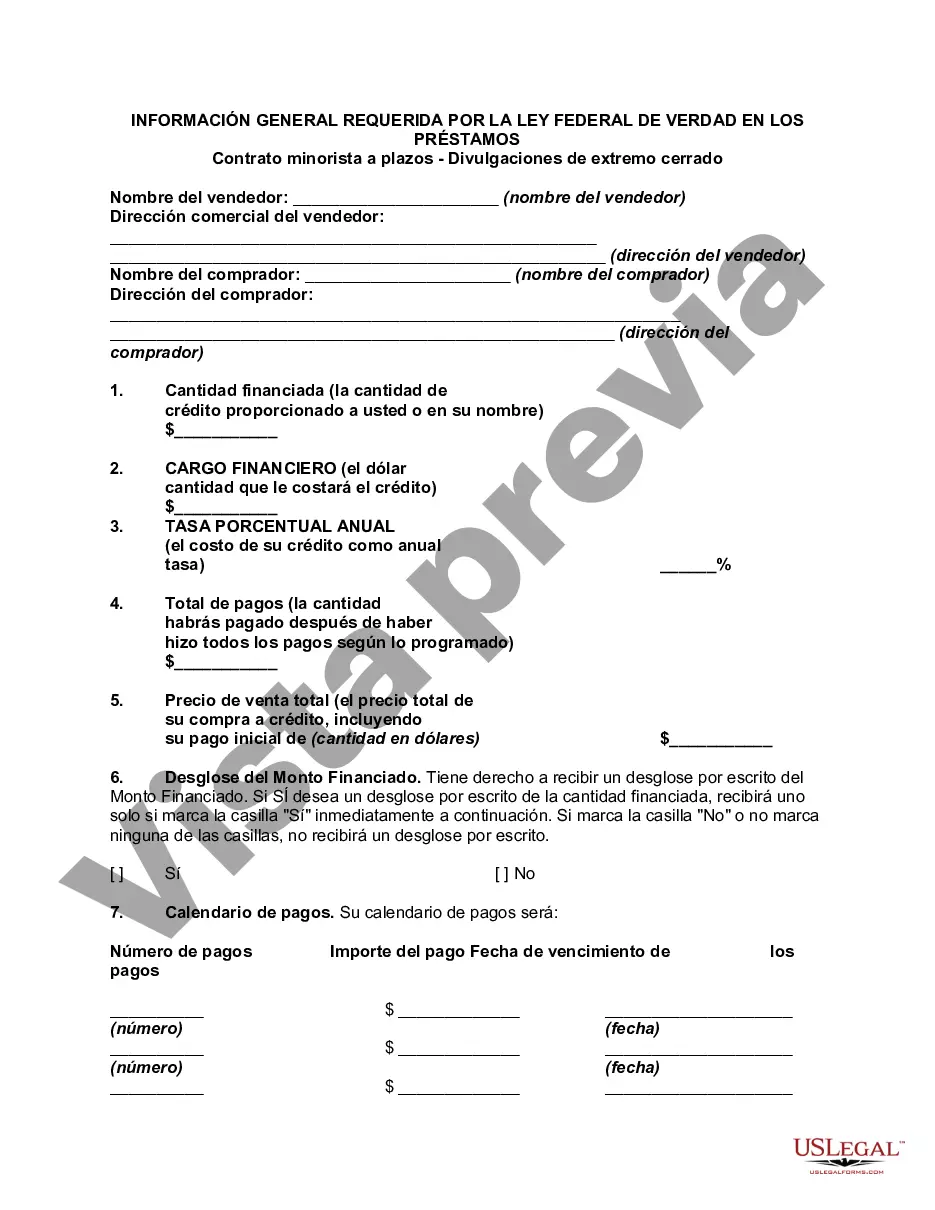

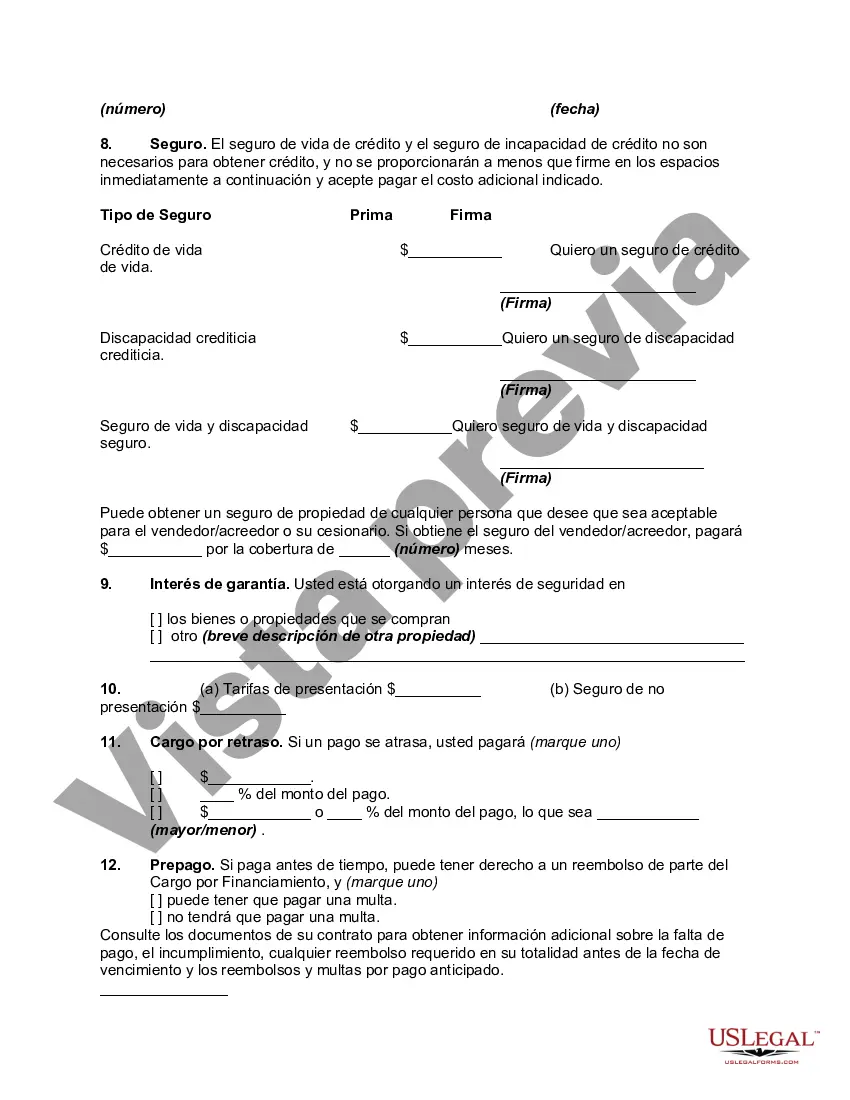

Miami-Dade, located in Florida, is subject to the General Disclosures Required By The Federal Truth In Lending Act for Retail Installment Contracts — Closed End Disclosures. These disclosures are aimed at providing clear information and ensuring fairness and transparency in consumer lending practices. The Federal Truth in Lending Act applies to various types of loans, including retail installment contracts, mortgages, and credit cards, among others. Under the General Disclosures required by the Federal Truth In Lending Act in Miami-Dade, several key aspects are covered to protect consumers. These include: 1. Annual Percentage Rate (APR): The APR represents the cost of credit on a yearly basis. Lenders must disclose the APR to help consumers compare different loan offers accurately. It includes the interest rate, finance charges, and other fees associated with the loan. 2. Finance Charges: Lenders must disclose the total finance charges, which include interest charges, application fees, origination fees, and any other charges imposed on the loan. 3. Amount Financed: This disclosure indicates the net amount the consumer will receive after deducting fees, prepaid finance charges, and other applicable charges from the loan amount. 4. Total Amount of Payments: This includes the sum of all payments required over the life of the loan, including principal and interest. 5. Payment Schedule: The disclosure must outline the timing, frequency, and number of payments expected from the borrower. 6. Repayment Terms: Borrowers should be aware of any penalties, late fees, or non-payment consequences that may apply. These terms must be clearly stated in the disclosures. 7. Right of Rescission: Certain loans, like home equity lines of credit (HELOT), provide borrowers with a right of rescission, allowing them to cancel the loan within a specified period without facing penalties or fees. This right should be disclosed if applicable. By providing these General Disclosures, the Federal Truth in Lending Act ensures that consumers in Miami-Dade have access to clear, concise, and comparable information when obtaining a loan. It aims to protect individuals from unfair lending practices and empower them to make informed financial decisions. Different types of loans may have specific variations in the required disclosures or additional requirements. For instance, mortgage loans have additional disclosures, such as the estimated total monthly payment, information about escrow accounts for taxes and insurance, and an itemization of closing costs. Credit card disclosures include the annual fee, interest rate calculation methods, minimum payments, and penalty fees, among others. It's crucial for lenders in Miami-Dade to abide by these General Disclosures and ensure compliance with the Federal Truth in Lending Act. By adhering to these regulations, they uphold the principles of fair lending, consumer protection, and transparency in the financial services industry.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Miami-Dade Florida Divulgaciones generales requeridas por la Ley Federal de Veracidad en los Préstamos - Contrato minorista a plazos - Divulgaciones cerradas - General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures

State:

Multi-State

County:

Miami-Dade

Control #:

US-02514BG

Format:

Word

Instant download

Description

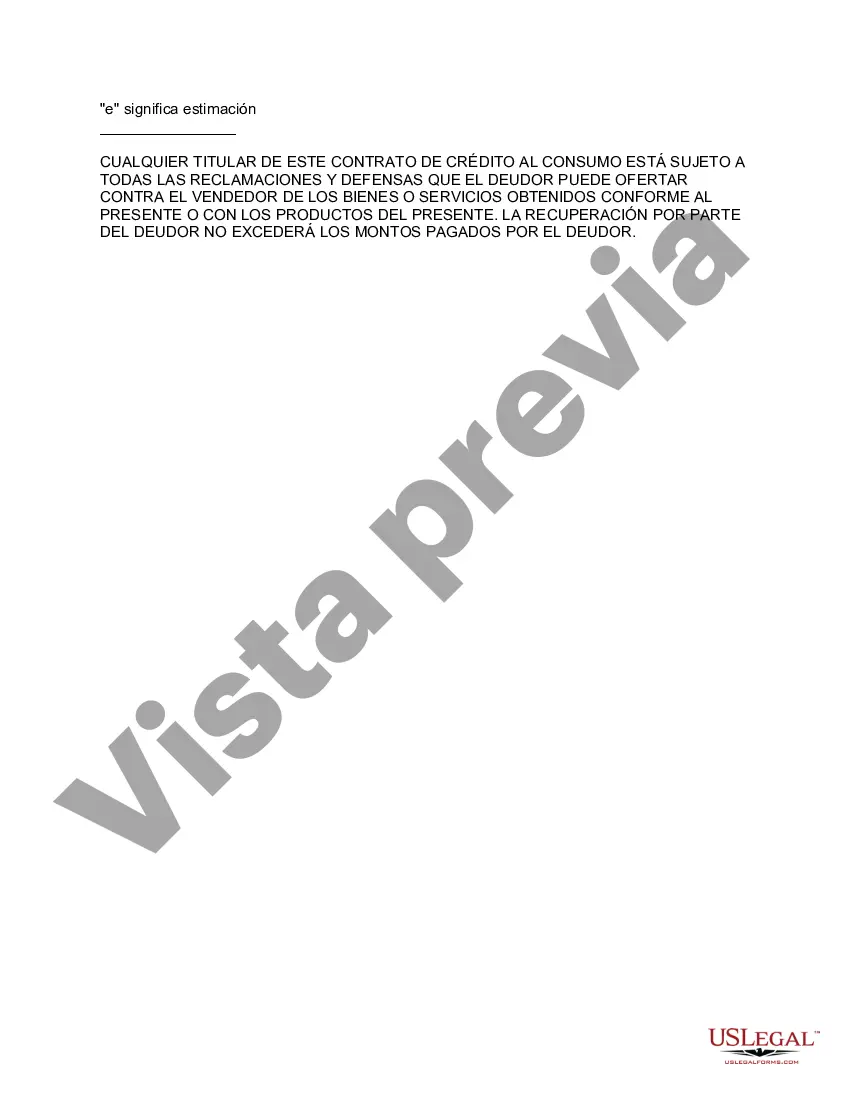

The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. The Act merely asks lenders to be honest to the debtors and not cover up what they are paying for the credit. Regulation Z is a federal regulation prepared by the Federal Reserve Board to carry out the details of the Act. TILA applies to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use.

Closed-end transactions involve a fixed amount to be paid back over a period of time such as a note or a retail installment contract.

Miami-Dade, located in Florida, is subject to the General Disclosures Required By The Federal Truth In Lending Act for Retail Installment Contracts — Closed End Disclosures. These disclosures are aimed at providing clear information and ensuring fairness and transparency in consumer lending practices. The Federal Truth in Lending Act applies to various types of loans, including retail installment contracts, mortgages, and credit cards, among others. Under the General Disclosures required by the Federal Truth In Lending Act in Miami-Dade, several key aspects are covered to protect consumers. These include: 1. Annual Percentage Rate (APR): The APR represents the cost of credit on a yearly basis. Lenders must disclose the APR to help consumers compare different loan offers accurately. It includes the interest rate, finance charges, and other fees associated with the loan. 2. Finance Charges: Lenders must disclose the total finance charges, which include interest charges, application fees, origination fees, and any other charges imposed on the loan. 3. Amount Financed: This disclosure indicates the net amount the consumer will receive after deducting fees, prepaid finance charges, and other applicable charges from the loan amount. 4. Total Amount of Payments: This includes the sum of all payments required over the life of the loan, including principal and interest. 5. Payment Schedule: The disclosure must outline the timing, frequency, and number of payments expected from the borrower. 6. Repayment Terms: Borrowers should be aware of any penalties, late fees, or non-payment consequences that may apply. These terms must be clearly stated in the disclosures. 7. Right of Rescission: Certain loans, like home equity lines of credit (HELOT), provide borrowers with a right of rescission, allowing them to cancel the loan within a specified period without facing penalties or fees. This right should be disclosed if applicable. By providing these General Disclosures, the Federal Truth in Lending Act ensures that consumers in Miami-Dade have access to clear, concise, and comparable information when obtaining a loan. It aims to protect individuals from unfair lending practices and empower them to make informed financial decisions. Different types of loans may have specific variations in the required disclosures or additional requirements. For instance, mortgage loans have additional disclosures, such as the estimated total monthly payment, information about escrow accounts for taxes and insurance, and an itemization of closing costs. Credit card disclosures include the annual fee, interest rate calculation methods, minimum payments, and penalty fees, among others. It's crucial for lenders in Miami-Dade to abide by these General Disclosures and ensure compliance with the Federal Truth in Lending Act. By adhering to these regulations, they uphold the principles of fair lending, consumer protection, and transparency in the financial services industry.

Free preview