The use of an A-B trust ensures that both spouse's applicable exclusion amounts are effectively used, thereby doubling the amount of property which can pass to heirs free of Federal Estate Taxes.

A Chicago Illinois Marital Deduction Trust, also known as Trust A, is a legal arrangement that allows a married couple to maximize the value of their estate and reduce estate taxes upon the death of one spouse. This trust is created to take full advantage of the marital deduction provision in the federal estate tax laws. Trust A, also referred to as the "Marital Trust" or "A Trust," is usually funded with assets equal to or less than the federal estate tax exemption amount. Upon the death of the first spouse, the assets in Trust A are transferred to the surviving spouse, who becomes the sole beneficiary of the trust. The surviving spouse can withdraw income generated by the trust assets and also has limited access to the principal, if necessary. The primary purpose of Trust A is to provide the surviving spouse with financial support while still preserving the assets for future generations. Since assets transferred to Trust A are not included in the surviving spouse's estate, they are protected from estate taxes until the death of the surviving spouse. On the other hand, the Bypass Trust, also known as Trust B, is set up to utilize the estate tax exemption of the first spouse to die. This trust is funded with assets equal to or less than the federal estate tax exemption amount, together with any remaining amount after funding Trust A. Upon the death of the first spouse, assets in Trust B are not included in the surviving spouse's estate for estate tax purposes. Instead, they are passed directly to the designated beneficiaries, typically the children or other family members. The surviving spouse may receive income generated by the trust assets, but does not have access to the principal unless the trust permits it under specific circumstances. The primary goal of Trust B is to prevent the estate tax exemption of the first spouse to die from being wasted. By fully utilizing this exemption, couples can effectively reduce their potential estate tax liability and preserve wealth for future generations. In summary, a Chicago Illinois Marital Deduction Trust consists of Trust A (Marital Trust) and Trust B (Bypass Trust). Trust A provides financial support for the surviving spouse while preserving assets, and Trust B maximizes estate tax exemptions. These trusts work together to minimize estate taxes and ensure the smooth transfer of assets from one generation to the next.A Chicago Illinois Marital Deduction Trust, also known as Trust A, is a legal arrangement that allows a married couple to maximize the value of their estate and reduce estate taxes upon the death of one spouse. This trust is created to take full advantage of the marital deduction provision in the federal estate tax laws. Trust A, also referred to as the "Marital Trust" or "A Trust," is usually funded with assets equal to or less than the federal estate tax exemption amount. Upon the death of the first spouse, the assets in Trust A are transferred to the surviving spouse, who becomes the sole beneficiary of the trust. The surviving spouse can withdraw income generated by the trust assets and also has limited access to the principal, if necessary. The primary purpose of Trust A is to provide the surviving spouse with financial support while still preserving the assets for future generations. Since assets transferred to Trust A are not included in the surviving spouse's estate, they are protected from estate taxes until the death of the surviving spouse. On the other hand, the Bypass Trust, also known as Trust B, is set up to utilize the estate tax exemption of the first spouse to die. This trust is funded with assets equal to or less than the federal estate tax exemption amount, together with any remaining amount after funding Trust A. Upon the death of the first spouse, assets in Trust B are not included in the surviving spouse's estate for estate tax purposes. Instead, they are passed directly to the designated beneficiaries, typically the children or other family members. The surviving spouse may receive income generated by the trust assets, but does not have access to the principal unless the trust permits it under specific circumstances. The primary goal of Trust B is to prevent the estate tax exemption of the first spouse to die from being wasted. By fully utilizing this exemption, couples can effectively reduce their potential estate tax liability and preserve wealth for future generations. In summary, a Chicago Illinois Marital Deduction Trust consists of Trust A (Marital Trust) and Trust B (Bypass Trust). Trust A provides financial support for the surviving spouse while preserving assets, and Trust B maximizes estate tax exemptions. These trusts work together to minimize estate taxes and ensure the smooth transfer of assets from one generation to the next.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.