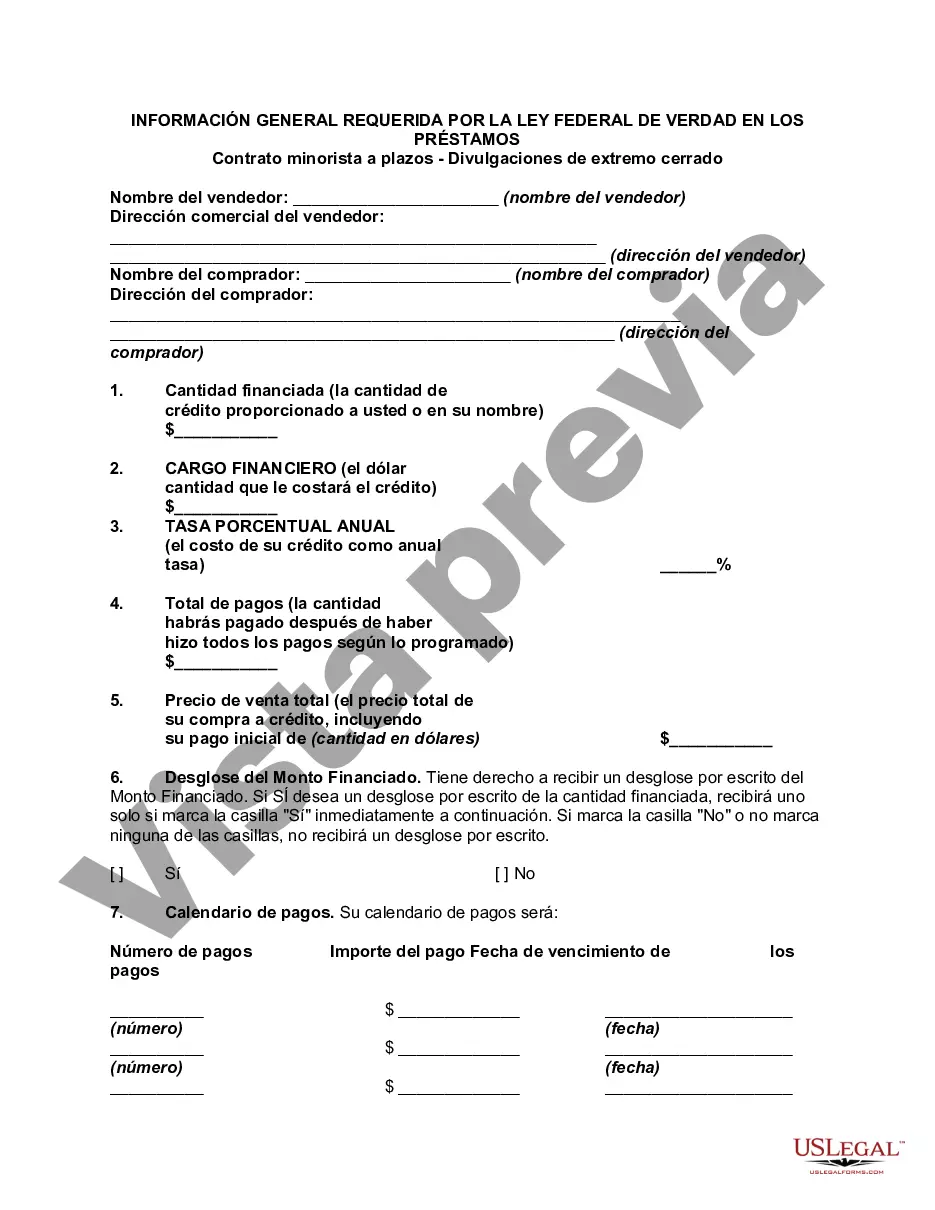

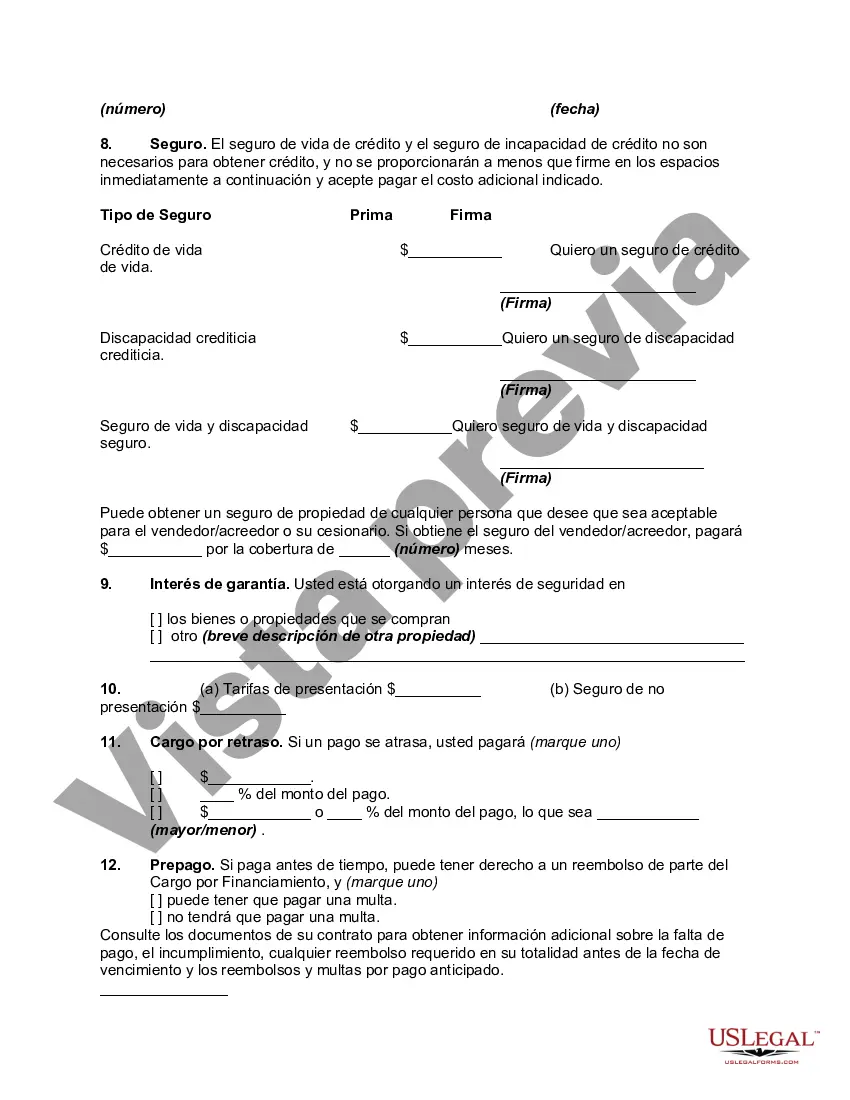

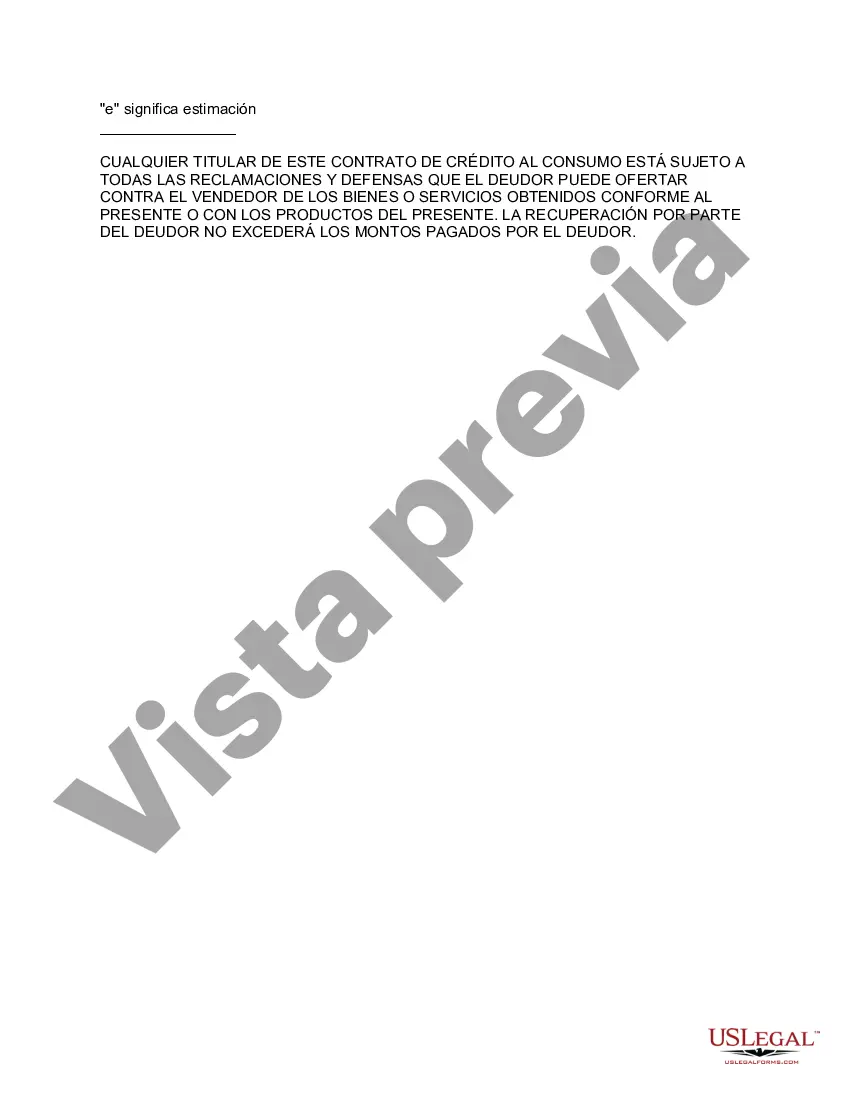

Los Angeles, California is a vibrant city located on the West Coast of the United States. It is the largest city in California and the second-largest city in the whole country. Known for its iconic landmarks, diverse culture, and thriving entertainment industry, Los Angeles attracts millions of visitors every year. When it comes to the General Disclosures required by the Federal Truth in Lending Act (TILL) — Retail InstallmenContractac— - Closed End Disclosures in Los Angeles, California, there are several aspects to consider. These disclosures aim to ensure transparency and fairness in consumer lending practices. Here are some important key points to note: 1. Annual Percentage Rate (APR): The APR is a crucial disclosure under the TILL. It represents the cost of credit on a yearly basis, including both the interest rate and any additional fees charged by the lender. Consumers must be provided with a clear and accurate APR calculation for their retail installment contracts. 2. Finance Charges: Alongside the APR, the finance charges must be disclosed. These charges generally include interest payments, loan fees, and any other fees associated with the loan. This disclosure helps borrowers understand the total cost of credit and make informed decisions. 3. Amount Financed: The amount financed refers to the total loan amount minus any prepaid finance charges. It indicates the actual principal amount that consumers borrow. This disclosure provides clarity on the funds received by the borrower. 4. Total Sale Price: The total sale price reveals the overall cost of the purchased item or service, including the financed amount, interest charges, and any other fees involved. This disclosure helps borrowers understand the total cost they will be responsible for. 5. Payment Schedule: The retail installment contract should include a detailed payment schedule, outlining the number of payments, amount due for each installment, and the due dates. This information helps borrowers plan their finances and ensure timely payments. 6. Prepayment Penalty: If applicable, any fees or penalties for early loan repayment must be disclosed to borrowers. This disclosure ensures that borrowers are aware of any potential costs if they choose to pay off the loan ahead of schedule. These are just a few key examples of the General Disclosures required by the Federal Truth in Lending Act — Retail InstallmenContractac— - Closed End Disclosures in Los Angeles, California. It is essential for lenders to provide accurate and transparent information to consumers to protect their rights and prevent any unfair practices.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Los Angeles California Divulgaciones generales requeridas por la Ley Federal de Veracidad en los Préstamos - Contrato minorista a plazos - Divulgaciones cerradas - General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures

Description

How to fill out Los Angeles California Divulgaciones Generales Requeridas Por La Ley Federal De Veracidad En Los Préstamos - Contrato Minorista A Plazos - Divulgaciones Cerradas?

Laws and regulations in every area vary throughout the country. If you're not a lawyer, it's easy to get lost in a variety of norms when it comes to drafting legal documentation. To avoid costly legal assistance when preparing the Los Angeles General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures, you need a verified template legitimate for your region. That's when using the US Legal Forms platform is so beneficial.

US Legal Forms is a trusted by millions web catalog of more than 85,000 state-specific legal forms. It's a perfect solution for professionals and individuals looking for do-it-yourself templates for various life and business situations. All the documents can be used multiple times: once you pick a sample, it remains accessible in your profile for subsequent use. Therefore, when you have an account with a valid subscription, you can just log in and re-download the Los Angeles General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures from the My Forms tab.

For new users, it's necessary to make a couple of more steps to get the Los Angeles General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures:

- Analyze the page content to ensure you found the appropriate sample.

- Utilize the Preview option or read the form description if available.

- Search for another doc if there are inconsistencies with any of your requirements.

- Click on the Buy Now button to get the template once you find the appropriate one.

- Opt for one of the subscription plans and log in or sign up for an account.

- Decide how you prefer to pay for your subscription (with a credit card or PayPal).

- Select the format you want to save the file in and click Download.

- Complete and sign the template in writing after printing it or do it all electronically.

That's the easiest and most affordable way to get up-to-date templates for any legal purposes. Find them all in clicks and keep your documentation in order with the US Legal Forms!